Clearwater Seafoods (OTC:CSEAF, TSX:CLR) is a publicly traded harvester and processor of shellfish. The company is based in Atlantic Canada, and the majority of its operations are in the ocean surrounding that area. It also has an 85%-owned joint venture that harvests scallops off Argentina, and acquired a shellfish company operating from the UK in 2015. The company primarily operates in shellfish, with clams, scallops, shrimp, and lobster being examples of primary products. It has a premium positioning within most of its markets, with significant exposure to frozen at sea and live products, which command premium prices in the marketplace.

The company has significant hard assets, which are primarily composed of the vessels it uses for harvesting, as well as onshore processing assets. However, the most interesting asset is the most long-lived, but also the most subject to political interference. That is its quota/licenses to harvest seafood. The company has a variety of transferrable licenses which give it exclusive or protected rights to harvest certain species in certain areas.

These licenses are extraordinarily valuable because they confer a monopoly and a durable competitive advantage to the company. Because of population growth, changing consumer preferences, and the rise of the middle class in Asia, consumption of premium seafood seems likely to continue to grow. Given that in many of its areas Clearwater has a harvest monopoly (at least locally) on a product, the company should be able to push through price increases that exceed the rate of inflation.

Demand for some of its products (lobster consumed in restaurants, for example) has declined as a result of COVID-19. The firm also has significant debt levels. However, there is also an owner-operator type of management with significant skin in the game, and the company has been running a strategic process that has the potential to result in a sale of either the whole business or a portion of it.

Quota and Quota Risks

Clearwater’s quota and licenses for a variety of offshore fisheries is its most important asset. However, its quota asset also comes with political risk. In Atlantic Canada, where the company is based, the offshore fisheries are those farther from shore, which are dominated by big companies like Clearwater Seafoods. These “corporate” fisheries are more profitable and consolidated than the inshore fisheries. Inshore fisheries are those with licenses to fish closer to shore, and they are only granted to individual fishermen. Those fishermen are much more politically powerful in Canada than the corporate fishermen they compete with. There are enough of them, and they vote as a block so that they control a number of seats in Canada’s parliament, which gives them leverage. They are also a better “story” for politicians to tell – regarding protecting the little guy, as opposed to protecting big corporations.

The Government of Canada’s Department of Fisheries and Oceans (DFO) has demonstrated this bias a number of times, and the uncertainty that bias creates reduces the value of the company’s quotas and licenses. One example is the Northern shrimp quota. Northern shrimp were initially caught by large offshore vessels, but after the decline of the cod fishery in the 1990s, the inshore cod fleet from Newfoundland applied to be granted shrimp licenses. The existing offshore fleet objected, but the licenses were granted anyway, as Newfoundland was in dramatic economic distress. The principle the licenses were granted on was a compromise – first-in, first-out – so that those who had the licenses first would keep them if shrimp stocks declined. Now that decline has happened, as cod/capelin stocks are rebounding (crowding out shrimp in the food chain), and the shrimp quotas need to be reduced to keep the shrimp population sustainable. Those same inshore fishermen protested vociferously enough that the first-in, first-out principle was scrapped. While I don’t think this change is a huge issue for Clearwater, it does demonstrate the lack of property rights around its quota.

More pressing is the issue around the Arctic clam fishery. Canada has been undergoing a process called reconciliation, which is designed to improve the lot of the indigenous people of the country, as a part of the national apology for residential schools. The DFO decided to grant 25% of the Arctic clam fishery to an indigenous group (which will be fished by a corporate partner) as part of the process. Given Clearwater previously possessed 100% of that quota, this is material to the company. It is especially significant given the company has recently purchased two (expensive) state-of-the-art factory ships for the purpose of harvesting its clam quota. Now that it will have less quota, the company’s new ships will not be fully utilized. That said, Clearwater was able to once again retain its 100% share of the Arctic clam fishery by partnering with a number of First Nations. There was a political scandal around the connections of the other bidder (who originally won the new license), and since that came out, the government has been renewing Clearwater’s ability to use it on a short-term basis. The company will still own the other 75% of the quota, and I would expect the government to more permanently enshrine this agreement – it seems quite win-win, as both the previous license owner and the First Nations came to it voluntarily.

