Eoneren/E+ via Getty Images

This week, we cover the stock-picking strategy of Benjamin Graham, considered by many to be the father of value investing, and list the stocks currently passing AAII’s Graham Defensive Investor screens. Since inception (1998), our Graham Defensive Non-Utility screening model has an annual gain of 13.0% and our Graham Defensive Utility screening model has an annual gain of 6.8%. These compare to 6.3% for the S&P 500 index over the same period.

Read on to find out how we put these screens together.

How Benjamin Graham Does It

For over 80 years, the works of Benjamin Graham have served as the bible for value investors. Successful money managers such as Warren Buffett and John Neff swear by the simple message put forth by Graham of looking for value with a significant margin of safety.

Reviewing the philosophies of successful investors such as Graham can often prove enlightening. Graham’s approach focused on the concept of an intrinsic or central value that is justified by a firm’s assets, earnings, dividends, financial strength and stability, definite company prospects and quality of management. By focusing on this intrinsic value, Graham felt that investors could avoid being misled by the misjudgments often made by the market during periods of deep pessimism or euphoria.

This contrarian view dictates that stocks will appear most attractive when they are relatively unpopular with the market. The selection process takes great conviction and discipline because the momentum of the stock market will seemingly be against the contrarian investor, and there may be no clear indication as to when the market will come around to agree with you. In Graham’s opinion, however, the possibility of extraordinary gains only exists when the investor disagrees with the market.

In 1947, Graham published “The Intelligent Investor,” a book that outlined in detail his investment philosophy, and which he continued to update periodically. In the book, Graham felt that individual investors fell into two camps: “defensive” investors and “aggressive,” or “enterprising,” investors. These two groups are distinguished not by the amount of risk they are willing to take, but rather by the amount of “intelligent effort” they are “willing and able to bring to bear on the task.” For instance, Graham included in the defensive investor category professionals (his example, a doctor) unable to devote much time to the process and young investors (his example, a sharp young executive interested in finance) who are as yet unfamiliar and inexperienced with investing.

Graham felt that the defensive investor should confine their holdings to the shares of important companies with a long record of profitable operations and that are in strong financial condition.

Aggressive investors, Graham felt, could expand their universe substantially, but purchases should be attractively priced as established by intelligent analysis. He also suggested that aggressive investors avoid new issues.

This commentary focuses on the defensive investor approach.

Defensive Investor Screening

Graham outlined a set of criteria that helps the investor select securities that offer a minimum level of quality in terms of past performance and current financial position, as well as a minimum level of quality in terms of earnings and assets per dollar of the share price.

Graham’s analysis for the defensive investor is divided into primary industry sectors. Graham presented an investment approach specifically for utilities and industrials but suggested that additional sectors such as financials could also be selected using these criteria. Our Graham screens are therefore broken down into two segments-utilities and the rest of the stock universe.

Adequate Company (Enterprise) Size

Graham preferred large companies. He felt that large firms have the resources in “capital and brain power” to carry them through adversity and back to a level of satisfactory earnings. This concern comes into play for Graham because he looked at stocks of firms that have become unpopular due to unsatisfactory developments of a temporary nature. Graham also felt that the market responds more quickly with a price increase when an improvement is shown for a large firm than for a small firm.

When screening for company size, the three most popular criteria are market capitalization (number of shares outstanding times market price), sales and total assets. Graham focuses on sales for industrials and total assets for utilities because they directly reflect company activities and size while market cap is tied to overall market levels.

Strong Financial Condition

Graham used different measures of financial strength depending upon the industry. As a test of short-term liquidity, Graham specified a current ratio (current assets divided by current liabilities) of 2.0 or higher for industrial firms. No current ratio requirement is specified for the utility sector. Graham stated that this “working capital (current assets minus current liabilities) factor takes care of itself in this industry as part of the continuous financing of its growth by sales of bonds and shares.”

To measure the use of long-term debt, Graham required that long-term debt should not exceed net current assets or working capital for industrial firms. Financing is an important consideration for utilities, so Graham specified that investors look at the debt-to-equity ratio for this sector. He specified that debt should not exceed twice the stock equity (at book value, not market value).

