Rich people have small TVs and big libraries, and poor people have small libraries and big TVs. – Zig Ziglar

LexinFintech Holdings (NASDAQ:LX) might be an unusual name to some, but it is one of the biggest online consumer finance and e-commerce platforms operating in China. Its target market for its platform and services is the young Chinese professional. It provides customers with a credit line for purchases of consumer products which they can then use for purchases on the company’s e-commerce platform. Customers also receive a virtual credit card with their credit line which they can use to make purchases outside of the e-commerce platform.

The services that LexinFintech Holdings provides falls into two main categories:

- Loan servicing and interest income.

- Direct sales from its e-commerce platform and membership services for the said platform.

The bulk of its revenues come from the facilitation of credit that it provides to its customers through its credit partners and partner banks and from the earning of interest from such credit lines.

The online consumer finance industry is a new one in China with low competition and plenty of room for growth. This is despite the Chinese economy facing a significant slowdown due to the coronavirus pandemic, where now it is expected to be the only Fitch 20 country expected to show growth by the end of the year 2020. An accomplishment that many in more developed nations would welcome.

Company Performance

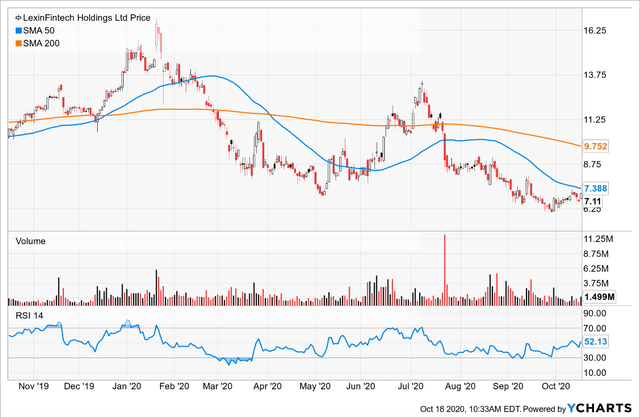

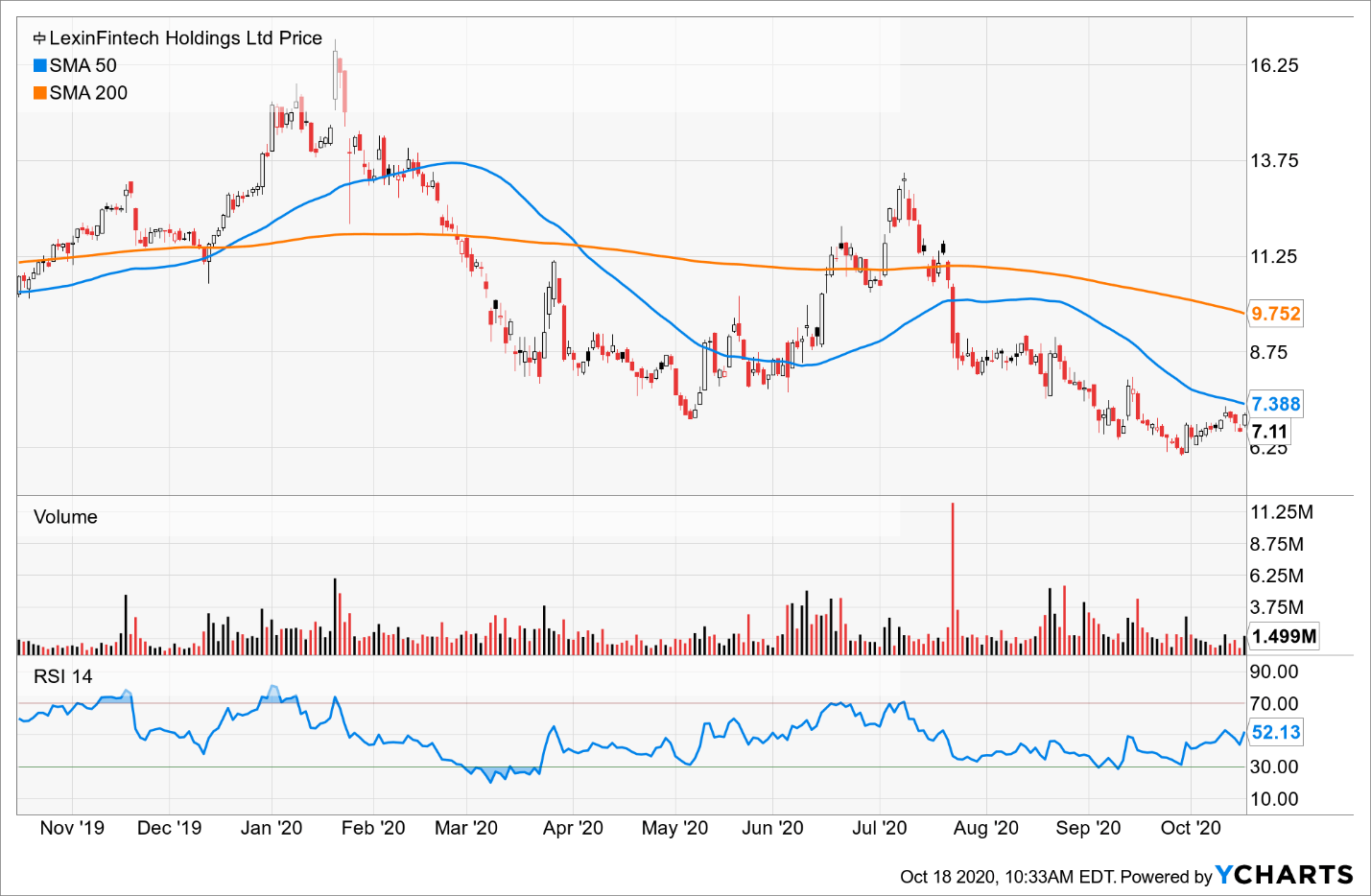

LexinFintech Holdings’ share price has suffered since its high in January 2020 of $16.64 with the main reason behind this being the onset of the pandemic leading to a decline in overall commercial activity and a depression in investor sentiment. Naturally, the significant disruptions in China caused by the pandemic lockdowns meant the shutting down of supply chains and the resulting economic uncertainty, resulting in consumers shopping less, whether offline or online.

Further, the fall in share price is also reflected on the company’s financial performance. This was because its COVID-19 pandemic-related write-offs and provisions to loans meant that the 48.8% increase in loan servicing and interest income and the 109% increase in the e-commerce platform income failed to result in an increase in net income, which recorded a 33.3% decrease. However, for reasons which we will soon see, with the share price trading around $7, which is a decline of over 50% from its January high, it represents a significant opportunity to buy with more than half of the risk having been eliminated from the share price.

The investor concerns that drove the price down are temporary, and the business fundamentals of the company not only remain strong but also have improved making for a powerful case to take advantage of its upside potential. The total number of users of the company’s loan products increased by 65.8% from 4.1 million in the second quarter of 2019 to 6.8 million in the second quarter of 2020. As a result, loans and credit lines increased by 57.8% from RMB 26.0 billion in the second quarter of 2019 to RMB 41.1 billion in the second quarter of 2020. As a result, the company is on track to meet its loan origination target for the year of 2020.

