gorodenkoff/iStock via Getty Images

Introduction

While we, and our clients, have been disappointed by the price action in Schrödinger (SDGR) since the publication of our initial report, our conviction remains high. We continue to believe that SDGR is fundamentally changing the way drugs and materials are discovered. We point investors new to SDGR to our initiation report to gain a full understanding of our thesis. For a quick refresher though, SDGR’s software enables customers to discover new innovative drug candidates at half the cost and in half the time when compared to traditional manual methods. Along with the software business, SDGR has an internal drug discovery segment. Some candidates are fully owned by SDGR while others are in collaboration with partners such as Bristol Myers Squibb (BMY). At the current market cap, SDGR’s internal pipeline is given zero value. The BMY partnership alone represents a potential of $2.7B in milestone payments, of which $1.7B is early-stage milestones, which is currently greater than the entire market cap of SDGR. Any incremental positive news from the internal pipeline will have a two-fold effect on the stock. As it will have a positive reaction just like any biotech would, but also it would be a confirmation of the power and ability of the software.

With the base of an incredibly sticky (>99% retention rate), high margin (>70% GMs), and growing software business aimed at a massive TAM in addition to the upside of a biotech that receives revenue through early-stage milestones, we believe SDGR represents massive upside for investors. In addition, the recent slump in the stock gives investors an excellent risk-reduced entry into a name where much of the potential upside has been priced out.

What’s Caused The Selloff?

Lower Than Expected Guidance

As stated in our initiation report, the initial drop in 2021 for SDGR was caused by lower-than-expected software revenue estimates. After posting better than 38% growth in software for 2020, investors were thrown off when management guided for 10-18% for 2021. While this was disappointing, it is logical.

This is because it takes time for a new customer to scale SDGR’s software, it doesn’t happen overnight. It takes a new customer about 12-24 months to build out an internal infrastructure and transition their legacy systems before they can truly ramp up licensing across their drug discovery programs. With this in mind, we expect the growth within SDGR’s software business to towards the end of 2022 and into 2023.

To go along with the weak guidance, SDGR has posted low to mid-teens growth in the software business through the first three quarters. This has been poorly received by investors. However, we highlight the fact that SDGR management has stated multiple times that the Q4 will be the heaviest in volume, hence why the midpoint of the guide for Q4 is better than 20% growth.

Weak Market Sentiment

In 2021 the market sharply pivoted away from stocks like SDGR. High-growth, biotech, and high multiple stocks all saw significant drawdowns during 2021. This can most easily be seen by the underperformance of ARK Innovation (ARKK) being down more than 20% while the NASDAQ was up more than 20%. ARKK holds a ~4% stake in SDGR, with their most recent transaction being purchase on December 14th.

While the drawdown in 2021 was in many cases needed for these stocks, the drawdown in SDGR specifically was overdone. Investors threw SDGR into the same basket as COVID beneficiaries such as Peloton (PTON), pre-revenue likely frauds like Nikola (NKLA), and broke SPACs like Ginkgo Bioworks (DNA). While the sentiment surrounding these stocks matches the sentiment surrounding SDGR, the underlying prospects of their business are vastly different. SDGR has a real product with real customers targeting a massive TAM that is continuously growing regardless of future COVID circumstances.

Our Expectations Going Forward

Q4 Report

Throughout the year, SDGR management has continued to reiterate the full-year software revenue guidance of $102-$110M. Management has iterated the reason they have kept the wide guidance heading into Q4 is that Q4 is historically the busiest. This comes even as SDGR lowered guidance for drug discovery during the Q3 report, citing the pushout of milestones. What this signals to us is that management is willing to lower guidance and that they are not focused on chasing Wall Street’s numbers. Most recently, with 10 days left in the calendar year, SDGR reiterated the guidance along with the announcement of the retirement of CFO Joel Lebowitz. While this continued reiteration of guidance has given us confidence, this further emphasizes the importance of the Q4 report in our conviction going forward.

If software revenues for Q4 miss or even come in at the low-end, this will severely affect our conviction in SDGR and our confidence in management. This is because it will shift our view on management from honest and long-term focused to misleading and focused on the short-term stock price. Reiterating guidance 10 days before the year-end and then missing that guidance would be a major blow credibility-wise. If this scenario plays out, it would likely force us out of the stock.

