David Becker/Getty Images News

Background

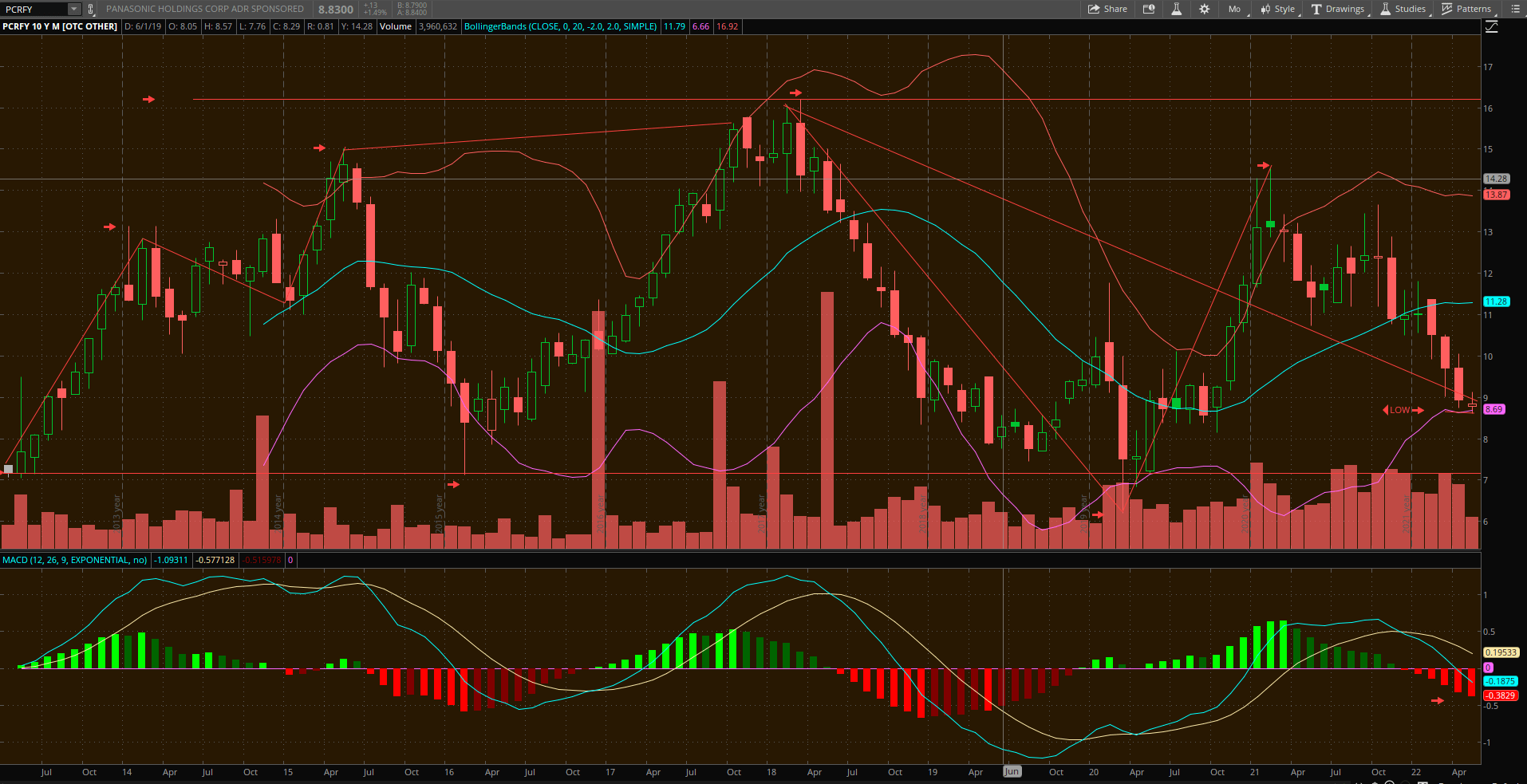

Panasonic Holdings Corporation (OTCPK:PCRFY) known across the world as a manufacturer and purveyor of electronic appliances like refrigerators, washing machines, microwave ovens, and PCs has been focused on emerging global markets since 2010. This appears to have been an important past strategy for developing future growth. As seen in the chart below, that strategy presents a cyclical big picture view of alternating stock valuations across nine years.

Panasonic Corporation Long-Term Monthly Chart

Panasonic Corporation Long-Term Monthly Chart (Thinkorswim Monthly Chart)

Apparent, are cyclic patterns of peaks followed by deep declines that approximate earlier previous lows. Strategically, this suggests that the revenue model is highly sensitive to financial disruptions in the global marketplace that tend to recur in cyclic patterns over years observed in the chart above. The current low is in response to challenging economic conditions like Covid-19 and present world supply chain breakdowns that have severely damaged stock valuations.

