portishead1/E+ via Getty Images

The last time I wrote on Summit Midstream Partners, LP (NYSE:SMLP), was back on March 8, 2022, by writing – A Granular Look At Its (Super) Conservative FY 2022 Guidance. Lo and behold, on August 4, 2022, Summit reported its Q2 FY 2022 numbers and updated its full year guidance. As of August 4th, Summit now expects its FY 2022 Adj. EBITDA to be at the high-end of its guidance range, or closer to $220 million.

Based on year-to-date financial results and the timing and performance of recent well connections in 2022, we believe we will trend toward the high end of our previously announced Adjusted EBITDA guidance range of $205 to $220 million. We continue to see strong momentum behind our systems throughout the second half of 2022 and into 2023 which we believe positions SMLP for strong growth in 2023.

(Updated Management Guidance – August 4, 2022)

For perspective, back on February 25, 2022, Summit’s management said the following about FY 2022 guidance.

Providing 2022 adjusted EBITDA guidance of $195 million to $220 million based on 75 to 110 new well connections and total capital expenditure guidance of $20 million to $35 million, excluding $10 million of Double E capex.

(Initial FY 2022 Management Guidance – February 25, 2022)

This conservative guidance really caught Mr. Market off guard and SMLP units crashed on February 25, 2022, closing down 30.6%. With very limited sell side coverage or sponsorship combined with a large and diffuse retail ownership, sentiment got super negative and SMLP units drifted under $14 (on March 16, 2022). In other words, many people just ‘gave up’ and capitulated.

On May 3, 2022, SMLP reported a solid Q1 FY 2022 quarter, and was very upbeat on its conference call. SMLP units rebounded smartly, briefly trading north of $21 (on May 4 – May 6th). Incidentally, on May 31, 2022, RBC downgraded SMLP. I got a copy of the RBC report and was really surprised to learn they were modeling both FY 2022 and FY 2023 Adj. EBITDA at only $205 million.

As we know now, SMLP’s management is telling the market they think FY 2022 Adj. EBITDA will be closer to $220 million. Moreover, given their active and upbeat discussions with producers behind its systems, management said the following about FY 2023.

While it’s still too early to formally provide 2023 guidance, we believe this level of well connection activity and continued contracted EBITDA growth behind our Double E joint venture to generate at least 10% year-over-year Adjusted EBITDA growth in 2023.

In addition, to support that initial FY 2023 Adj. EBITDA discussion, management is suggesting at least 200 wells could be connected behind its systems in 2023. This would be about an 80% increase to both FY 2021 and FY 2022.

Based on recent customer development plans, permitting and rig activity, and commodity price expectations of over $80 per barrel of crude oil and over $5 per MMBtu of natural gas in 2023, we currently expect to connect at least 200 wells to our systems in 2023. While this remains below pre-pandemic average well connections of approximately 260 wells per year, this would be a 80% increase from the average wells connected to the system in 2021 and 2022.

Now that we have housekeeping matters out of the way, in today’s piece, I write to share my pro-forma model and explain why SMLP’s FY 2023 Adj. EBITDA growth also looks conservative. I won’t go as far as to say ‘super’ conservative, like I did back on March 8, 2022. Again, though, I do think there is upside to 10% Adj. EBITDA growth in FY 2023.

