Diego Thomazini

B. Riley Financial (NASDAQ:RILY) is a diversified financial services firm that I’ve pitched as a good buy at various points in the past.

The company generates revenue from investment banking and capital markets advisory services as well as small cap equity research, wealth management, restructuring advising, retail liquidation, real estate advising, fixed income advising, ownership of several retail brands and communications companies, and its own investment book.

RILY was a huge winner in 2021, as low corporate bond yields and a red-hot equity market produced ample opportunities for the company to offer its investment banking services. But this year, as the stock market has swooned and bond yields have surged, RILY’s core capital markets advisory business has pulled back.

Most recently, investors witnessed this disturbing press release concerning RILY’s second quarter 2022 earnings:

Seeking Alpha

Negative $4.36 per share in earnings? This is obviously a very bad sign, if it accurately reflects RILY’s profitability. If RILY is generating deeply negative earnings and burning cash, the company won’t survive for long – to mention nothing about the $4 per share annual dividend!

Luckily, the above negative EPS number does not accurately reflect RILY’s financial situation or results. Rather, it is a result of accounting measurements surrounding its equity and debt investment portfolio that severely skew its results.

So, let’s dive into RILY’s second quarter results to assess the company’s prospects as well as the safety of its 7.2%-yielding dividend.

1. Accounting Metrics Skew Results

As briefly mentioned above, RILY has its own investment book of publicly traded equities, corporate bonds, and other investments. When a public company owns a portfolio of stocks and bonds, the shift in market value of these securities needs to be accounted for in order to come to an accurate valuation of the company as a whole.

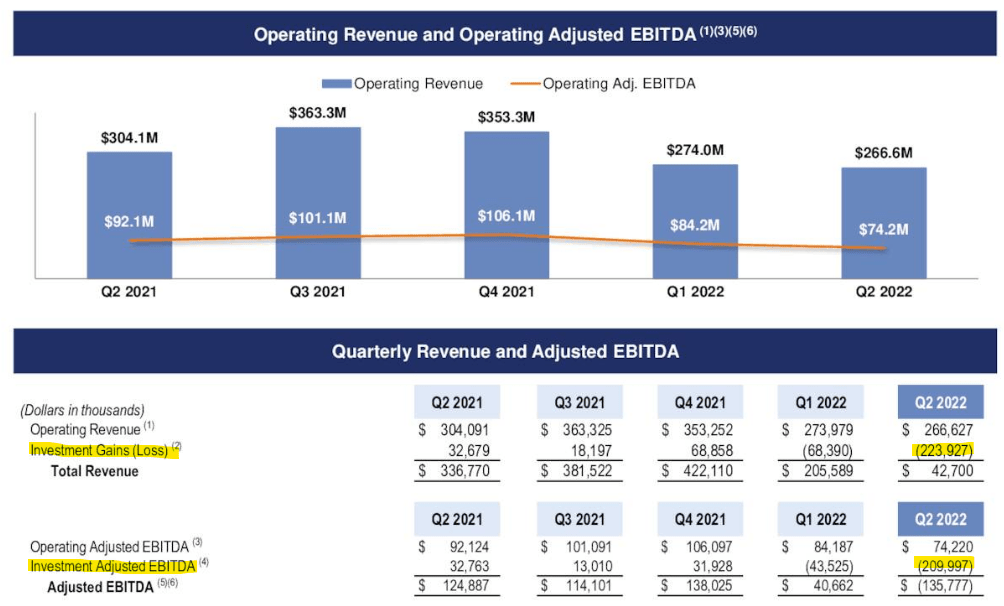

Hence we find that though RILY’s operating revenue and EBITDA have held up even after the boom times of 2021 passed, “investment” revenue and EBITDA have turned negative as the market values of its stocks and bonds have fallen this year.

RILY Presentation

The “investment” segment refers to (mostly unrealized) gains or losses on RILY’s investments and loans based on fair value adjustments. It also includes trading income or losses, but trading is relatively small compared to the big swings in value of its investment portfolio.

As CEO Bryant Riley explained on the Q2 2022 conference call, these downward fair value adjustments “are mostly unrealized and correlate to market contraction.” In other words, they do not indicate weakness in RILY’s performance in particular so much as weakness in the performance of the stock and bond markets generally.

