OLGA Zhukovskaya/iStock via Getty Images

While the market was worried about the Russian and Ukraine impact on Upwork Inc. (NASDAQ:UPWK), the company was out executing on the business model. The stock traded down to below $20 on fears of a major slowdown, but the freelance marketplace is here to stay. My investment thesis remains very bullish on the gig economy stock now trading at depressed valuation multiples not reflective of a growth company.

FinViz

Russia Impact

Upwork reported an amazingly strong quarter, with revenues beating estimates by $5.6 million. The company grew revenues by 24% in the quarter to reach $141.3 million.

As with a lot of tech companies, Upwork faces a business interruption from the Russian invasion of Ukraine. The company is shutting off all business in both Russia and Belarus on May 1, and Ukraine has naturally been impacted with half the country embattled off and on in war with Russia.

The company forecast ~4% of the business cut off from ending business in Russia and Belarus and another 6% is at risk due to work in Ukraine. In total, Upwork has up to 10% of the business at risk, though the Ukraine portion should’ve felt the impact starting in February. Remember, this is either the talent or the client suggesting some of the work can shift to another area other than business from a client in the 3 countries.

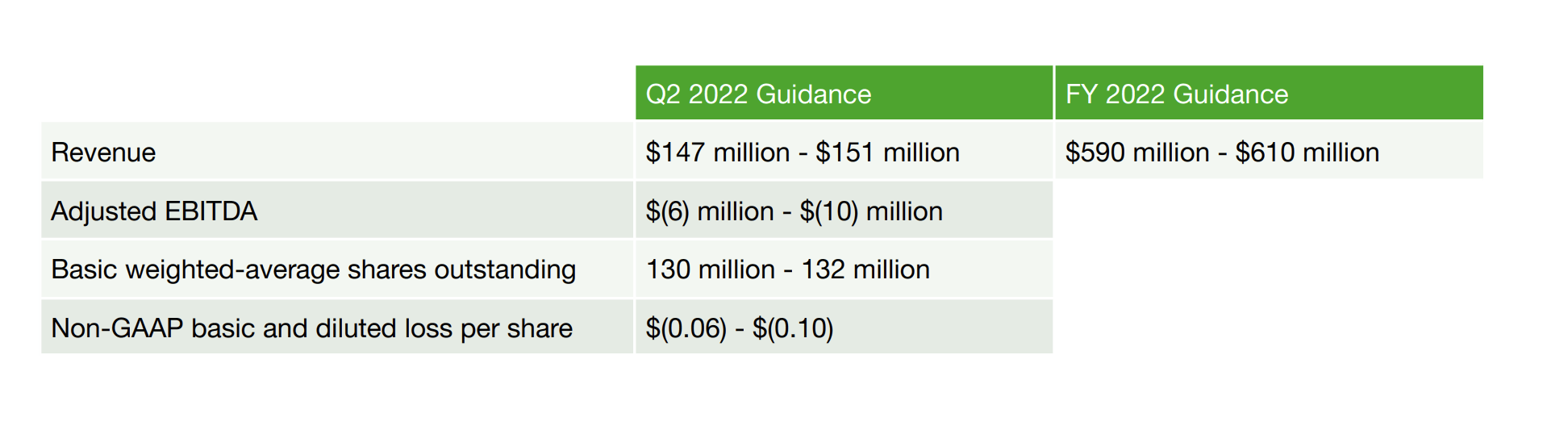

Upwork offered impressive guidance for 2022 revenues of $590 to $610 million. The company did cut the previous annual revenue guidance from $620 to $630 million when providing guidance in early February before the Russian invasion.

Upwork Q1’22 shareholder letter

The guidance cut amounts to an elimination of $25 million in annual revenues for the year, or ~4% of the original guidance and ~5% of the 2021 revenues of $503 million. Remember though, the full Russian impact is only 8 months of the year with probably some disruption for March and April. The Ukraine disruption is for up to 10 months of the year, but a lot of the workers remain engaged and could stay very active with Kyiv no longer active in the war zone. Upwork suggests only a $1 million revenue hit in Q1’22, and the business has seen additional talent signup in Ukraine as families look to find flexible work in a difficult environment.

