andresr/E+ via Getty Images

Investment Thesis

Okta (NASDAQ:OKTA) helps organizations stay secure. As more and more enterprises embrace a zero-trust environment, this provides a strong tailwind for Okta to continue taking market share.

Along these lines, Okta provides investors guidance all the way into the next fiscal year and is expected to grow its top line to $1.8 billion. What’s more, with more than 14K customers and rapidly growing, Okta is now trading the cheapest valuation for some time.

Priced at 18x forward sales, this stock is now enticingly valued.

Note that Okta’s fiscal year and calendar year are misaligned. Throughout the analysis, I’ll only reference its fiscal year.

Investor Sentiment Holds Ground

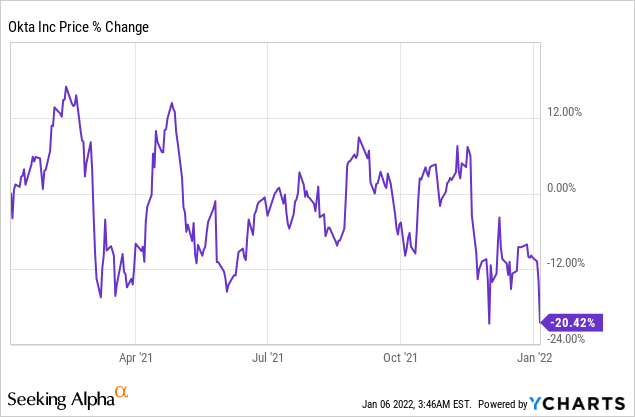

If you follow Okta’s space, you’ll know that countless tech stocks have been bleeding red during the last several months. However, in that light, I have to say that Okta hasn’t fared too badly.

Yes, the stock is down 20% in the past twelve months. But compared with other names, that’s really not that bad.

And the reason why the stock has held its ground is that investors continue to recognize that Okta’s near-term prospects continue to strengthen.

Now, let’s dig further.

Okta’s Guidance Remains Alluring

(Source)

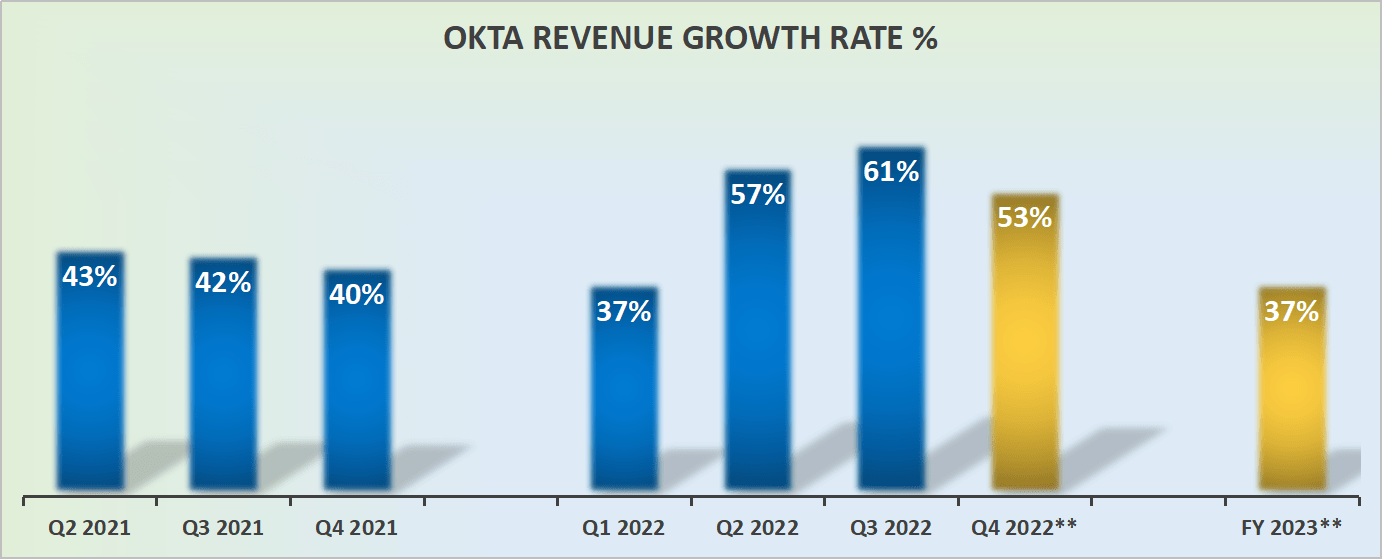

As a brief reminder, Okta acquired Auth0 back in May 2021, so we won’t start lapping that acquisition until Q2 2023. Auth0 was a substantial acquisition that meaningfully increased its revenue growth rates during fiscal 2022.