As you can see in the image below, the bulk of the decline in fair market value of securities came from RILY’s equities portfolio. Secondarily, a decline in the fair market value of RILY’s corporate bond portfolio likewise added to RILY’s unrealized investment losses.

RILY Presentation

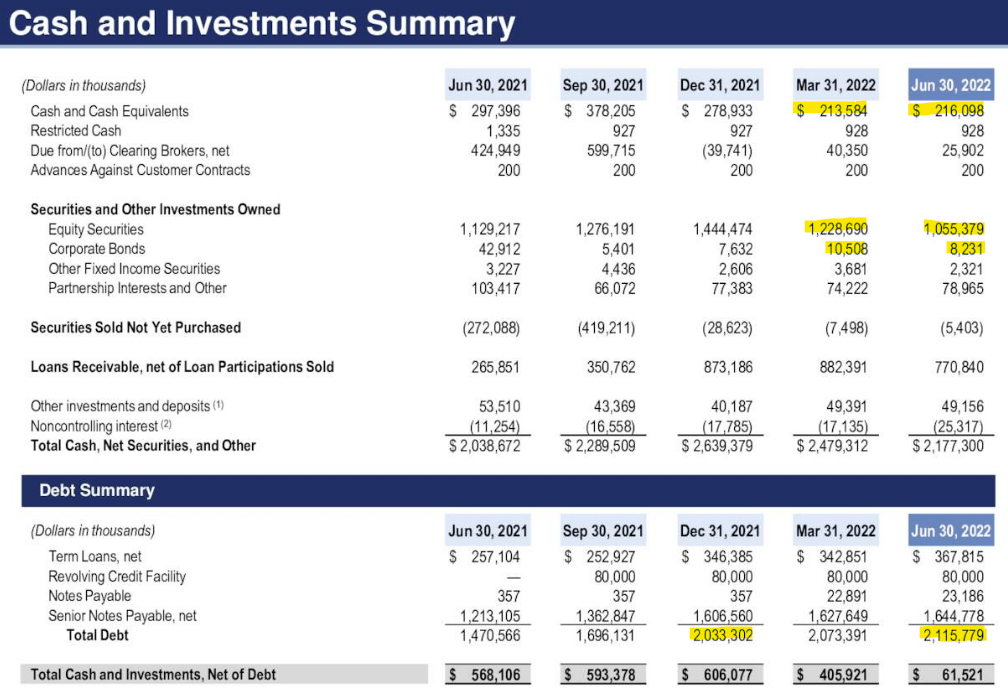

While total debt did tick up by 2% and total cash & investments declined 12.2% from Q1 to Q2, it’s important to note that total cash, marketable securities, and other investments on the balance sheet still exceed total debt by $61.5 million.

In other words, even assigning zero value whatsoever to the financial services segment (RILY’s core revenue generator!), shareholders would still come out with $61.5 million, or about $2.19 per share, of value in a total liquidation scenario. As recently as the end of 2021, RILY’s liquidation value was above $21.50 – again without assigning any value at all to the financial services part of the business.

What’s more, after two consecutive quarters of negative earnings, note that total debt has only risen 4.1%.