Earnings Stability

Graham liked to look at the historical company performance over an extended period of time. He prefers companies that avoid losses during recessionary periods. This points to industries such as utilities, insurance, food processing, medical supply firms and pharmaceuticals. Graham recommended 10 years of positive earnings in his screen for the defensive investors. Unfortunately, most screening programs on the market today only cover five years of income statement data. Our screen designates positive earnings for the last seven years.

Dividend Record

A common test for financial strength over time is a long period of uninterrupted dividends. The Graham screen looks for companies currently paying a dividend and that have done so over each of the last seven fiscal years.

Earnings Growth

Graham recommended a minimum increase of at least one-third in per-share earnings in the past 10 years, which translates into about a 3% average annual growth rate-a rate that roughly keeps pace with inflation over the long term. Without such a criterion, a screen looking for companies with low multiples will most likely uncover many companies with poor prospects. While Graham felt that even companies in a state of “retrogression” could be interesting if purchased at a low enough price, this was not the domain of the defensive investor. Our filter specifies a seven-year growth rate in earnings greater than 3%.

Moderate Price-Earnings Ratio

Graham seemed to express frustration with the impact of special charges on the earnings per share calculation. He felt that management’s discretion in establishing reserve accounts makes it difficult for the investor to determine whether earnings per share truly reflect the operation of the firm for a specific time period. To help circumvent this problem and smooth the impact of the business cycle, Graham often averaged earnings over a period of several years. When defining the price-earnings filter, Graham required that the price relative to average earnings over the last three years be no more than 15. His goal in establishing the cutoff is to produce a portfolio with an average multiplier of 12 to 13.

Graham wanted to establish a portfolio that is priced reasonably compared to the yield available to the AA bond yield. At the time he wrote the book, investment-grade bonds were yielding 7.5%. When bond yields go up, an investor requires a lower price-earnings ratio to consider a stock purchase. Conversely, lower bond yields mean that an investor could accept a higher price-earnings cutoff, which makes more stocks available for consideration.

Moderate Ratio of Price to Assets

Graham is a believer in using a low price-to-book-value ratio to select stocks and normally requires a ratio below 1.5 for the defensive investor. However, he also felt that a low price-earnings ratio could justify a higher price-to-book-value ratio. Therefore, he recommends that investors multiply the price-earnings ratio by the price-to-book ratio and not let that value exceed 25.5-the product of a current price-earnings ratio of 17 and a price-to-book ratio of 1.5.

Summing It Up

Graham wrote that, “You are neither right nor wrong because the crowd disagrees with you,” he said. “You are right because your data and reasoning are right. In the world of securities, courage becomes the supreme virtue after adequate knowledge and a tested judgment are at hand.”

His investing philosophy focused on finding larger companies with strong historical growth rates that were selling at a discount. Graham summarized his own philosophy by stating that intelligent investing consists of analyzing potential purchases according to sound business principles.

The passing companies of the Graham defensive utility and non-utility screens do not represent a list of recommended stocks. As with all types of investing, it is important to perform due diligence to verify the stock’s financial strength and earnings potential. It is also essential to decide if the stocks match your investing style and risk tolerance before committing your investment dollars.

This Week’s Graham Screen Stock Ideas

15 Stocks Passing the Graham Defensive Investor Non-Utility Screen (Ranked by P/E)

American Association of Individual Investors

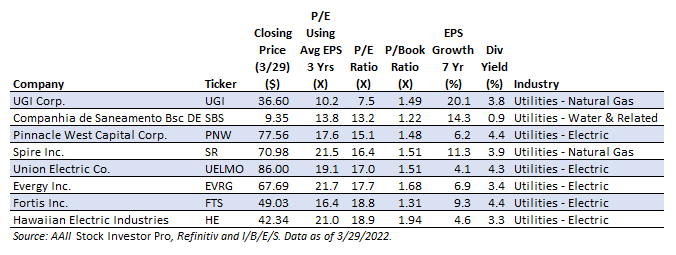

Stocks Passing the Graham Defensive Investor Utility Screen (Ranked by P/E)

American Association of Individual Investors

___

The stocks meeting the criteria of the approach do not represent a “recommended” or “buy” list. It is important to perform due diligence.