Moreover, Okta reported its Q3 2022 results last month, and given the shaky market, management decided to get in front of investors’ worries and provided investors ample visibility all the way into the next fiscal year.

Accordingly, as you can see in the graph above, not only is Okta guiding for its Q4 2022 to report strong revenue growth rates, but management sought to allay investors worries that even as it laps the very fast growth Okta reported during fiscal 2022, that its near-term prospects are showing no signs of slowing down.

Okta’s Prospects Continue to Improve

Okta provides its users with cloud security while ensuring seamless access to the right application or device. With the proliferation of applications and different working environments, employees need to allow users access to critical data, while at the same time ensuring access is safe.

(Source)

This is exactly what Okta provides via its Single Sign-on software, a unified identity solution. Okta ensures users are able to remain productive without comprising security.

Since Okta is a cloud-first platform, it’s able to run maintenance operations at lower costs than other on-prem solutions. This translates into higher ROI for customers.

What’s more, as I’ve said before and I’ll say it again, follow the customer as they know best.

(Source)

Oftentimes, it’s more illustrative to follow the customer than it is to follow the share price. As long as more and more customers/users are embracing a platform, that will be more indicative of the company’s success than practically anything else.

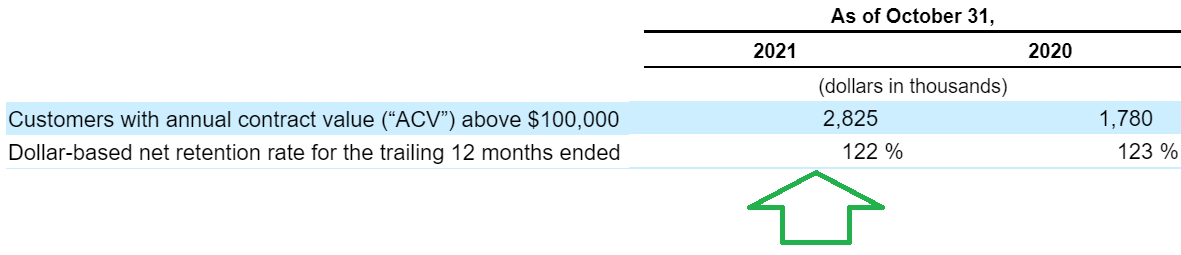

As you can see above, Okta’s customers with annual contract value higher than $100K were up 58% y/y. That is clear evidence that customers are finding value from being on Okta’s platform.

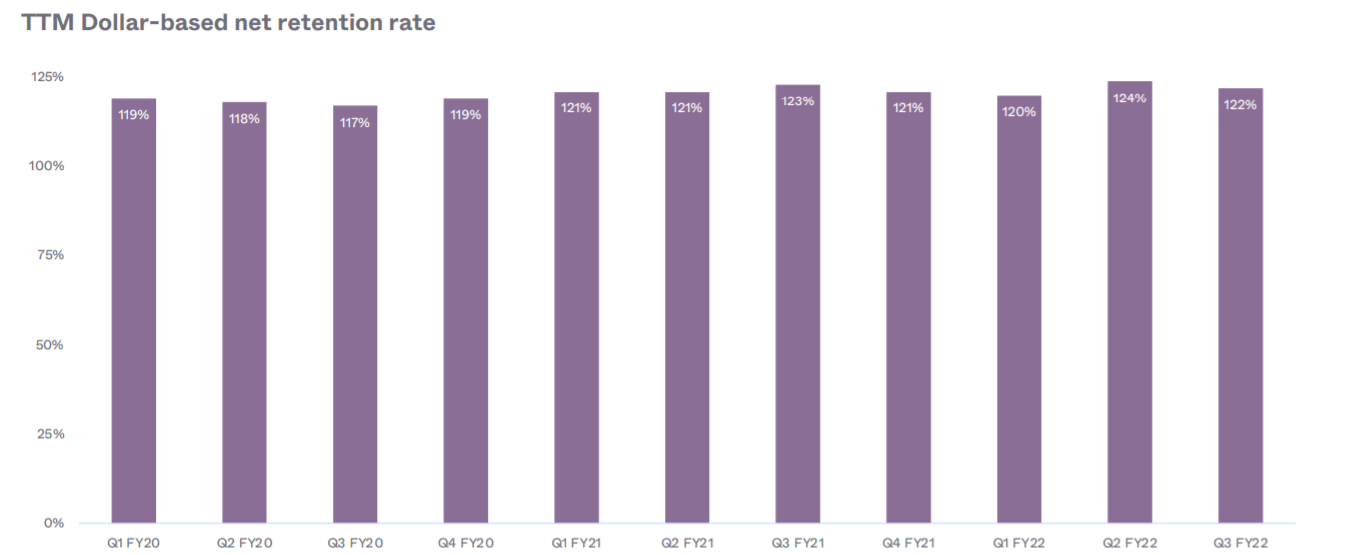

(Source)

Furthermore, you can see above that net retention rates remain flat with the same period a year ago. Again, this reinforces that Okta’s ability to upsell more products to new customer cohorts remains strong at 122%.