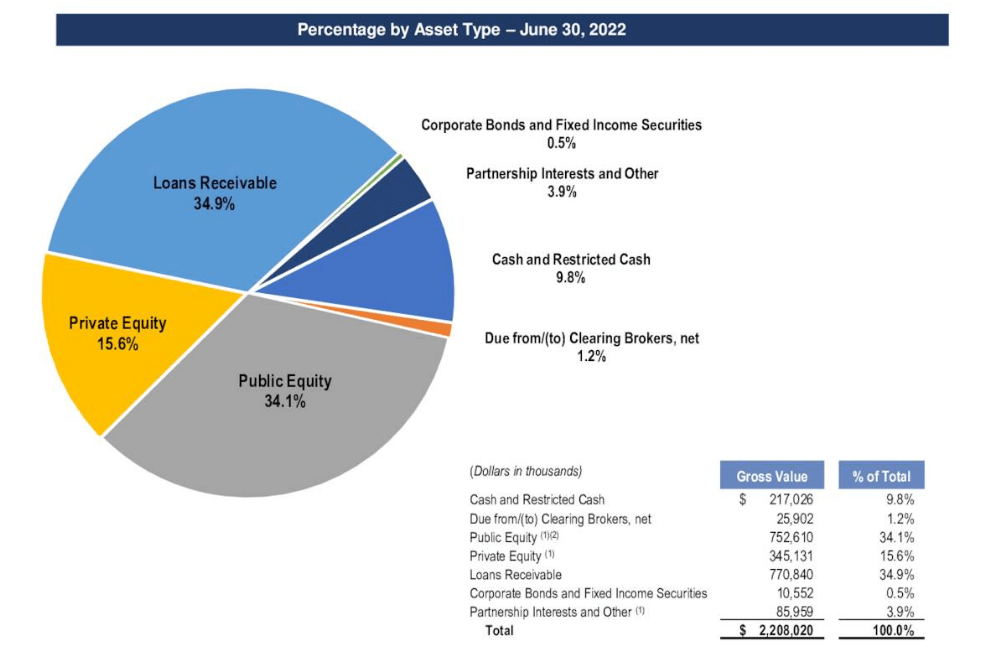

Here’s a clearer breakdown of RILY’s investment assets:

RILY Presentation

When combining RILY’s cash position, marketable securities, and other investments, the company has no net debt. It is impressive to see a company with no net debt generate the kind of operating EBITDA that RILY does.