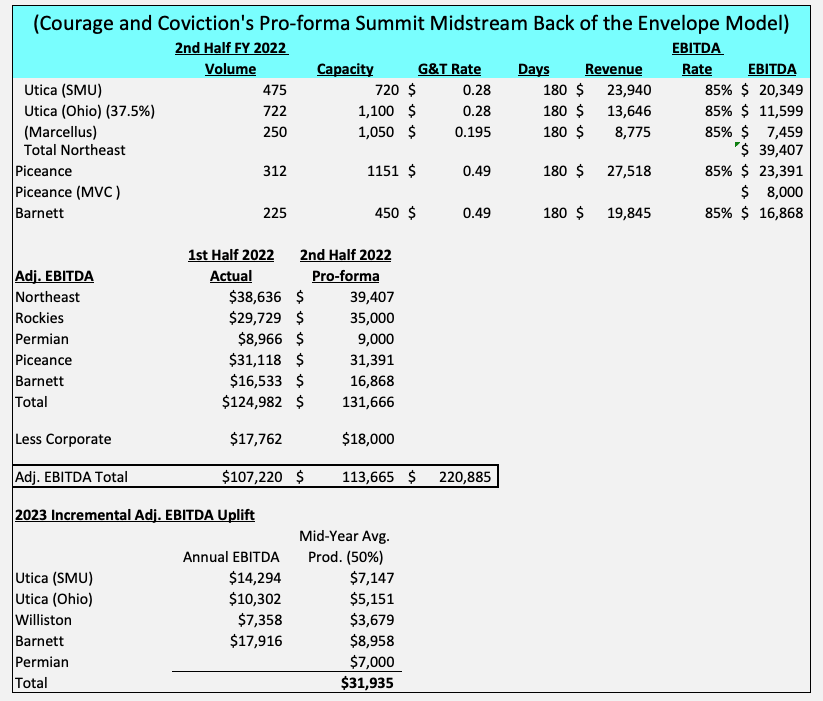

My Pro-forma SMLP Back of the Envelope Model

Based on the updated information we have from August 4, 2022, as well as Summit’s August 5th conference call, I created this following pro-forma model.

Generally speaking, I am fairly good at synthesizing and I usually don’t spend a ton of time building out models. However, I made an exception here and built a simple model on Summit to show its FY 2023 initial Adj. EBITDA commentary is very achievable.

I am making volume x G&T (gathering and transport) calculations to get to revenue and then making Adj. EBITDA capture rate assumptions. All of my assumptions are based on synthesizing based 10-Ks and 10-Qs combined with management’s public commentary on 2nd half 2022 drilling activity.

Courage and Conviction’s Model

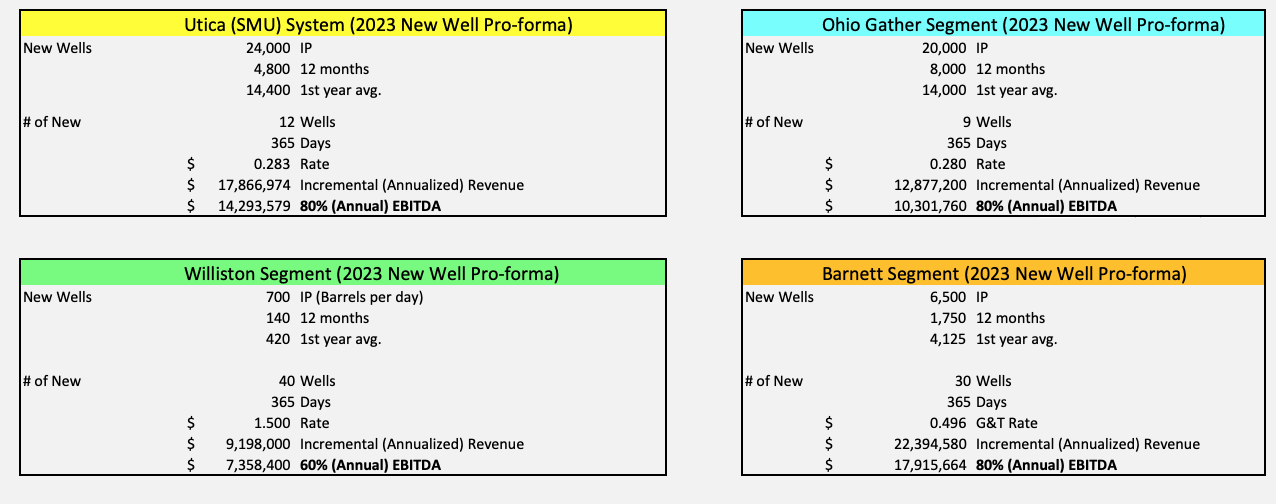

Next, in 2023, I am assuming flat production/EBITDA in the DJ and Marcellus and the Piceance basins as new wells will be incremental and should enough to hold production flat. To drive FY 2023 Adj. EBITDA, the upside resides in four basins. Enclosed below you can see my assumptions on numbers of wells, IP rates, G&T rates, and incremental Adj. EBITDA. Also, given the timing of drilling, I am only assuming 50% of the uplift, as not all of the wells will come online in January 2023. 2023 production will occur throughout the year.