The guidance for $102-$110M equates to $27.3-$35.3M for Q4, which represents YoY growth of 9-41% for the fourth quarter. Per our estimates, our median case is for $34.05M in software revenues. In our eyes, anything below the $30M mark would be a failure. This is because $30M represents 20% YoY growth which would mark an acceleration in growth after posting three straight quarters in the teens. This acceleration would also support the thesis of the lag between introducing new customers and their ability to scale out the use of SDGR. We are also looking for gross margins to stay above 70%, but if a fall below that is caused by higher than expected R&D expenses we would not worry.

| Dec 2020 | Dec 2021 Bear | Dec 2021 Median | |

| Software Revenues | $ 24,957,000 | $ 27,111,000 |

$ 34,050,000 |

| YoY Growth | 9% | 36% |

Brick by Brick Capital Estimates, Data SEC

2022 Guidance

Along with the importance of software revenue for Q4, the guidance for 2022 is equally important. Firstly, we will want to hear any new information pertaining to the IND of MALT1 and that it is still on track for submission in the first half of 2022. Along with this, any further commentary regarding their internal and joint pipeline would be welcomed, especially a timeline for their second IND submission.

Below are our bull/median/bear cases for SDGR. We base our estimates off of $108.72M/$23M for 2021 revenues of software/drug discovery. We would want SDGR’s guidance for 2022 to match our median case estimates. However, if software guidance is at or below our bear case, we would be concerned and need to reevaluate our conviction.

| Software Growth | Drug Discovery Growth | |

| Bull | 29% | 95% |

| Median | 21% | 75% |

| Bear | 12% | 41% |

| 2021E | 2022E Bull | 2022E Median | 2022E Bear | |

| Software Revenues | $ 108,722,000 | $ 140,251,380 | $ 131,553,620 | $ 121,768,640 |

| Drug Discovery | $ 23,000,000 | $ 44,850,000 | $ 40,250,000 | $ 32,430,000 |

| Total Revenues | $ 131,722,000 | $ 185,101,380 | $ 171,803,620 | $ 154,198,640 |