2. Revenue Is Down But Not Out

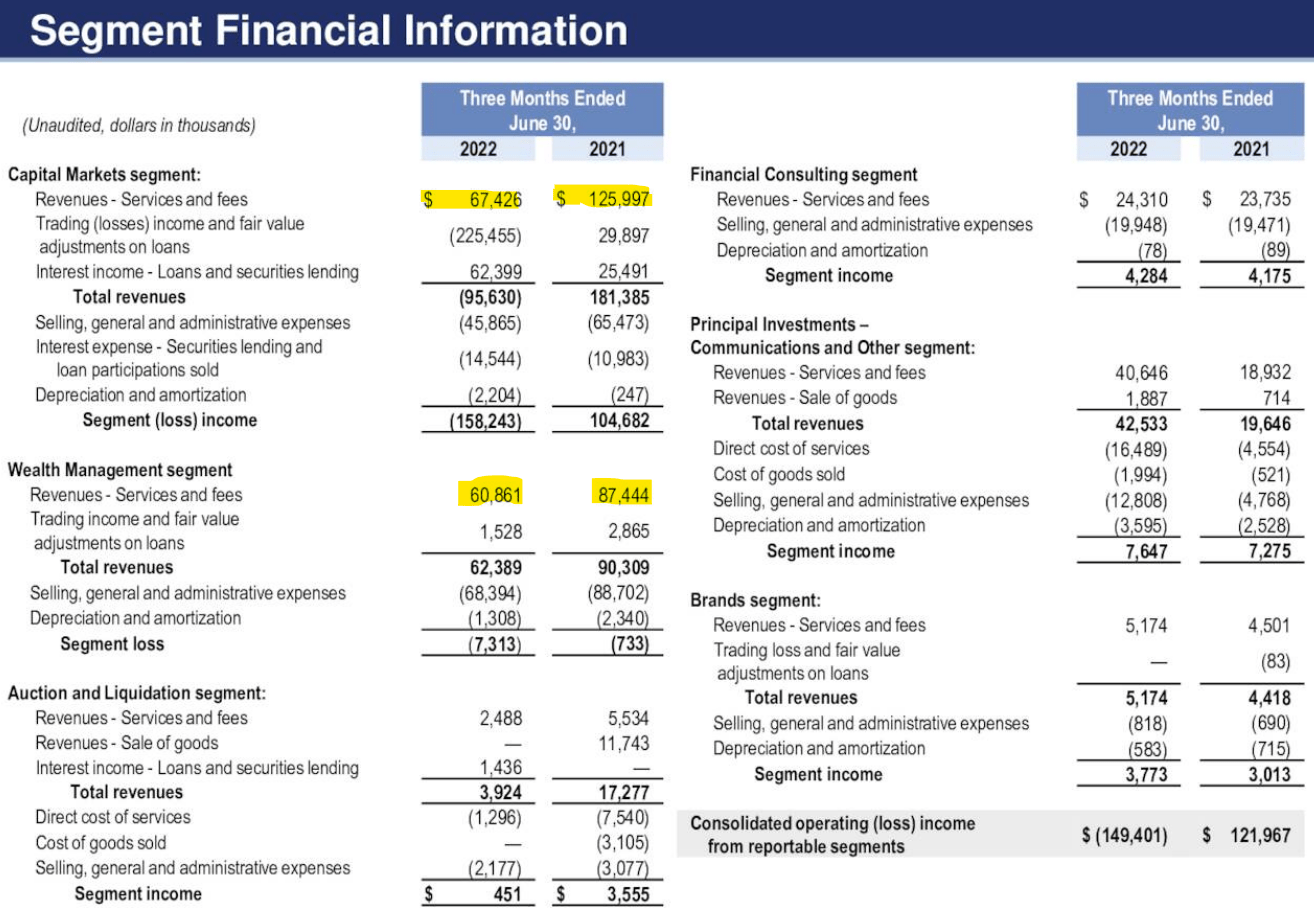

Revenue from RILY’s core financial services business segment, which includes investment banking, financial consulting, and real estate advisory services, did decline from $266.1 million in Q2 2021 to $200.9 million in Q2 2022. The bulk of that decline in services revenue came from the Capital Markets segment, which saw services and fees revenue roughly half from Q2 2021.

RILY Presentation

This should not be surprising, given that financial conditions for capital markets were significantly worse in the second quarter of this year than they were in the second quarter of last year. Public companies are not issuing as much equity because stock prices are lower. Nor are they issuing as much debt because interest rates are much higher.

