William_Potter/iStock via Getty Images

We have previously covered ASML Holding (NASDAQ:ASML) here as a pre-earnings article in November 2022. The company will be announcing its FQ4’22 earnings soon, by mid-January 2023. Its earnings and raised guidance on Investor Day have been excellent indeed, triggering a remarkable stock recovery by early November 2022. However, it remains to be seen if the rally will hold, despite the tremendous backlog of €38B and bookings of €8.9B reported in the last quarter.

For this article, we will be focusing on the rapidly developing Chips war between the US and China, potentially affecting ASML’s stock valuations in the short term. However, we will also share our reasons for remaining bullish on its future execution, due to the foundries’ robust planned capital expenditure, significantly aided by the ongoing self-sufficiency movement thus far. Considering these factors, we concur with the management’s statement that the China ban will not significantly change its 2030 outlook.

Investment Thesis

The ASML export restrictions began during President Trump’s era, with the aim of maintaining a two-generation technology or the equivalent of a four-year gap between the global chip production capabilities and that of China. However, the recent development implies an aggressive wide-ranged curb, with some analysts projecting a decade’s gap ahead.

This is probably attributed to China’s surprising technological advancement in the older 14-nm chips, reaching the globally competitive level of data storage NAND chips. Another rumor suggests that China has been able to produce 7-nm chips since 2021, using an older generation of deep ultraviolet lithography (DUV), eclipsing Intel’s (INTC) launch in 2023. A lower labor cost also enables it to offer a more attractive selling price contributing to the country’s large ~20% market share of global chip production thus far.

No wonder the US government opted for these strategic restrictions to curb China’s forward technology to above 14-nm. This is also significantly attributed to the latter’s previous Zero Covid Policy over the past three years, which tremendously disrupted the global supply chain. It has naturally prompted the US government to push for strategic self-sufficiency across multiple sectors, with semiconductor chips being one critical component.

How Will The Restriction Affect ASML’s Top Line?

The latest news indicates that ASML may have to comply with the global tightening controls over the exports of its equipment to China, representing a notable headwind to its forward top and bottom-line growth. The country accounts for 14.72% of the company’s revenues in FY2021. The number has also been growing notably from 11.59% in FY2019, despite the previous export restrictions.

Depending on how the eventual restrictions are structured, we do not think ASML’s performance will be materially impacted in the short term. The critical question will be from FY2024 onwards, since the company has also committed to raising its annual production capacity to 90 units for 0.33 of low NA EUV and 600 units for DPV, with an unspecified sum for 0.55 High-NA EUV.

Due to the new export agreement, ASML’s High-NA EUV equipment may not be available to China since it represents cutting-edge technology capable of 3-nm or lower, superior to most offerings in the market. Market analysts expect the 3-nm chips to be commonly utilized in the next generation of autonomous vehicles, 5G/6G internet, cloud infrastructure, artificial intelligence, and potentially military applications.

Due to the growing political pressure, Apple (AAPL) has already reversed its original plan of using Yangtze Memory’s chips. Nvidia (NVDA) has also released a lower-performing A800 GPU, which complies with the performance threshold determined by the Chips ban. The combination of the Chips and equipment ban will likely limit the country’s technological advancement, including core computing and artificial intelligence capabilities.

On the other hand, Taiwan will still have access to the technology, due to Taiwan Semiconductor Manufacturing’s (TSM) interesting geographical predicament. The latter holds the title of the world’s largest foundry, with a leading market share of 53.4% by H1’22. The island also accounts for 39.33% of ASML’s FY2021 revenues, likely attributed to the foundry’s capital expenditure of NT$839.19B or the equivalent of $30.25B in the same year.

TSM’s Capex is expected to further expand by 33.18% to NT$1,117.66B or the equivalent of $36.39B annually through FY2024, attributed to its expanded Arizona plant. The first plant is expected to be completed by 2024 for 4-nm chips, with the subsequent one ready by 2026 for 3-nm chips. Notably, the latter may likely be produced with ASML’s High-NA EUV equipment.