Brick by Brick Capital Estimates

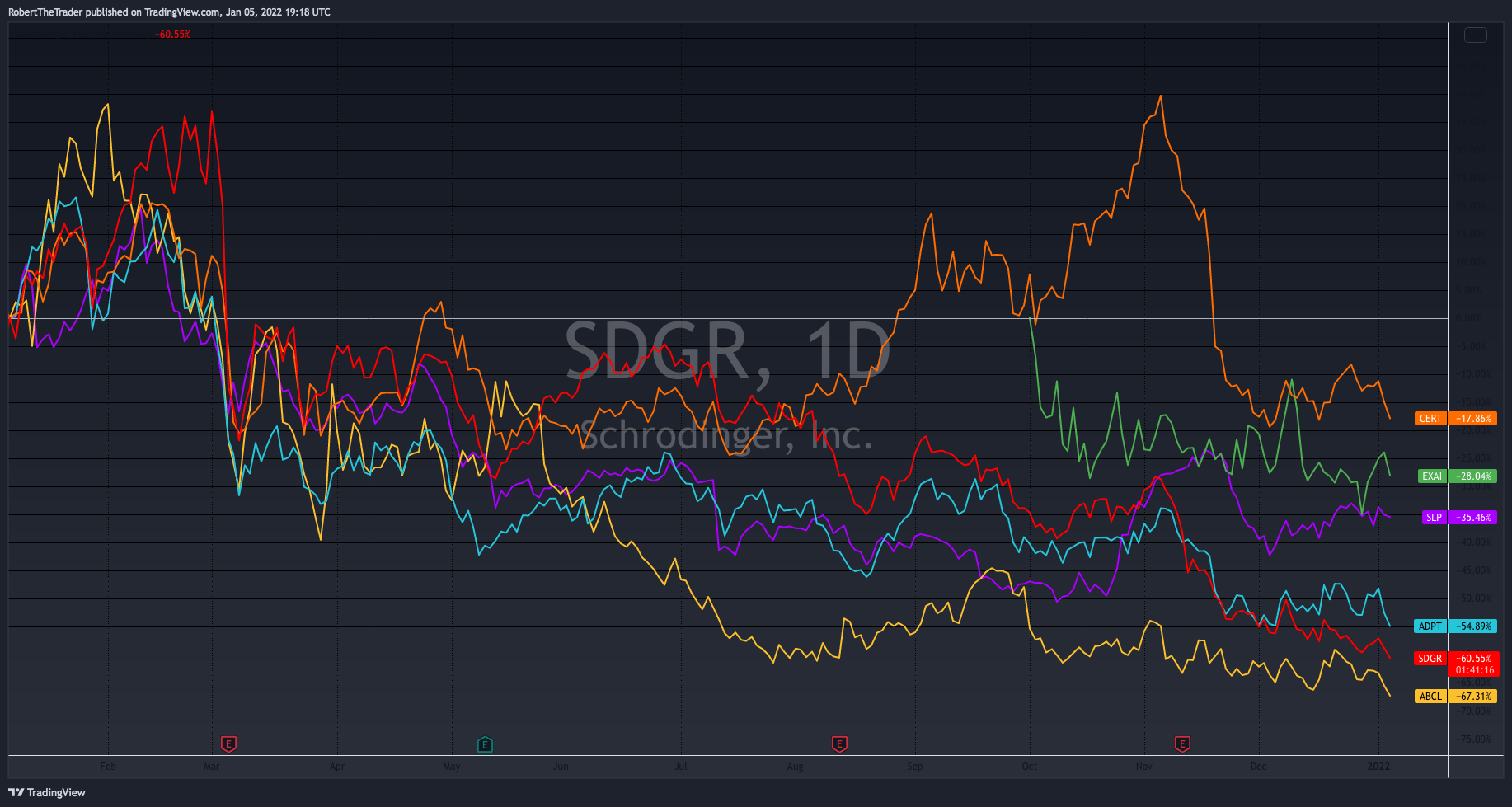

Deeper Look At The Peer Group

In our initiation, we did a deep dive between SDGR and Simulations Plus (SLP), which we believed was the best comparison in terms of offerings of products for drug and material discovery. To give even further context as a justification to SDGR’s high multiple, we compiled a larger peer group table of companies using computational modeling in any stage of drug development. Only two other peers, Exscientia (EXAI) and Adaptive Biotechnologies (ADPT), even have an internal drug discovery pipeline. Which neither are further progressed than SDGR’s. So the high multiples of the peers are not justified by a further progressed pipeline. We also used the peer group average which has a 19.27 price-to-sales ratio, which represents a 42% premium to SDGR’s.

| Symbol | Market Cap | 2022 Estimated Sales | Price/Sales |

| CERT | $ 4,354 | $ 362,000,000 | 12.02 |

| ADPT | $ 3,644 | $ 199,000,000 | 18.31 |

| ABCL | $ 3,669 | $ 132,000,000 | 27.79 |

| EXAI | $ 2,411 | $ 37,000,000 | 65.16 |

| SLP |

$ 976 |

$ 51,000,000 | 19.14 |

| Peer Average | $ 3,010 | $ 156,000,000 | 19.27 |

| SDGR | $ 2,332 | $ 171,803,620 | 13.57 |

Trading View Data, FactSet Estimates

Overall, our takeaway is that SDGR’s current valuation is more than justified when looking at the larger peer group. We also believe that the premium which most of the peer group enjoy currently over SDGR is unjustified. SDGR also has significantly more upside than its peers because of its internal drug discovery pipeline. It is also helpful to put in context that the entire peer group has had a tough past year and that SDGR is not the only poorly performing name in the group. Sentiment surrounding the space has weakened, but the macroeconomic tailwinds and value proposition have not.

Trading View Data

Our Final Thoughts

The future prospects of SDGR’s software business are severely undervalued and the future prospects of their drug pipeline are completely written off at current levels. In 2021 SDGR was incorrectly thrown in the same basket as companies that trade on hypothetical future revenues or minuscule near-term revenues. We continue to believe that SDGR is fundamentally changing the way new drugs and materials are discovered and that they are superiorly positioned to capitalize.

We also believe it is important to point out that the major shareholder David E. Shaw has not sold any stock below the $66 level. Which we view as a confirmation of our thoughts, as a smart investor with a closer understanding of the company believing the stock is below its worth.

While we firmly believe the current risk-reward presented in SDGR is the best since the IPO, we highlight that this dynamic could quickly change depending on the Q4 report and guidance for 2022. So we remain bullish on the name, with the knowledge that the Q4 report may result in a major change in our conviction.