Lobster Quota

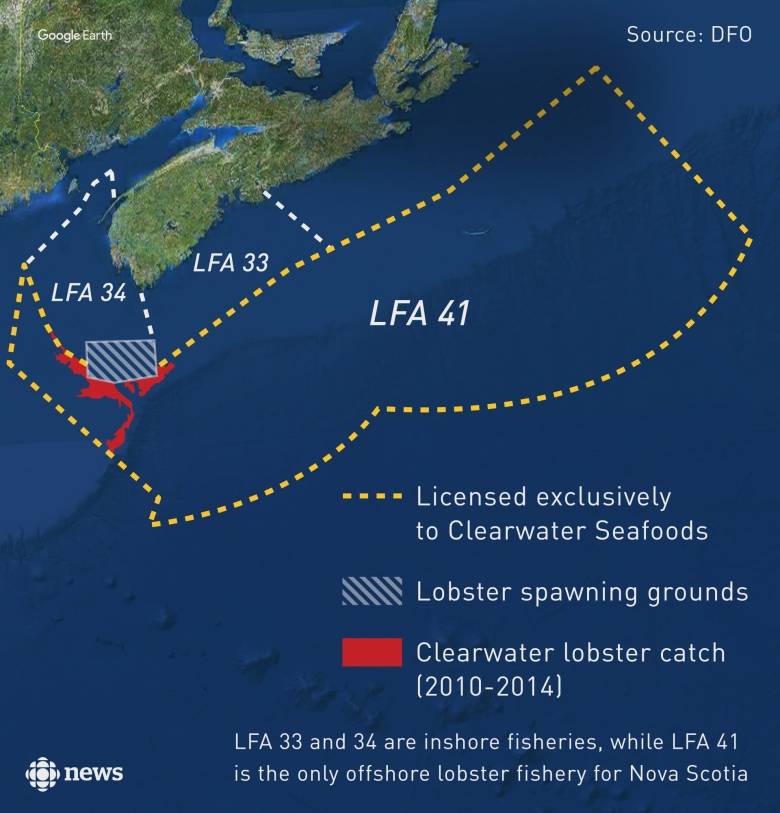

On a go-forward basis, there is the potential for these types of quota losses to continue. Aside from previously holding all the Arctic clam licenses, Clearwater Seafoods holds all the offshore lobster licenses in Nova Scotia. This is in contrast to the inshore licenses, which are held by a variety of smaller fishermen, each of whom has a boat and the shared right to fish the inshore area with a certain number of traps only during the fishing season. On the other hand, Clearwater has a giant offshore area where it has exclusive fishing rights. The company can use as many traps as it chooses to, as long as it fishes within its quota.

Clearwater’s license is much more valuable than an inshore license, because it is more efficient to use one big vessel than a bunch of little ones. The ability to fish all year round is also extremely valuable. It allows the more efficient use of crews, and means less ships can catch the same amount. Also, because the market is better supplied during the inshore season, prices for lobster are higher during the off season, when only the offshore fleet is active.

All those attractive features mean the inshore fishermen would love to have access to the offshore licenses. The difference between the fleets isn’t that much in 2020, and the inshore fishermen have the ability to fish in the offshore. They also give a very sympathetic interview on why they would love to have the ability to fish the offshore areas. You can see a portion of that in the CBC investigative report linked below the following map of Nova Scotia lobster licenses.

Source: CBC News Investigative Report

I believe Clearwater Seafoods’ lobster marketing and distribution network has material value outside of their lobster quota. It operates large tanks where it can store live lobsters. This distribution network is exceptionally valuable because live lobster is much more valuable than canned lobster, as it is usually eaten as a special occasion food, often at restaurants. While that has hurt things during COVID-19 as restaurant demand is down, I think eventually special occasions will remain a time when people choose to go out. After all, anything coming out of a can has quite a bit less cachet, and selling prestige items is generally a recipe for good margins.

