wildpixel

V.F. Corporation (NYSE:VFC) withstood a significant selloff from early December that was worsened by the departure of its ex-CEO Steve Rendle, as it also downgraded its FY23 forecasts. In addition, the company highlighted that it sees worse-than-expected headwinds in its North American segment, which was not contemplated in its previous guidance.

Rendle’s departure also added to the uncertainty as Credit Suisse (CS) downgraded VFC, arguing against “the abrupt CEO transition and lack of clarity on which brand is seeing incremental pressure.”

As such, VFC lost all the gains from its November lows, as inventory, and macroeconomic headwinds heaped further pressure, forcing weak holders to flee.

However, we are pleased to point out that VFC has seen robust support as the selloff triggered a bear trap, which re-tested its November lows. Moreover, we gleaned buyers have also returned to undergird VFC at a critical juncture, suggesting that it should consolidate constructively from here.

Notably, China’s recent reopening from its COVID lockdowns should also help lift the company’s operating performance in 2023/24, as we believe it has not been reflected in the company’s guidance. Also, Wall Street estimates have been downgraded following the recent outlook revision by V.F. Corporation.

As such, we assessed significant headwinds baked into its outlook while the company continues searching for a permanent CEO. Also, we don’t expect any material changes to its FY27 model that the company communicated at its Investor Day in late September.

Notably, the project is mainly driven by CFO Matt Puckett. However, when the permanent CEO comes on board, we cannot rule out material changes to its key executive ranks. Hence, it could be prudent for investors to lower their expectations of its FY27 model, given the recent outlook change and Rendle’s departure.

Despite that, Nike’s (NKE) most recent earnings release suggests that inventory headwinds could be nearing its peak or past its peak. While consumer discretionary headwinds could worsen in 2023/24 as we potentially head toward a recession, VFC’s battered valuation has likely reflected its execution challenges.

Accordingly, VFC last traded at an NTM EBITDA multiple of 12.6x, well below its 10Y average of 15.2x. Moreover, with an NTM dividend yield of 7.15%, well above the two standard deviation zone over its 10Y average, we believe the market has priced in massive pessimism.

Notably, based on its revised adjusted EPS guidance of $2.1 (midpoint) for FY23 (year ending March 2023), its projected payout ratio has increased to 93%. It’s much higher than FY22’s 56% payout ratio, suggesting the market could be pricing in the risks of a dividend cut if V.F. Corporation faces even more downside risks through FY24.

Hence, we postulate that the market’s positioning is justified, as we need to be prepared for a global recession, despite China’s reopening. Moreover, the onslaught of COVID infections could hamper a rapid recovery in China’s economy. Therefore, investors should be patient and expect any mitigating impact from China’s recovery only from H2CY23, as we could be due for a near-term recession.

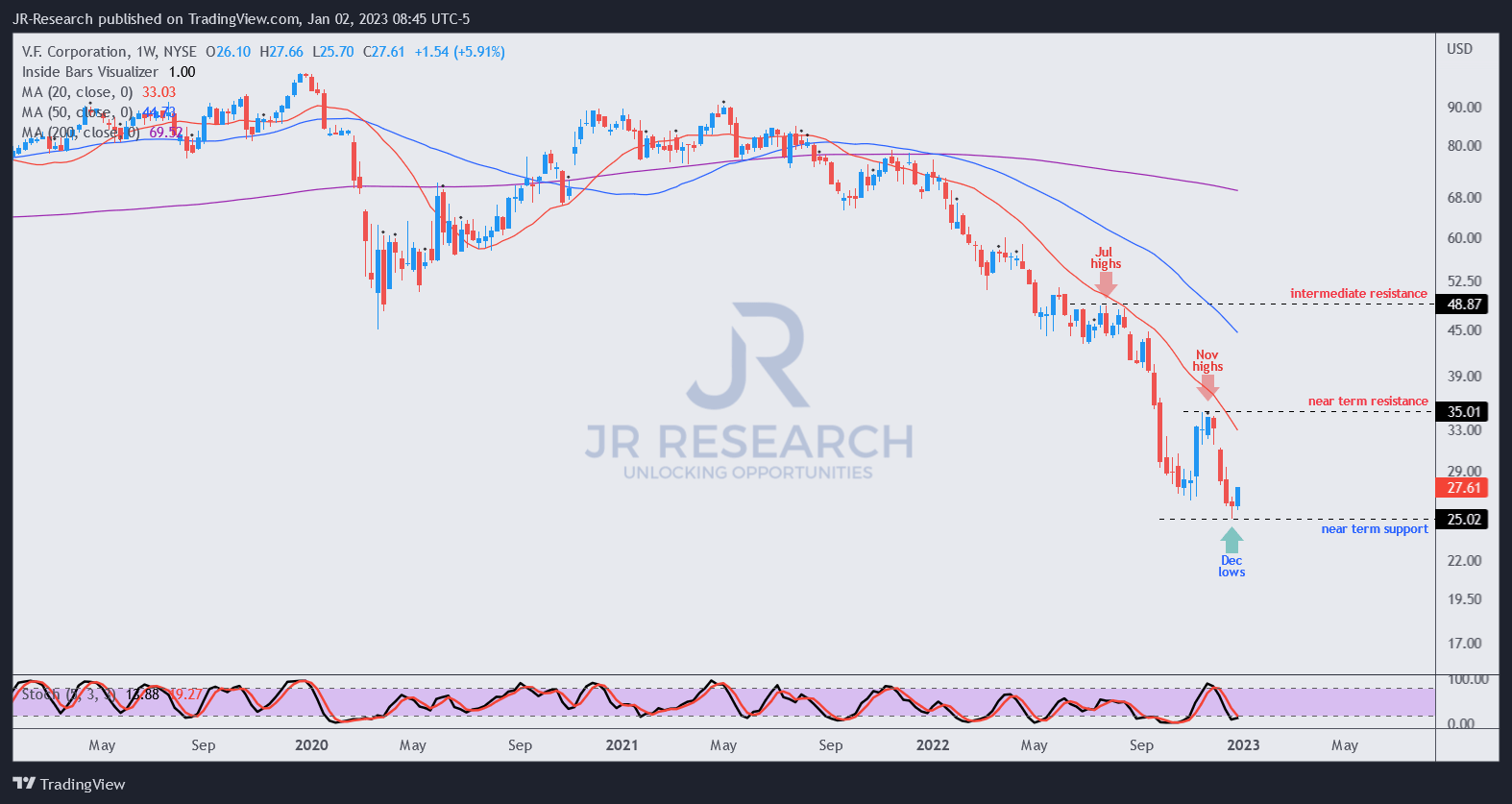

VFC price chart (weekly) (TradingView)

As seen above, VFC formed a near-term bottom at its December lows. We assessed that it’s a formidable bear trap, suggesting market operators forced a steep selloff that took out November lows before reversing the selloff to form a bullish reversal

As such, VFC has decisively retaken the lows from November and should consolidate constructively, even though investors should temper their expectations of a near-term recovery.

However, if you have the patience to hang on to it, the reward/risk is likely skewed substantially to the upside. Accordingly, a recovery to its November highs suggests a price-performance upside (excluding dividends) of nearly 30%.

At that level, it implies an FY24 EBITDA multiple of 14x, still below its 10Y average. Also, we assessed that its earnings estimates have upward revision potential if the company could improve its execution to cross the Street’s lowered bar over the next couple of years.

Rating: Buy (Reiterated)