Based on these assumptions, and I don’t think they are aggressive, by any stretch, as you can see, there is a very realistic pathway to $250 million in FY 2023 Adj. EBITDA. Moreover, given Ascent’s purchase of Exxon’s Utica acreage, combined with how good Ascent is as a shale producer, there could be upside in the Utica (SMU) system as there is 720 Mcf/d of capacity (I am only assuming 2022 exit rate production at 475 Mcf/d). Also, there could be upside on its Ohio system too (given the strong IP rates and outlook for natural gas).

Courage and Conviction’s Model

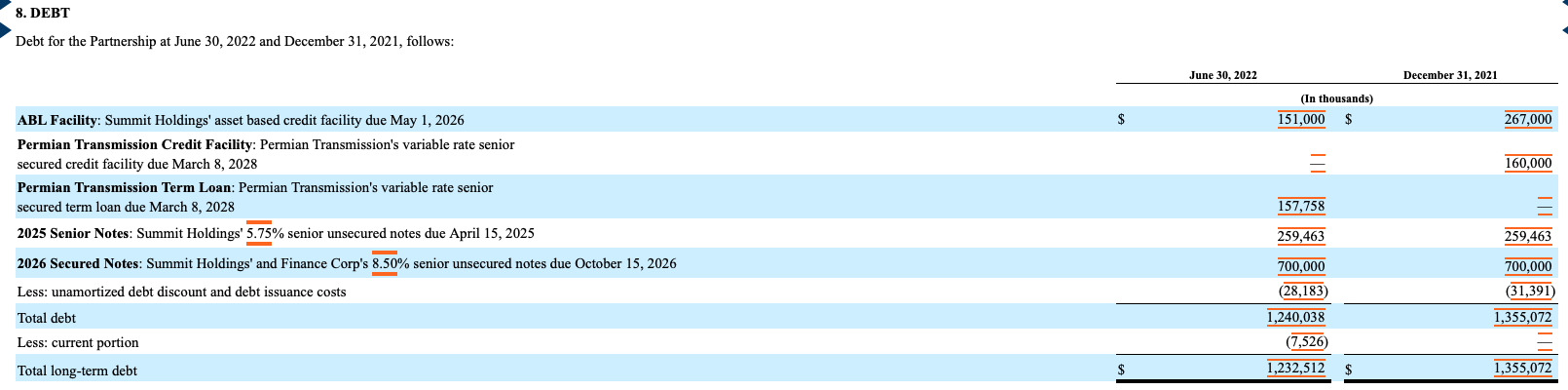

The Balance Sheet

In terms of the debt, as of June 30, 2022, Summit’s debt is as follows:

$151 million ABL, $700 million on the 8.5% Second Lien Notes, and $259 million 5.75% 2026 notes. There is also about $113 million of preferred stock that is in PIK status. As of now, the Double E pipeline is off balance sheet as the cash flow from the asset is earmarked to pay down and service the $158 million Permian Term Loan that is Libor +2.375% and there is about a $105 million Preferred on the Double E.

Summit Midstream’s FY 2022 Q2 10-Q

As an aside, in its current state, the Double E is a 1.3 Bcf/d pipeline that should generate $45 million of annual Adj. EBITDA, once fully subscribed. As of November 2023, there will be 1 Bcf /d of take or pay contracts. In case you don’t know, these are ten-year take or pay contracts and Exxon Mobil is the anchor sponsor, with 750 Mcf/d. Given the number of rigs running in near the Double E and the strong demand pull out of Waha to the Texas coast, driven by strong LNG and Mexican gas imports, I would argue that the Double E should trade at 10X to 12X. Also, with perhaps about $50 million or $60 million of incremental investment, Summit’s management has suggested that pipeline could expand to upwards of 2 Bcf/d, which could result in approximately $60 million of annual Adj. EBITDA. Now again, this is a few years out, as Summit needs to secure the 10 year take or pay commitments on the remaining 0.3 Bcf/d as well as secure commitments on the would be incremental 0.7 Bcf/d before any final expansion plans are made. That said, net of the debt, in its current state, you could argue that equity value of Double E today, is close to $200 million, to Summit, and net of its current debt, at the operating company level.

