Hammad Khan/iStock via Getty Images

Introduction

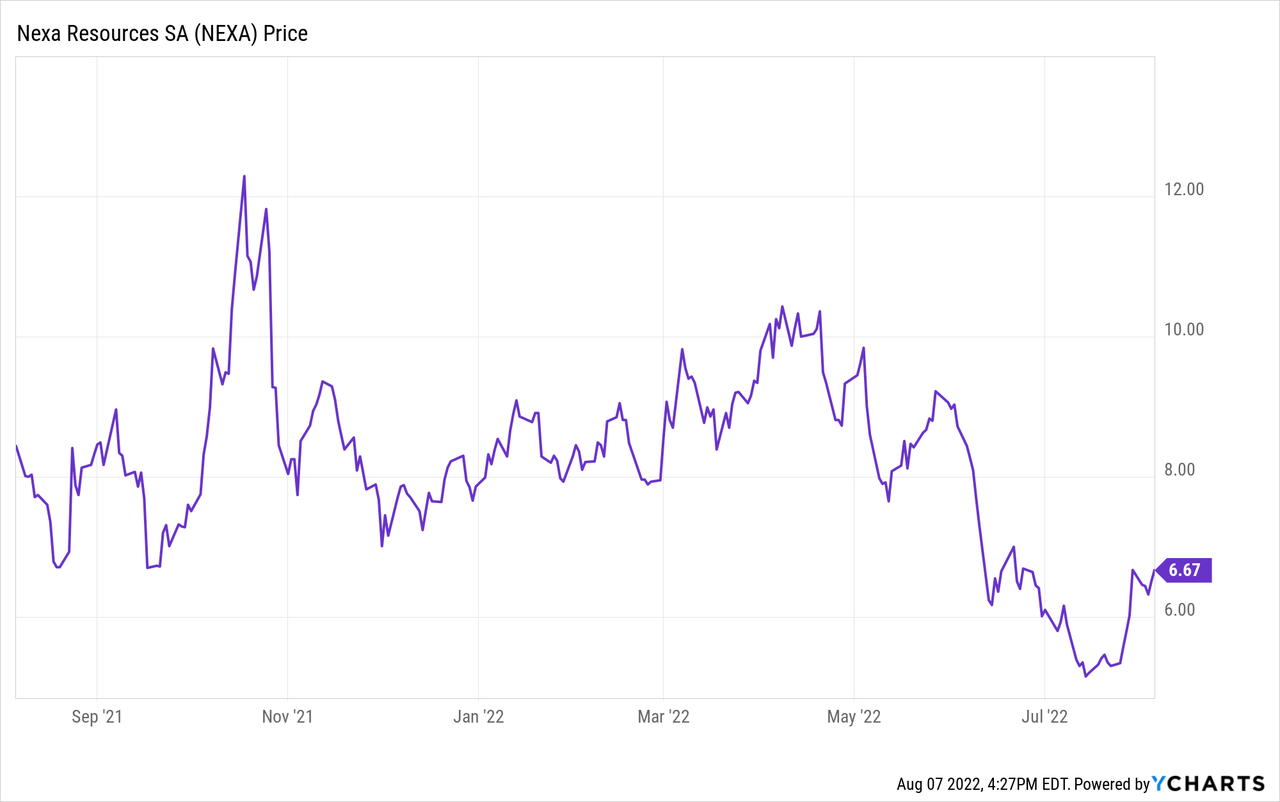

Since my previous article on Nexa Resources (NYSE:NEXA) about 1.5 years ago, the share price has lost about 40%. This is surprising considering that the zinc price increased by more than 50% and is currently still approximately 20-25% higher than in February 2021. Additionally, Nexa just completed the construction of a new mine which means the capex will decrease to just the sustaining capex while the new mine will contribute to the operating cash flow. If the zinc price remains at this level, Nexa Resources will be a true cash cow.

The first half of the year was strong, thanks to the high zinc price

Nexa is a relatively large zinc producer. An important feature of Nexa is that the company owns zinc smelters as well which means the company offers some vertical integration which helps to keep the ‘loss’ to middle men low. About 50% of the throughput of the smelters came from its own mines while the other half was delivered by third parties. With a total smelter production of in excess of 300 million pounds of zinc in the first half of the year (thanks to a strong second quarter) while the company also produce copper (over 35M pounds), lead (about 60 million pounds), silver (4.8 million ounces) and some gold (13,200 ounces) in the first semester, Nexa is off to a good start.