The company could see substitution of the work originally compiled by Russian talent, possibly even by new Ukrainian workers. The major hiccup with guidance is not knowing what the substitution rates will be for the work knowing so many clients have strong relationships with existing talent.

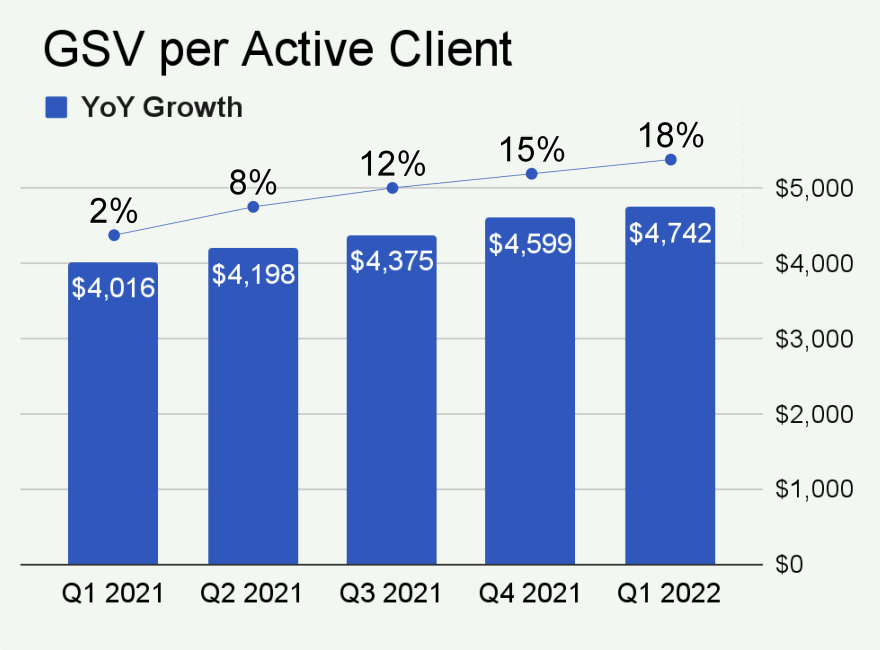

Outside of the war zone, the business model remains strong. Active clients were up 16% YoY to 793K, but more importantly, these clients grew GSV (gross service volumes) by 18% YoY to nearly $5k.

Upwork Q1’22 shareholder letter

Upwork needs fewer new customers when existing clients are spending more. The focus on enterprise customers is a big part of the GSV per active client lift, as the current average spending of only $5K per year is a relatively small amount for most businesses.

Deep Value

The stock has fallen so much that Upwork is now a deep value tech stock while the market is busy shunning overpriced tech stocks. The work marketplace company isn’t EBITDA positive now, but investors shouldn’t bypass the stock for this reason.

Upwork trades at only 3.5x 2023 sales targets lowered by the Ukraine issue. This P/S multiple is normally towards the low end for a tech stock growing revenues in excess of 20% annually.

SA earnings estimates

The company was EBITDA profitable before the war in Ukraine and only lost $0.6 million in Q1’22. The guidance isn’t shocking for the EBITDA loss to accelerate to $6+ million in Q2’22, mainly as more brand advertising spend occurs in the quarter.

Investors shouldn’t exactly want Upwork to focus on profits during this period of developing a global work marketplace for freelancers. The company is only guiding to 2022 revenues of ~$600 million, so the business is relatively small. The biggest issue with not being profitable is a scenario where the company burns tons of cash, but Upwork has a cash balance of $673 million, while the net cash position is only $121 million due to $562 million in debt.

Takeaway

The key investor takeaway is that Upwork is primed to rally when the stock market moves away from the current panic mode. The stock trades at a minimal P/S ratio due to the Ukrainian issues and doesn’t fall into the high multiple tech stocks deserving of an additional sell-off.

Investors should use weakness to load up on Upwork, with the Ukraine headwind turning into a tailwind for a vibrant business.