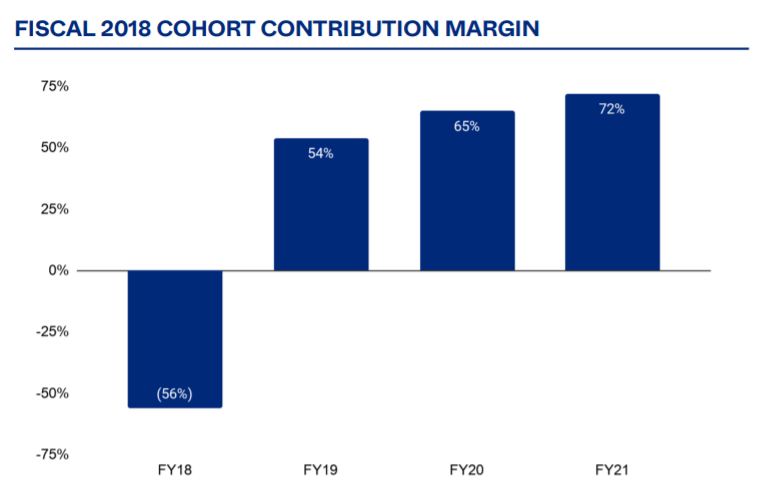

(Source)

Furthermore, during its Q3 2022 results, Okta highlighted its customer economics for its 2018 cohort. As you can see above, after the first year of adopting Okta, Okta’s ability to report positive unit economics are impressive, with Okta seeing positive unit economics one year after the customers are on the platform.

And this leads me to address Okta’s profitability.

Putting a Spotlight on Okta’s Profitability

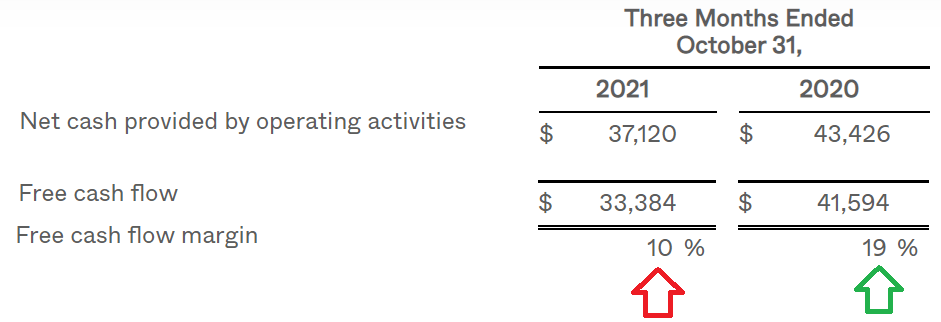

As I remarked back in December, Okta’s ability to generate free cash flow compressed in Q3 2022 compared with the same period a year ago.

(Source)

This is one aspect that has weighed on investor sentiment of late. There’s no getting around the fact that Okta’s determination of investing for growth has translated into it slipping below the coveted Rule of 40.

This is something that investors should keep their eyes on going forward. That being said, I charge that this angle is now already priced into its stock.

Valuation – Reasonably Priced

Ultimately, I’m not going to argue that Okta is the cheapest stock out there in cybersecurity. What I will argue is that it’s very much the cheapest it has been for a while. Rarely does Okta trade as cheaply as it has traded right now.

Okta is priced at 18x forward sales. This is not that expensive when we consider that Okta is probably going to end up growing at close to 40% CAGR over the next twelve months.

For reference, Zscaler (NASDAQ:ZS) is priced at 30x next year’s sales (adjusted for different year-end dates). While CrowdStrike (NASDAQ:CRWD) is priced at 21x next year’s revenues. Reinforcing that cybersecurity names simply don’t trade all that cheaply.

The Bottom Line

Here’s the summary, Okta is guided to grow by 35% CAGR over the next 4 years. This level of visibility doesn’t come that cheaply, at 18x next year’s revenues.

Thus, investors are left with two choices. They can either chase returns elsewhere and hope that the value rotation remains, or they can sit still and allow Okta’s intrinsic value to compound over time.

I believe that one is much better provided for by having patience, conviction, and learning to invest and sit on one’s hands. Good luck!