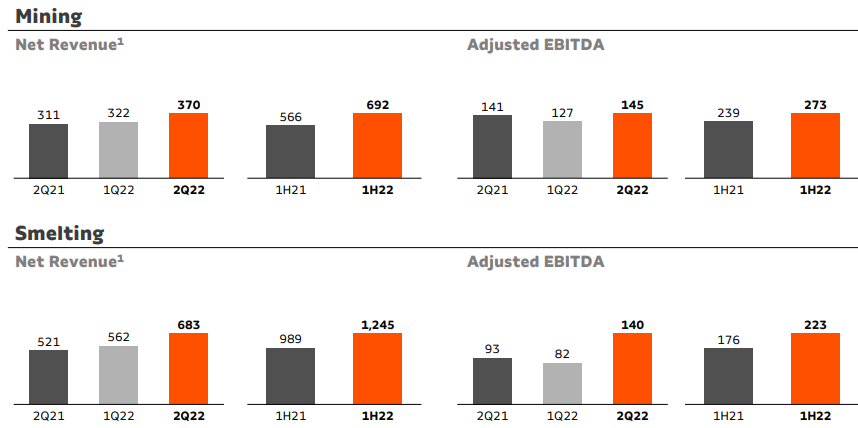

This also means we should not look at Nexa as ‘just’ a mining company as the EBITDA contribution from the smelting segment is definitely not negligible: in the first half of this year, 45% of the EBITDA was actually generated in the smelting division, as you can see below.

Nexa Investor Relations

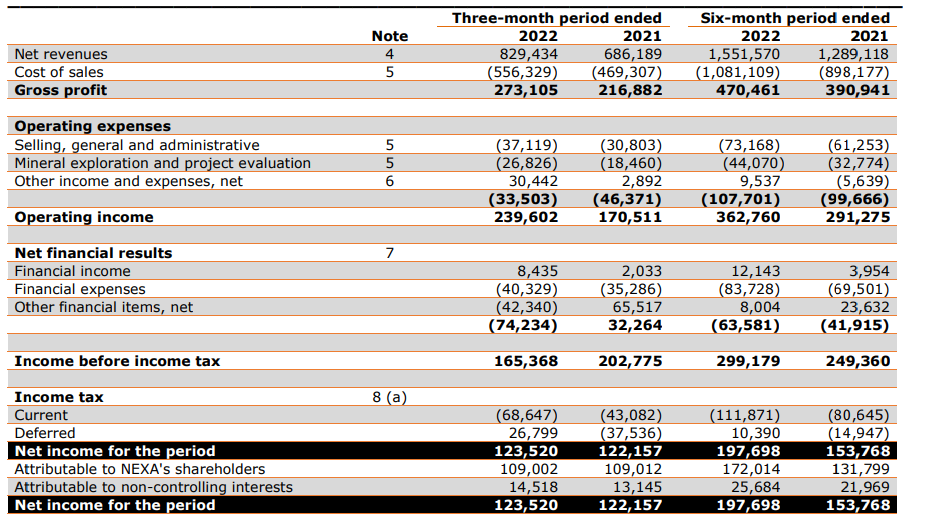

In the first half of the year, Nexa reported a total revenue of $1.55B, resulting in a gross profit of just over $470M. As you notice, even during the first six months of last year the gross profit remained pretty strong, thanks to the smelting activities providing a strong backbone to the company as a whole.

The total operating income increased to $363M despite a sharp increase in the exploration expenditures as Nexa continues to explore on either new projects as well as on the existing mines for both infill drilling and resource expansion drilling.

Nexa Investor Relations

The net income came in at $198M of which about $172M was attributable to the shareholders of Nexa. This results in an EPS of $1.3 in the first half of the year. So on an annualized basis, Nexa is indeed trading at just around 2.5 times the earnings.

As Nexa has in excess of $1B in net debt, the cash flows are also very important. The company reported an operating cash flow of $289M in the first half of the year, but this includes almost $180M in working capital-related items and excludes the $63M in interest and lease payments as well as the approximately $102M in taxes owed (versus just $79M in taxes paid). This means the adjusted operating cash flow in the first semester was approximately $305M.

Nexa Investor Relations

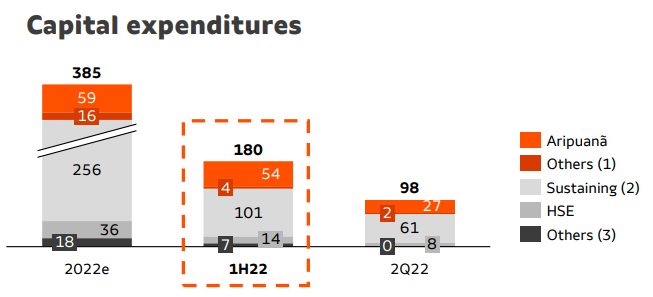

The total capex was $182M resulting in a free cash flow of $123M and even if you would deduct the $26M in net income attributable to non-controlling interests, Nexa’s H1 free cash flow was very strong with approximately $97M.

