bjdlzx

(Note: This article appeared in the newsletter on June 11, 2022 and has been updated as needed.)

Athabasca Oil (OTCPK:ATHOF, ATH:CA) has been waiting for a time when management could reduce the debt load made from some acquisitions a few years ago. Now that opportunity presents itself and not a moment too soon either. The latest round of financing cost more than 9% in interest even with a second lien as protection and some warrants as well. Furthermore, the company has a provision to direct three-fourths of its free cash flow (as defined in the agreement) to the repayment of this debt until a certain amount has been redeemed. Investors have more than average risk just investing in a thermal operation in the first place. Therefore, the reduction of debt will reduce the operating leverage as well as the financial risk associated with that leverage.

Thermal producers usually have fairly high production costs. This company is no exception.

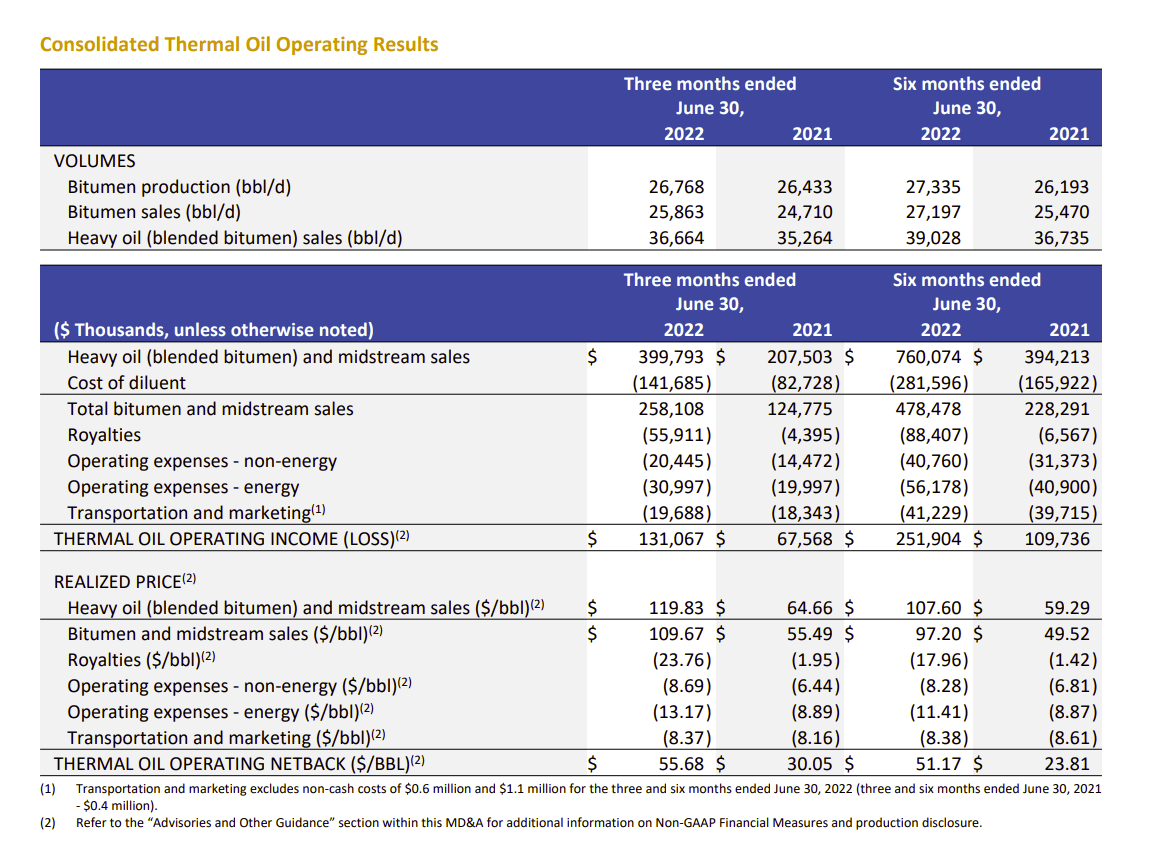

Athabasca Oil Thermal Operating Results (Athabasca Oil Second Quarter 2022, Management Discussion And Analysis.)