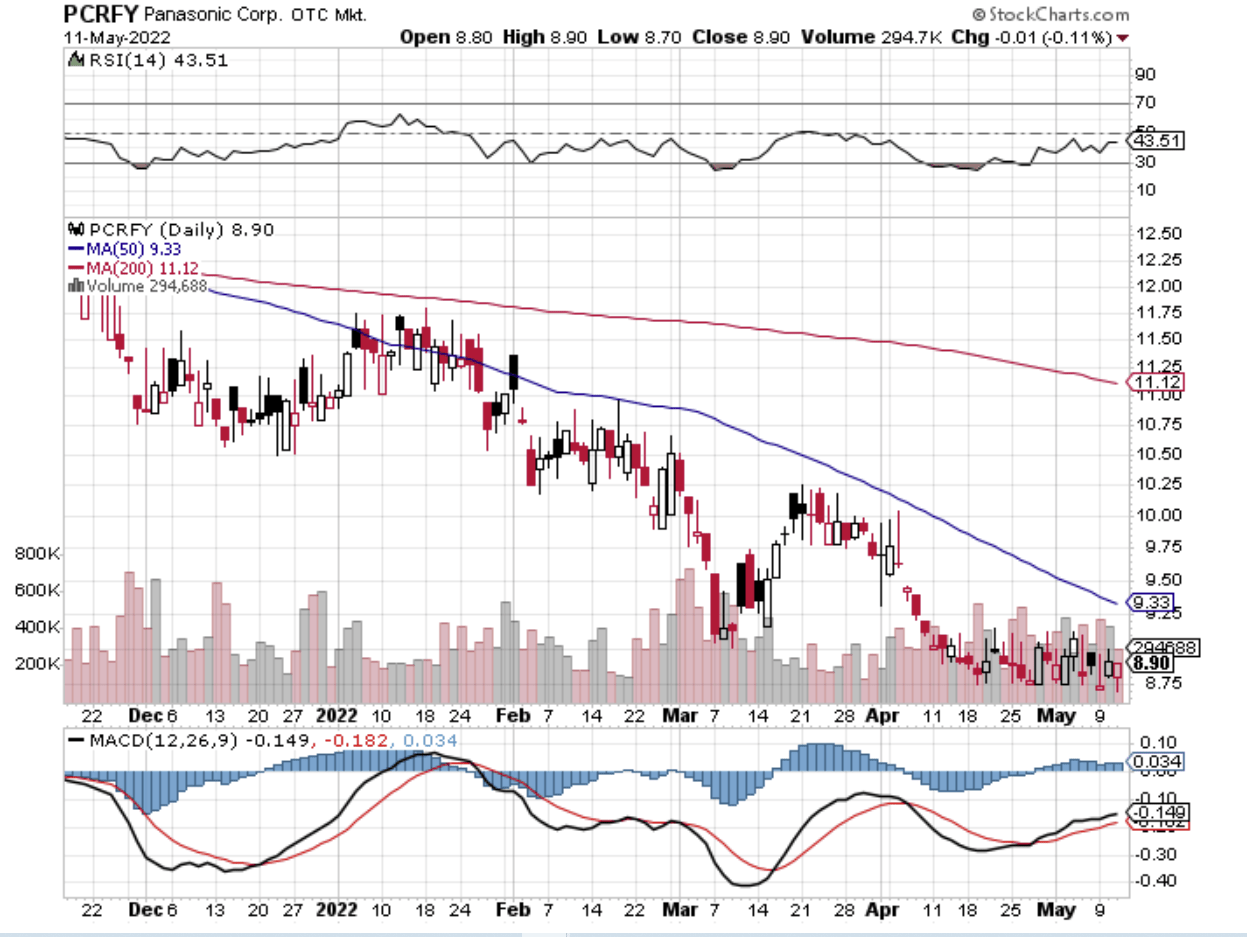

This revenue model is subject to change with a planned expansion in global development of lithium automobile batteries. It is occurring at a time when share value has been deeply discounted in a flat consolidation noted in the day chart below.

Panasonic Day Chart

Panasonic Day Chart (StockCharts)