This may sound surprisingly low, but the cash flow statement does not split up growth capex and sustaining capex. The corporate presentation does provide a more detailed breakdown, and there we see about $58M of the capex was spent on Aripuana (the new mine) and other growth initiatives. We also see the full-year sustaining capex will be around $315M ($385M minus the Aripuana and other capex) for an average of around $80M per quarter.

Nexa Investor Relations

This means the sustaining free cash flow in the first half of the year was approximately $157M. However, applying the expected average sustaining capex per quarter for this year, the adjusted and normalized free cash flow was approximately $117M in H1. Divided over just under 132M shares outstanding, the free cash flow per share was $0.89. Definitely good enough to make some heads turn.

The balance sheet should now get safer fast thanks to the completion of the new mine

While the zinc price remains volatile, Nexa has one ace up its sleeve. The construction of the Aripuana zinc mine in Brazil is now pretty much complete, and the project will stop being a cash drain and will become a net cash contributor over the next few quarters as production ramps up to nameplate capacity. This ramp-up will take time. Nexa anticipates Aripuana will run at 30-40% of capacity by the end of Q3 and 70-80% of capacity by the end of this year before moving to 100% in the first half of next year.

As a reminder, Aripuana will produce in excess of 150 million pounds of zinc, over 50 million pounds of lead, 9 million pounds of copper, 14,500 ounces of gold and 1.8 million ounces of silver per year over an initial 11-year mine life. And although there were some cost overruns pushing the total capex to $625M, the mine is now a ‘sunk cost’ and we should look at Aripuana on a ‘going forward’ basis. And with an anticipated cash cost of $0.21 per pound of zinc, the project should do well in the current price environment.

The contribution from the new Aripuana mine from next year on also means Nexa’s net debt and debt ratios will improve dramatically.

Nexa Investor Relations

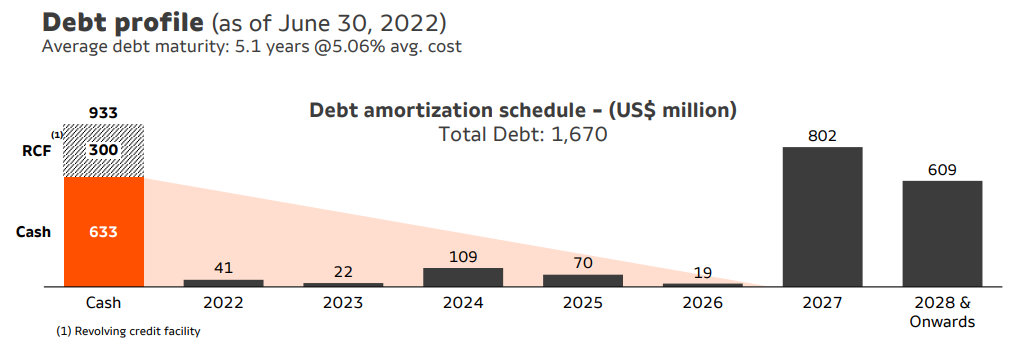

There is absolutely no rush as the majority of the debt consists of two bonds which are still about 5 years away from the maturity date. As you can see below, virtually no debt is due before 2027.

Nexa Investor Relations

Meanwhile, the incoming free cash flow will further boost the cash position (and reduce the net debt) while the Aripuana-mine will also start contributing to the EBITDA, which means the debt ratio will improve from both sides of the equation: a lower net debt and an increasing EBITDA.

Investment thesis

There may still be some volatility in the next few quarters as the zinc price has been pretty volatile. But based on the Q2 results, Nexa is cheap, even if we use a zinc price 15-20% lower than the realized zinc price in Q2. And that excludes the contribution from the new Aripuana mine, which is currently being commissioned. Nexa seems to be in no rush to deploy the incoming cash flow as on the conference call, management confirmed it is ‘looking for projects similar to Aripuana’ while it is also working on some other projects in its portfolio.

Nexa will host an Investor Day in New York in October, and we will likely see a multi-year plan presented by the company at that time.

I have a long position in Nexa and have written some put options that are currently in the money as I would like to build up my position ahead of the market realizing the balance sheet will rapidly and substantially improve thanks to the strong cash inflow. I am surprised the share price is now trading 40% below its February 2021 level as the zinc price is higher and a whole new mine is about to be commissioned in the current zinc price climate.