As shown above, the operating expenses are tremendous compared to the unconventional business. Management often focuses on the wonderful margin. But there is not enough of the product produced for decent cash flow given the debt levels unless selling prices are at robust levels. That is the main reason for the high interest rate and the warrants.

Furthermore, transportation costs are higher, and the product needs to be blended with condensate in order to flow through the pipelines to market. Since the sales price is discounted from the more desirable light oil, the breakeven WTI price for thermal product is often pretty high. It can become higher when (as is often the case) the discount widens during the periodic industry downturns.

Management is projecting that the company should have a net cash position by yearend. That would certainly help the situation tremendously. Management tends to maintain a large cash position so that there is no need to use the credit line during hostile industry conditions and so there is adequate liquidity to shut-in production should that become necessary during those times of weak commodity prices.

This management also tends to buy and sell projects. The cash position lets sellers know that management is able to execute transactions because the cash is available.

Light Oil

Athabasca needs cash flow during the industry downturn part of the business cycle. In fiscal year 2020, for example, production was shut-in when it no longer produced positive cash flow. This is what makes it so difficult for thermal producers to survive as standalone upstream companies.

This company has a joint venture that produces light oil. That joint venture offers the promise of decent cash flow during downturns once development is sufficient to provide that cash flow.

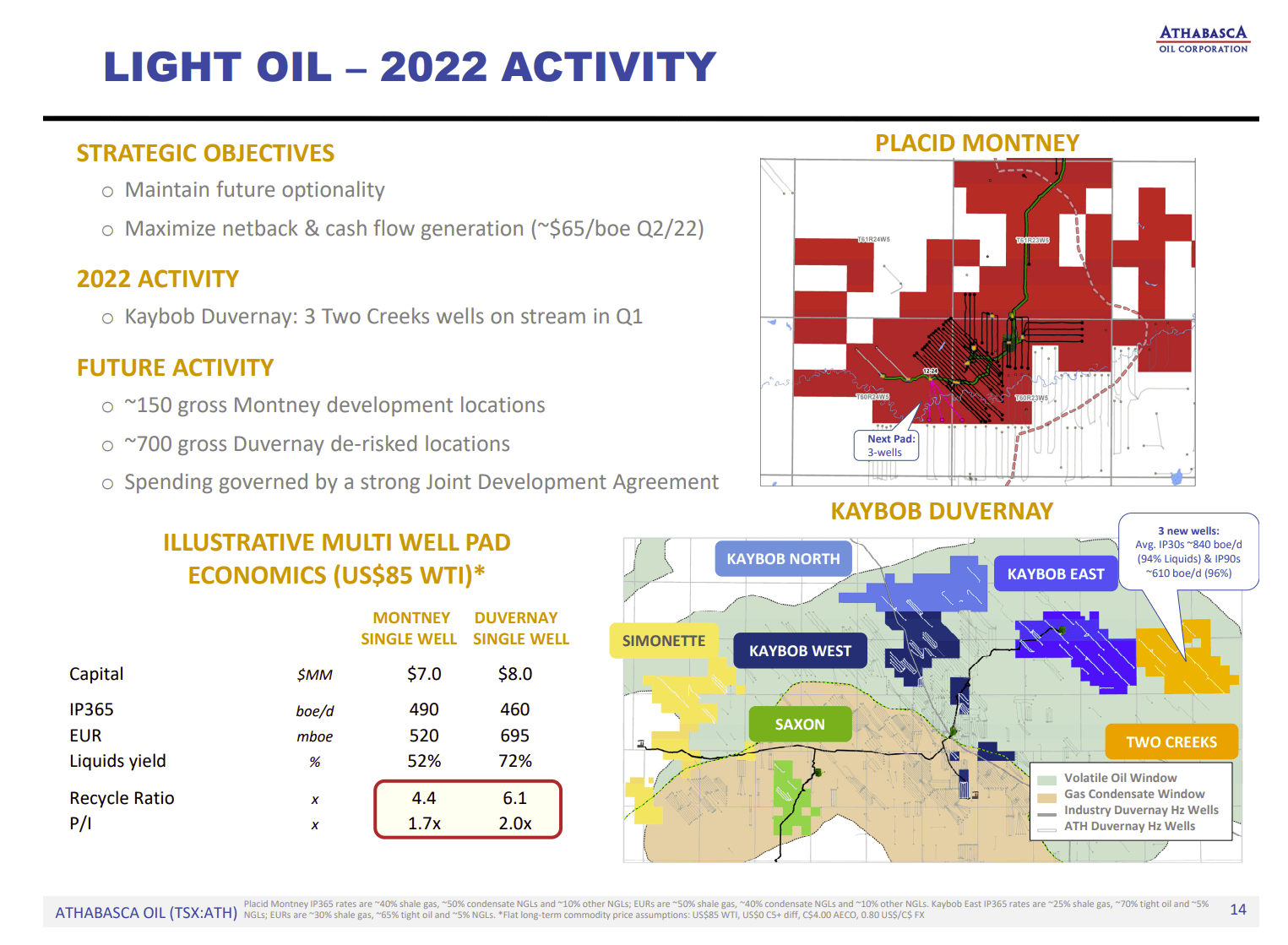

Athabasca Oil Second Quarter 2022, Update Of Light Oil Business (Athabasca Oil Corporate Presentation Second Quarter 2022.)

The costs are much lower for this joint venture project, so the profitability shown above is a lot better. The production selling price is not discounted as is the case with the thermal product. Therefore, the WTI breakeven is lower, there is no widening of a discount to worry about, and the cash flow during cyclical downturns is reliable (compared to thermal).

Both partners are currently working on getting the well costs down before this project goes into “production mode.” Therefore, production growth will be on the slow side or maybe nonexistent, until the partners determine that the well costs are satisfactory.

The well design has resulted in much better initial flow rates and overall production per well. So, some cost progress has been made. But it is also clear that more work needs to be done.