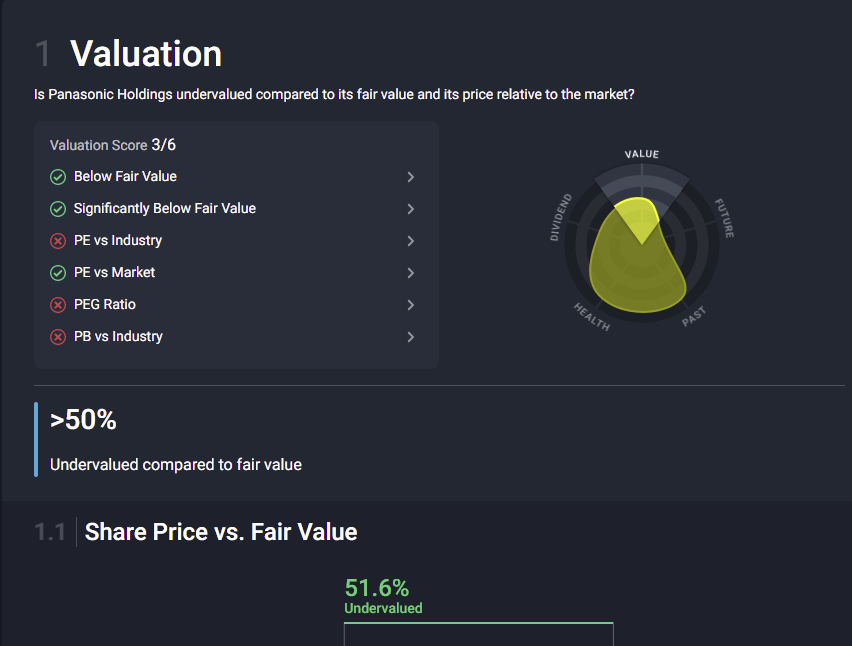

Undervaluation

Not only has the share value plummeted, but as seen in the graphic below, the company is significantly undervalued while participating in a paradigm change in global EV production.

Share price versus fair value is undervalued by 51.6%. Hurt by severely declining global economic conditions, company stock is cheap given the company’s overall inherent valuation. For investors, this spells lower investment risk at a time when Panasonic is prepping to grow electric battery power and distribution for global auto manufacturers planning to produce millions of EVs.

Valuation (Wall Street.com)

Article Thesis

Panasonic is maneuvering into a leading position to produce lithium automotive batteries for the emerging growing world market. Currently, a continued collaboration with TSLA, completion of an improved more powerful electric car battery, and a new gigafactory battery plant to be built in the U.S. near Tesla by 2024 are projects geared to improve future profitability.

I believe this collaboration can change the current financial dynamics that underly the cyclic past patterns for share values and boost them significantly. This is occurring at a time when Panasonic’s share price is attractive in respect to actions the company is now taking.

Second chances may also be viewed as opportunistic. Panasonic is just one example of many previous highflyers that have had share value beaten down in the current marketplace. Going forward, many investors will be watching closely for buyback opportunities. Multiple past bounce-back capability is apparent in this stock’s major upswings following past deep downdrafts. Successes repeat if better circumstance manifest. Experience is also a great teacher.

First Tesla Go-Around

Perhaps an early teaching feature concerned Panasonic’s arrangement with Tesla in 2011 to provide electric car batteries. Panasonic’s overall strategy, at that time, was to take a low-risk position with regard to their partnership. This produced far-reaching effects that limited future growth. During questioning concerning Q3 2011 results, Elon Musk said the following:

Sure, we do have firm pricing from Panasonic. And so, we have very good predictability as to what the price will be over the next four years. We’re not obligated to purchase all of those sales. So, it is profitable for us, if Panasonic becomes uncompetitive, to exit the bill with relatively small penalty.

I wouldn’t mind leasing at first. In fact, since the cars seem to be fixed price, if I could lease first and stay under mileage, I could buy the car after the lease and not be any worse for wear.

Actuality, the Panasonic deal was limited to only 80,000 vehicles during a 6-to-12-month period, but far more cars were in the offing by Tesla. This provided Tesla with the option of future leasing sales. Perhaps this was the first overcautious deal by Panasonic and a missed opportunity unlikely to be repeated in round two. It bears watching.

New Focus Moving Ahead

In spite of a rocky history, including different opinions on prospects for profitability and years of red ink, the company reports that it plans to build a multi-billion-dollar factory in the U.S. and supply Tesla with lithium-ion batteries. This is likely to include Panasonic’s latest larger and more powerful EV battery which is currently being built in Japan with Toyota Motor Corporation (TM).

The 4680 format (46 millimeters wide and 80 millimeters tall) battery is about five times bigger than those currently supplied to Tesla, meaning the U.S. car maker will be able to lower production costs and improve vehicle range. This is a big breakthrough occurring at an optimal time.

Figurative Battery Image

Figurative Battery Image (Getty Images)

Japan’s NHK reports the Japanese company is looking at sites in Oklahoma and Kansas because of their proximity to Texas. In addition, Panasonic is planning to build and mass-produce the new battery for Tesla at its plant in Japan planned for March 2024. Though promising, these are forward-looking two-year projects.

Perhaps, this time around, given past experience with Tesla, Panasonic will find traction by growing itself into a premier global electric car battery company. In my opinion, this pathway can build company growth through global demand at a higher current level than selling appliances. The potential is there, and I believe, if managed properly, it is highly conceivable. Panasonic will have to pull its own weight. Adequate financial health is important for it to bear a greater load of investment than before.