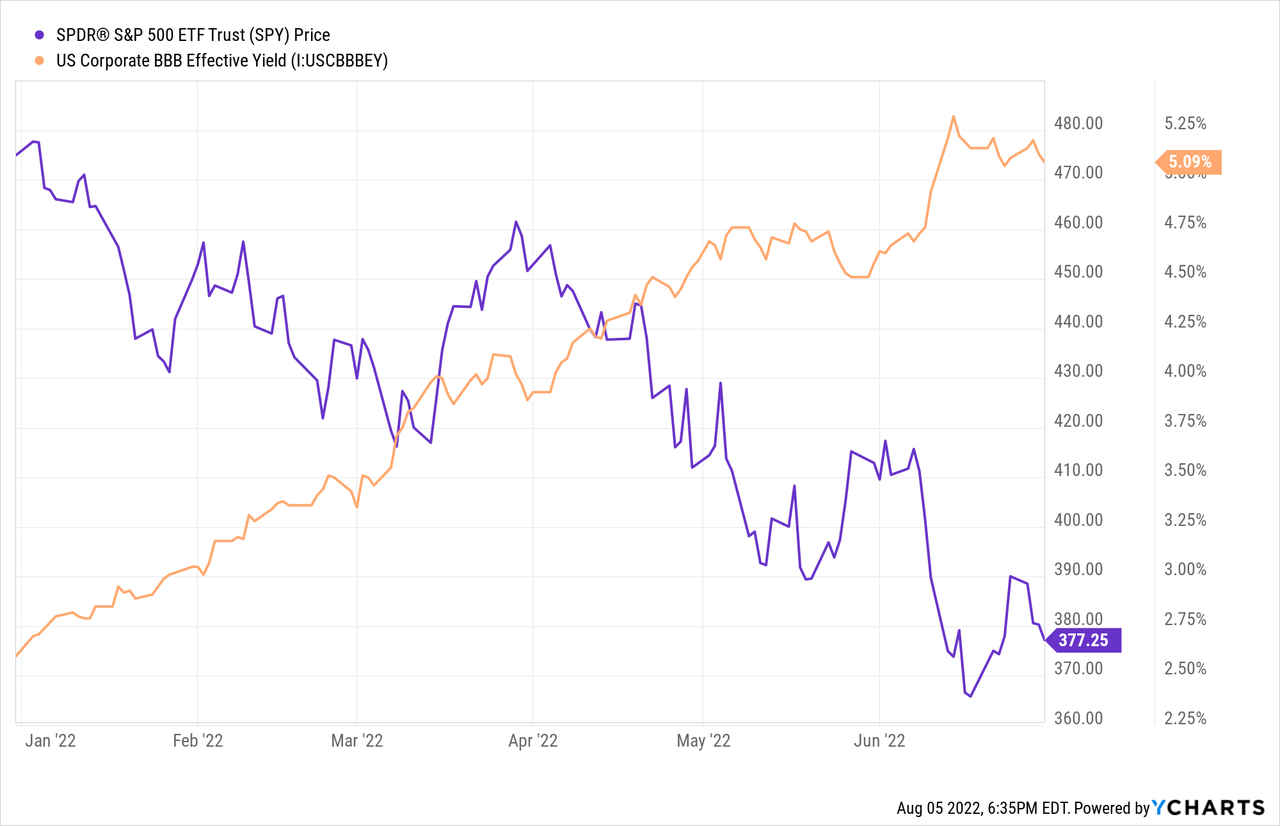

From the beginning of the year through the end of June, the S&P 500 (SPY) shed 20% of its value, while BBB corporate interest rates roughly doubled from just over 2.5% to over 5%.

This environment was obviously not conducive to heavy capital markets activity!

But the second quarter may have marked the bottom for capital markets, as the Federal Reserve has shown some signs of being close to a pivot and the stock market has rebounded. Riley commented on the conference call:

Being able to generate the operating results that we did during another quarter without capital markets is extremely gratifying for us. And since quarter end, we have recovered some of the investment losses that we reported as the market has come back a bit.

3. The Dividend Remains Safe – For Now

RILY’s $1 per share quarterly dividend amounted to a little over $28 million in the second quarter.

Omitting the unrealized investment losses, I calculate RILY’s Q2 operating income to be around $76 million. Taking out $31.7 million in corporate-level interest expense, I then get to $44.3 million of profit before taxes. Because of investment losses and other tax deductions, RILY will have no income taxes due for the second quarter.

Thus, I estimate that RILY’s cash profit in the second quarter to be around $44 million, which is more than enough to cover the $28 million dividend while leaving about $16 million available to invest in whatever investment opportunities RILY’s management team deems most attractive.

That includes stock buybacks, in which RILY has been engaging all year. Weighted average diluted shares outstanding fell from 28.67 million in Q2 2021 to 28.05 million in Q2 2022.

What’s more, as RILY continues to build up its less cyclical business segments, it should continue to generate a foundation of stable, recurring cash flow to support the dividend. Here’s Bryant Riley from the Q2 conference call:

The relative contribution from our less cyclical and less episodic businesses have meaningfully grown with the entire Riley platform generating $366 million of operating EBITDA over the trailing 12 months compared to $114 million of operating EBITDA in 2019. With increasing contributions from less cyclical and less episodic businesses exceeding the capital needed to support our dividend, we continue to have flexibility to invest across our businesses. To that end, we are pleased to deliver our shareholders $1 dividend for the quarter.

What’s more, if and when capital markets become more friendly, RILY’s cash profit generation and dividend both have ample upside. It is important to remember that bear markets, such as the one we are in now, only occur about 5% of the time. The other 95% of the time, bull markets reign. And during those times, RILY should thrive.

Here’s Riley again:

Looking ahead, we are encouraged by the opportunity to increase that dividend [as] capital markets return and become more normalized and they will normalize. We have seen cycles like this many times over the course of B. Riley’s 25-year history and each time we have come out on the other side [more] strongly than before.

Bottom Line

RILY is one of my favorite financial stocks, not least of which because founder and CEO Bryant Riley has a huge amount of skin in the game. The vast majority of Riley’s wealth (not to mention his name!) is tied up in RILY, and his leadership has proven skillful as the firm has gobbled up numerous other financial services companies in order to form the diversified company RILY is today.

Complicated accounting creates a somewhat misleading picture, causing investors to perceive at first glance that RILY is losing money and burning cash – that it isn’t profitable at all. While operating income for RILY’s core revenue generation business is certainly lower this year than it was last year, the business is still profitable.

The headline negative earnings number is a result of fair market value declines in RILY’s securities portfolio, but that does not necessarily represent a permanent loss. Just as with your own investment portfolio, a paper (unrealized) loss on a stock or bond holding does not represent a real loss unless it is realized by selling it at a price lower than one’s cost basis.

The dividend remains safe for now, although market conditions could certainly worsen from here enough to threaten the $1 per share quarterly payout.

As such, RILY and its 7.2% dividend yield look attractive for the income investor willing to accept somewhat above-average risk.