While ASML does not break down South Korea’s shipment, Asia-Pacific accounts for 13.99% of the company’s revenue in FY2021, likely attributed to Samsung (OTCPK:SSNLF), the world’s second-largest foundry with a market share of 16.5% in H1’22. The company similarly reported a growing Capex of 47.12T Won or the equivalent of $39.58B in FY2021, with analysts projecting a minor expansion of 5.98% to 49.94T Won or the equivalent of $38.20B in annual Capex over the next three years. Furthermore, Samsung is aiming to launch advanced 2-nm chips by 2025 and 1.7-nm by 2027, using ASML’s High-NA EUV equipment as well.

Other companies, such as INTC and Micron (MU), will also build new fabs in the US, pointing to the more than robust demand for ASML’s equipment over the next few years. Therefore, the China ban will likely have a muted impact, with equipment simply flowing to other customers. It is still unclear how severe the export restriction will be, since China is currently still able to purchase the company’s older DUV equipment.

So, Is ASML Stock A Buy, Sell, or Hold?

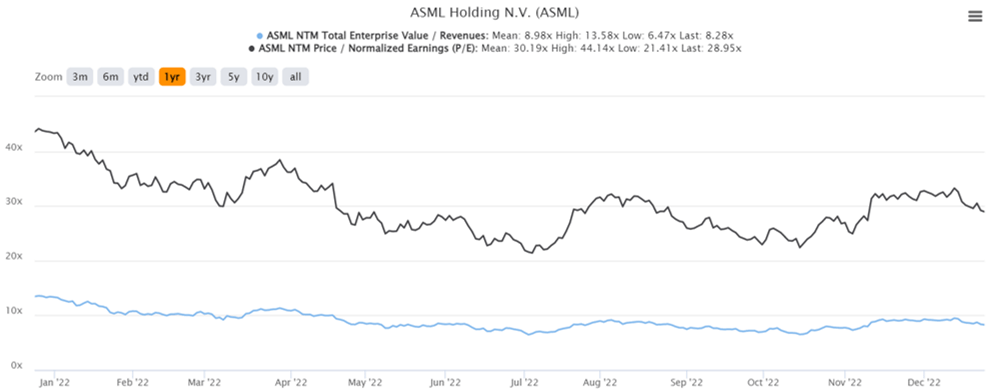

ASML 1Y EV/Revenue and P/E Valuations

S&P Capital IQ

ASML is currently trading at an EV/NTM Revenue of 8.28x and NTM P/E of 28.95x, lower than its 5Y P/E mean of 32.13x. Otherwise, somewhat in line with its 1Y P/E mean of 30.19x. Based on its projected FY2024 EPS of $24.44 and current P/E valuations, we are looking at a moderate price target of $707.53. These mirror consensus estimates’ target of $741.67 as well, indicating an excellent 34.51% upside potential from current levels, despite the 53.23% rally from the October 2022 bottom.

Considering its critical role in the semiconductor market and the ongoing digital/ electrification efforts, ASML remains a closely watched stock in our portfolio indeed. While there may be some geopolitical headwinds to its valuations, we reckon most of it is already baked in, due to the significant moderation from its peak P/E valuations of 52.30x since April 2021.

Combined with the abovementioned factors, we continue to rate ASML stock as a Buy. Naturally, investors that choose to nibble here need to be aware of the potential volatility through 2023, as the Feds are also poised to keep raising until a terminal rate of 5.1%, higher than the previous projection of 4.6%. PC demand is unlikely to return in the short term too, due to tightened corporate and consumer discretionary spending from the rising inflationary pressure. Nonetheless, no matter the soft landing or recession in 2023, ASML’s moat remains robust, safeguarding its forward profitability through the next decade.

Incidentally, bottom-fishing investors may try waiting for another $400s entry point. However, we would also highlight the folly of attempting to time the market, since it would be more prudent to dollar cost average accordingly.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.