Partner’s View

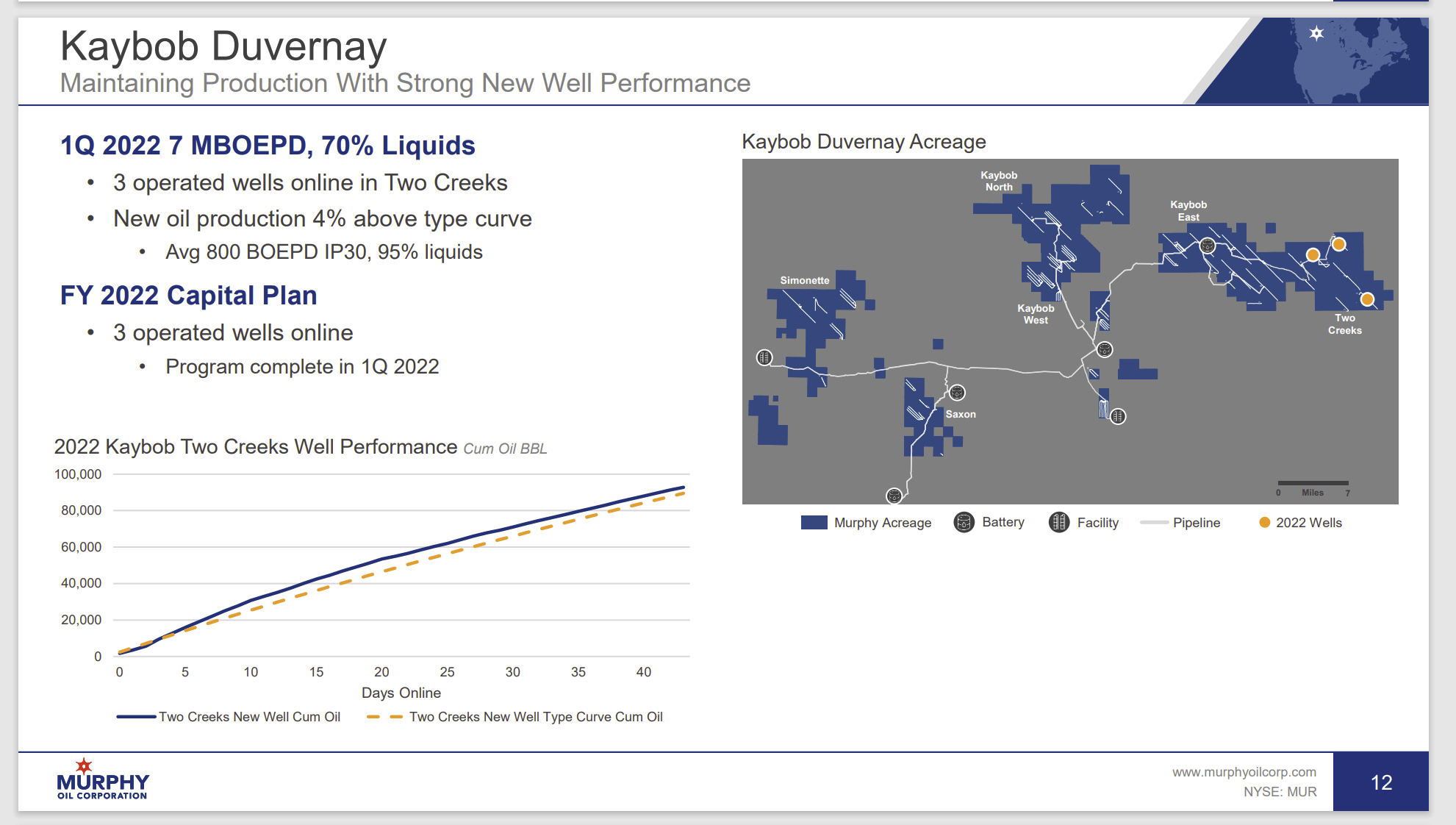

Small companies often need some additional credibility in this industry. In this case, that additional credibility comes from having Murphy Oil (MUR) as a partner in the light oil project. Here is Murphy’s view of the project from the first quarter slide presentation:

Murphy Oil Report Of Operated Joint Venture Progress (Murphy Oil Corporate Slide Presentation First Quarter 2022.)

Murphy operates some of the acreage and Athabasca Oil operates the rest. Having a well-established partner like Murphy with which to share information helps Athabasca Oil gain a credibility it might otherwise not have. The partnership also speeds the process of finding the most cost-efficient method with which to develop this project.

The current environment is likely to provide both partners with more free cash that they can use to optimize the operations. That is important to Athabasca Oil because the company needs the cash it gets now during industry downturns.

There is always the risk to a thermal producer of an extended downturn that results in no cash flow from the thermal operation. Therefore, it is essential that a thermal producer that wants to remain independent has a low-cost upstream operation. Clearly Athabasca has that operation. Now it needs to get that joint venture to the correct size to assure no financial stress during cyclical downturns.

Summary

Athabasca Oil is a leveraged thermal producer with an edge. That edge consists of a joint venture with a well-established industry producer for light oil production. Management also has the advantage of using the current robust commodity price environment to reduce debt as much as possible.

So many times, thermal oil produces insufficient or even no cash flow during industry downturns. Therefore, it is probably optimal for the company to have no debt at all “just in case.” Management appears to recognize this by agreeing to repay debt at a relatively rapid pace.

Still, this company is not a low-cost producer. Therefore, earnings will probably not be valued as highly as the more profitable competitors. The light oil joint venture does provide a future possibility of a more profitable production mix. Therefore, stock valuation related to earnings could improve as the joint venture progresses.

As long as there is substantial debt, this company is probably only for more venturesome investors. Conservative investors need not consider this company. Canadian prices tend to be far cheaper than United States prices, so there could be a purchase of some existing light oil production in the future.

Costs are improving at the thermal projects. But this company has a long way to go to match the thermal costs of industry leaders like Cenovus Energy (CVE). Investors need to view this company as a “work in progress” with a fair amount of work yet to be done.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.