Similarly, the number of new orders placed on its e-commerce platform increased by a whopping 168% from 27.8 million in the second quarter of 2019 to 74.6 million in the second quarter of 2020. As can be clearly seen, the ever expanding customer base resulted in an increase in business for the company, which bodes well for the future financial performance, especially once the broader economy begins its full recovery.

This business performance can be explained by the many positive traits that company has. For one, the company follows a customer acquisition model that has an extremely low cost. Based on a reading of its 2019 annual report, you can see that the company spent less than RMB 200 on each customer that it acquired and went on to recoup the cost within three months, making a profit thereafter. Second, the company’s track record has shown a strong retention policy by offering its old customers lower interest rates, higher ceilings for their credit lines, and flexible payment schedules. This has also had the dual impact of reducing customer delinquency rates. Third, the company follows a low-risk lending policy by targeting educated professionals as they have higher incomes and a stronger desire to build and improve their credit ratings and borrowing power.

Risks and Future Outlook

COVID-19: The biggest risk that has been outlined for LexinFintech Holdings is the ongoing COVID-19 pandemic which threatens to reduce the amount of consumption by customers, thereby leading to a decrease in the demand for consumer lending the company offers.

Regulatory: Another risk for the company is regulation. As the online consumer finance industry is new in China, it has not had a lot of regulation like in many developed economies and other sectors. However, once the industry starts to truly expand in its outreach, the Chinese regulatory environment could quickly tighten, which will affect all industry players.

Geopolitical: Additionally, the company faces regulatory and legislative threats from the United States as the country cracks down on companies listed on US stock exchanges to make them more transparent. A strong example is recent legislation passed by the US Senate targeting Chinese-owned firms.

Competition: Finally, even though China’s online consumer finance industry is huge, as the industry grows, we can expect more competition to attract the expansive customer base, which will lead to a rise in customer acquisition costs and hurt the bottom line.

Investor Takeaways

From the above analysis, it can be seen that fundamentals behind LexinFintech Holdings are strong, and there are good reasons to think that once the negative elements in the wider economy subside, there will be significant uptick in its share price. In the least, the share price has the potential to rebound to its January levels, which would represent more than a doubling of price. The future is bright for this industry as long as it can avoid too many of the headwinds mentioned, but for those with higher risk tolerance looking to diversify away into global assets, this is a strong candidate for your portfolio.

*Like this article? Don’t forget to click the Follow button above!

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This writing is for informational purposes only and Lead-Lag Publishing, LLC undertakes no obligation to update this article even if the opinions expressed change. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. It also does not offer to provide advisory or other services in any jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Lead-Lag Publishing, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.