Pro-forma Balance Sheet Leverage

So, let’s say, during the 2nd half of 2022, Summit generates another $35 million of free cash flow that will be used to pay down debt.

In 2023, based on my model, I’m projecting $250 million of Adj. EBITDA, assuming $40 million of Capex (given the big well growth). So, net of Capex and assuming $90 million of cash interest, we are looking at $120 million of free cash flow, however, $25 million of Adj. EBITDA is trapped at Double E, so we are still looking at $95 million of free cash flow, net Summit, the parent.

So assuming $130 million of free cash flow (2nd half 2022 and FY 2023), net debt, at the parent level should be about $20 million on ABL, and $960 million on the notes, or $980 million, as of December 31, 2023.

$980 million/$250 million of FY 2023 Adj. EBITDA is less than 4X of leverage. That is a dramatically better than over five turns of leverage not that long ago. This should re-rate the equity as it opens the door to a better refinancing of its $700 million 8.5% 2L debt.

Other things to consider

On June 30, 2022, Summit sold its small Lane Gather system to Matador Resources (MTDR), for $75 million of cash proceeds. As management stated, this transaction reduced Summit’s net leverage by 0.3X. Also, this saves Summit about $2.5 million per year in underutilized firm transport and Matador has committed capacity on the Double E pipeline.

Given that Summit’s team has now shown they are creative and willing to divest a non-core asset to de-leverage the balance, I want to speculate on other possible assets that might make sense to sell.

Here is management’s commentary from its August 5, 2022 call.

As we have discussed, growth in the base business is only one aspect of our overall story, we are pursuing and continuing to pursue leverage and value accretive bolt-on acquisitions and divestitures, and we’re also making great progress on commercializing and potentially expanding the Double E pipeline in the Permian.

I would argue, and again, this is me speculating, that Summit could sell its Marcellus system to Antero Midstream (AM), at the right price. This is 1.05 Bcf/d capacity pipeline that is very underutilized, at only 360 Mcf/d, in 2021. Based on triangulating Summit’s prior 10-Ks and 10-Qs, it looks like the G&T is only about $0.194. That said, it is super underutilized as Antero Resources (AR) controls the drill bit. The Marcellus system has generated low $20 million Adj. EBITDA on very depressed volumes. Perhaps, Summit could fetch $175 million for this asset, in a sale (which would only be 7X, using $25 million of Adj. EBITDA. I would argue that this would be win-win, as Summit could strongly reduce its net leverage and Antero Midstream would acquire an asset at a big discount (relative to the cost to build and given the depress volumes). Moreover, Antero Resources might be more inclined to drill behind this system’s inventory if Antero Midstream owned the asset, as it should be accretive to both Antero Midstream and Antero Resources. Secondly, I would argue that Summit’s DJ Basin assets are small and non-core. If they could get a good cash price, it might make sense to sell that to a large player that is bullish on oil drilling picking up in that basin. Again, any deals would have to be accretive to Summit’s balance sheet by reducing turns of leverage.

Putting It All Together

On August 4th, Summit reported a solid Q2 FY 2022 report, revised its FY 2022 guidance to the high end of its range and provided initial commentary for at least 10% Adj. EBITDA growth in FY 2023 based on upwards of 200 well connections behind its system, in 2023.

As I’m super in the weeds here, I decided to share my back of the envelope model. The reason for doing so is because there is such limited sell side coverage here. Moreover, I was really surprised that RBC was modeling FY 2022 and FY 2023 Adj. EBITDA at only $205 million.

In closing, SMLP units are way too cheap and fair value should be closer to $25, with upside potential in the low to mid $30s. Frankly, I have no idea why they are available for purchase at only $16.36, as of last night’s closing price. Lastly, I think my 2023 modeling assumptions are very fair and reasonable based on management’s commentary.