The company buys lobster during the inshore season from inshore fishermen, and sorts them on the basis of how long they can survive in holding tanks, and then ships them out via air freight all over the world over time. That way, it can offer restaurant wholesalers a consistent supply of high-quality lobster throughout the year. Clearwater has internalized its freight forwarding as well, which provides it the ability to land lobster anywhere in the world at a competitive price. This also gives the company competitive power over the inshore fishermen it buys from, as the other choice is selling to a cannery or taking a lower “in-season” price. From personal experience, lobster is often much cheaper in Western Canada during the summer, and is a promotional item during that time. As one example, a large chain of steakhouses in Canada runs a “Lobster Summer” promotion every year, where it brings in huge quantities of fresh lobster at special prices. Clearwater Seafoods has the ability to sell lobster at higher prices throughout the year, which gives its distribution system material value. This is hard to quantify, because the company doesn’t break out the margins by caught and purchased lobster, but it should reduce the cyclicality of the lobster business, as much of the margin isn’t from caught seafood, but rather more like a “storage fee,” which it should be able to charge irrespective of the size of the harvest.

The company recently announced the sale of a portion of its lobster licenses (two out of eight total) to the Membertou First Nation. The proceeds of $25 million will help it pay down debt, and the lobster will still be harvested using Clearwater’s ships. This should help provide the company political cover for its lobster licenses, as lobster has recently become a contentious political issue in Canada.

The Supreme Court of Canada ruled many years ago that a treaty with the local First Nations allows them to fish for a moderate livelihood. The government has delayed implementation of that ruling, and local First Nations have begun fishing out of the commercial lobster season relying on that ruling. There have allegedly been a number of violent acts in retaliation against this. Many of the inshore commercial fishermen are worried that this extra harvest will impact their livelihood. It seems reasonable that Clearwater wants to avoid the controversy and just keep profitably fishing its offshore licenses. Selling some of them to a First Nations group seems like a good way to gain political cover in a contentious issue, and provides additional funding to the business as well.

Leverage

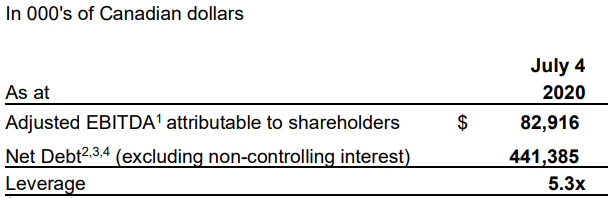

Clearwater has $441 million of net debt and long-term obligations. This is a relatively high rate of leverage for a company with significant non-controllable variability in its cash flow. With a target leverage ratio of 3.0X EBITDA, it can reasonably be expected to utilize most of its free cash flow for debt repayment as opposed to shareholder initiatives.

Source: Clearwater Seafoods Q1 2020 Financials

With the company trading at a market capitalization of $469 million, that implies the enterprise value is 10.9X EBITDA. That is probably relatively full valuation for Clearwater (especially given that their depreciation expenses are real given their assets spend time sailing around in salt water). However, the leverage provides significant potential upside to the common shareholders simply through the deleveraging process. The price of the common shares has appreciated significantly recently as a result of speculation around its strategic process. There have been reports of numerous bidders, both private equity and strategic. The current valuation of the firm is relatively full, which may not leave room for a significant premium from here. On the other hand, EBITDA has recently declined for reasons that are probably transitory (COVID-19), and Clearwater has some one-of-a-kind assets (monopoly power in offshore lobster and Arctic surf clams) that would be very attractive to multiple potential buyers. The same report linked above suggested sources had told them bids were in the $1 billion Canadian range, which would be $559 million CAD after subtracting the company’s net debt, or approximately $8.60 per share. The current price of $7.20 per share thus allows for some upside if a deal is consummated.