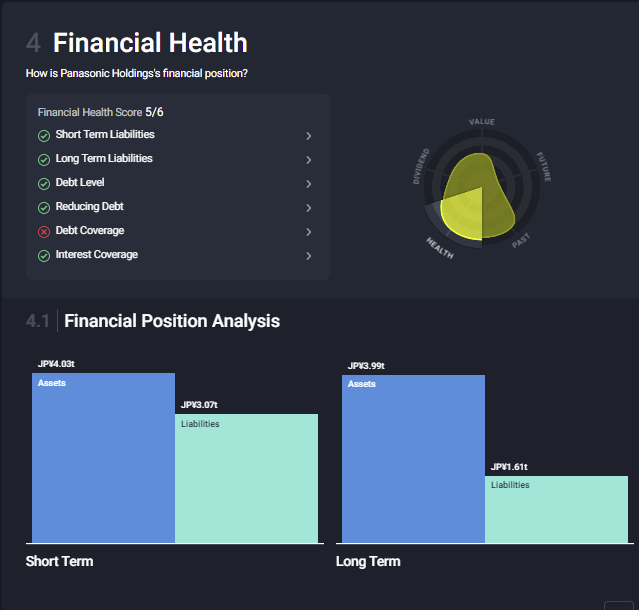

Financial Health

Of these 6 measures of financial health in the chart below, debt coverage is the singular concern. The 5/6 score places the company in a good position to obtain outside financial investment while it develops greater earning power. In addition, long- and short-term assets exceed liabilities which are also strengths.

Financial Health (Simply Wall St)

Annual Dividend

Panasonic also maintains a dividend payment of 2.7%. Though small, it is an additional value purchased with each low-priced share. The dividend is forecast to increase in three years. Any increase in dividend will signal improvement in financial health, but currently, it reflects the divergence between an undervalued stock that is still paying out a dividend. The company maintains a financial position to secure investment and come back changed.

Coming Back

There is a possibility for a burgeoning U.S. electric vehicle consortium moving forward. As American car manufacturers continue to embrace and grow EVs, with continued cooperation between Panasonic and Tesla, and current prospects for a future domestic supply of lithium, there is the opportunity to create a powerhouse combination for future profits. Panasonic is a vital player in that mix.

Such an outcome bodes well as an incentive for investors at a time when the world is experiencing a paradigm shift into electric-powered cars and trucks. So, take notice of Panasonic stock that is currently undervalued during this stock market downdraft, and monitor Panasonic’s growing involvement in the paradigm shift.

All conditions are subject to future change. Second chances may also be viewed as previously missed opportunities. Panasonic is just one example of many previous highflyers that have had their share value beaten down in the current marketplace. However, to deal with that outcome, the company has engaged in a program of restructuring by reducing overall global markets from 50 to 15-20 that have growth potential. This is an excellent restructuring to gain needed for financial traction.

Going forward, many investors will be watching closely for buyback opportunities. Multiple past bounce-back capability is apparent in this stock’s major upswings following past deep downdrafts. Successes repeat if better circumstance manifest. At its current stock price, Panasonic is worth watching.

Watch Time

The next two years are a critical time for Panasonic. I believe change is certain; what it will be is now in the making. Reconnection of important global supply chains and some decline in current inflationary pressures can also re-energize company sales for their new growth-oriented business sectors. Increased revenues and earnings can provide additional financial capital for growth, while a continued global transformation into batteries that drive cars and trucks portends considerable opportunities for broadly increasing EV battery production and sales. All spell future profitability.

This possible outcome bodes well as an incentive for investors at a time when the world is experiencing a paradigm shift into electric-powered cars and trucks. So, take notice, during this stock market downdraft.

I will be watching the process like a hawk and ready to share future evidence in support of my thesis.

Wrap Up

Panasonic is a vast globally experienced company that is in the process of re-orientation to focus on productive strengths. A focus on growing new markets to increase share value is mandatory. It needs to shed the image of the world’s appliance salesman for the automotive powerhouse it is becoming. What it does during the next two years is critical to the company’s future.

The potential global growth curve for EVs is gargantuan, and that makes the battery component financially viable. Plans for the coming two years are vital, and every effort must be made to find ways to work with Tesla and others to capitalize in that growing market that is changing the landscape. In my opinion, the relationship between both companies must and will expand and flourish. Panasonic’s relationships with other carmakers are also important to this partnership.

More than 100 years old, Panasonic does not lack future vision. Though poised for further breakthroughs in the automobile energy sector, it maintains a ten-year vision embracing a broad range of new emerging technologies. Continued growth and transition into more profitable ventures await. There are many reasonable possibilities in the making. It’s on my watchlist.