Catalysts and Risks

The biggest catalyst and risk by far here is the completion or cancellation of a deal, so shares are likely to have significant near-term volatility based on that news flow. However, if a deal doesn’t close, I think there is likely to be a buying opportunity as event-driven investors exit the name.

Non-market cyclicality is both a potential catalyst and risk here. There will be natural cycles that are both biological and market-based. The amount of product they produce will depend on everything from plankton reproduction to global warming. That provides more share price volatility, which can be a benefit for investors who are able to anchor to an intrinsic value and trade a position around it, but also increases the likelihood of experiencing permanent losses if the shares are purchased at the peak of a cycle. It seems probable that demand is more likely to grow than shrink from current COVID-19 lows, but the biological cyclicality is harder to predict.

The other potential risk for Clearwater from the supply side is the Canadian government adding Marine Protected Areas. The government has committed to protecting 10% of Canada’s waters as protected areas, and that designation restricts commercial fishing from occurring in these areas. There is a risk that productive fisheries will be eliminated, thus reducing the allowable catch in total, at least in the near term. There have been accusations that this process has been hijacked by special interest groups. However, those allegations generally revolve around MPAs being used to neutralizing the offshore oil and gas industry, not the offshore fishery, and this is a time when the political image of the independent fisherman helps rather than hurts the company in the political process.

One other potential catalyst is an improved balance sheet position. While Clearwater’s leverage is high, the debt markets don’t seem to be concerned about repayment. Its 6.875% unsecured US dollar-denominated debt trades at more than $1.05 on the dollar, with a yield to maturity of around 5%. Even if the company doesn’t improve its leverage metrics, it is likely that it will be able to refinance the balance sheet at a lower cost. If leverage metrics improve, that lower cost could be very material. That is also a potential source of synergy for buyers – many of the rumored buyers (especially the pension plans) could refinance at much lower cost, which would be immediately accretive and might thus increase the price they are willing to pay for the equity.

Seasonality

Clearwater has explicitly called out an expected increase in leverage during the first three quarters of the year due to seasonality. The best quarter for both clams and shrimp, as well as some of its European products, tends to be Q4 of the year, and that adds materially seasonality to the results of the company as a whole. The company’s net debt is usually much higher in the summer, as it buys lobsters from independents and stores them for sale later in the year. That seasonality is likely to be a factor for the bidders as well, as they may consider some of the firm’s net debt more a form of working capital, potentially allowing for a higher price.

Capital Spending

Clearwater has historically spent more than 100% of its cash flow on capital spending after accounting for payments made to the non-controlling partner in its joint ventures. That is largely how it ended up with so much debt. The company has spent that money largely on two new ships for the clam harvest. The newest ship only began harvesting clams late in the first quarter of 2018, so the company is now benefiting from the higher efficiency in the harvest and should be entering a period of lower capex. That should allow it to re-prioritize cash flows to reducing leverage even if there isn’t a buyout.

Conclusion

Clearwater has a widely diversified base of operations across a variety of seafood types in a variety of geographies, although it is still concentrated in Canada. The company has a material position of licenses that allow it to exclusively harvest in specific areas, which is a significant competitive advantage. The biggest risk for Clearwater is that the government may reduce these licenses over time. However, the macro environment is a benefit here, as the growing middle class in Asia and recovery from COVID-19 provide material tailwinds for the company and its margins.

The biggest near-term factor will be whether the company agrees to a sale. I think Clearwater’s exclusive rights to various species of seafood will provide some downside protection, but would expect significant near-term downside if it announces it will go forward independently.

To be notified of pieces on underfollowed microcaps, hit the orange follow button at the top!

Most of my best ideas are not released to the public, and are instead exclusive for members of The Microcap Review. Members get value stock ideas, plus net-net ideas, plus multiple special situation ideas every month. The special situations include merger arbitrage, liquidations, tenders and more. I am currently offering a two week free trial for new subscribers. That free trial allows you to check the service out with absolutely no risk, and if it isn’t for you, cancel online with zero hassle.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.