Sundry Photography

Investment Thesis

SiTime Corporation (NASDAQ:SITM) is a profitable business in the semiconductor industry with growing revenues and cash flow for the company to work with to further increase its profitability and expand into different end-markets.

SITM is positioned for long-term growth because of the following:

-

Its revenue is increasing, that’s always good.

-

Its growth opportunities in the Comms & Enterprise, Automotive, and Mobile end market position them for long-term performance.

-

They’re building more wafer inventory to battle supply chain constraints, their current edge over its peers.

Overall, SITM has a lot of potentials, mainly from growth drivers like 5G network driving densification in Comms & Enterprise, Advanced Driver Assistance Systems or (“ADAS”) in the Automotive, and smaller size with increased functionality in the Mobile end market. However, I rate it as a Hold because it is too overpriced compared to its peers in the industry.

Why SITM Might Be Staying For Long

SITM has a lot of opportunities in its end markets. Its revenue has been growing about 60% for the past few quarters with a gross margin of 50%. Its end markets, the Communications & Enterprise, Automotive, Industrial, and Aerospace, and Mobile, IoT, and Consumer, are set up for long-term performance. I’ll explain why each end market is set up for long-term performance, its demands, growth drivers, and its market size:

Communications & Enterprise

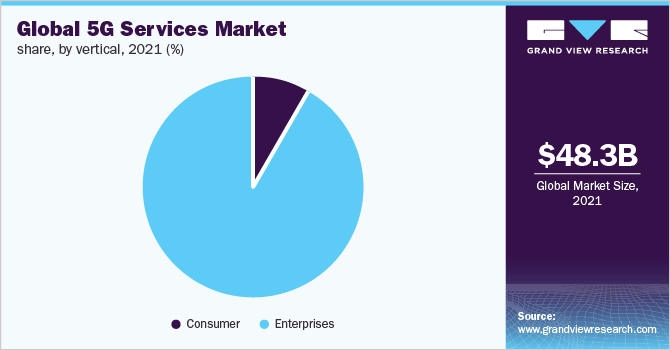

GrandViewResearch – 5G Services Market Size

In SITM’s Communications & Enterprise end market, they specialize in making 5G network densification. They’re going to make smaller and denser cells. SITM has excellent opportunities to enter the 5G market as well. The 5G market had a $48.25 billion addressable market and is expected to grow by $90 billion in 2022 with a Compound Annual Growth Rate of 56.7% from 2022 to 2030. This is an excellent opportunity for SITM to improve its precision timing solutions since SiTime Precision Timing provides:

-

Precision under changing temperatures

-

Stability under vibration

-

High reliability

SITM – Investor Presentation

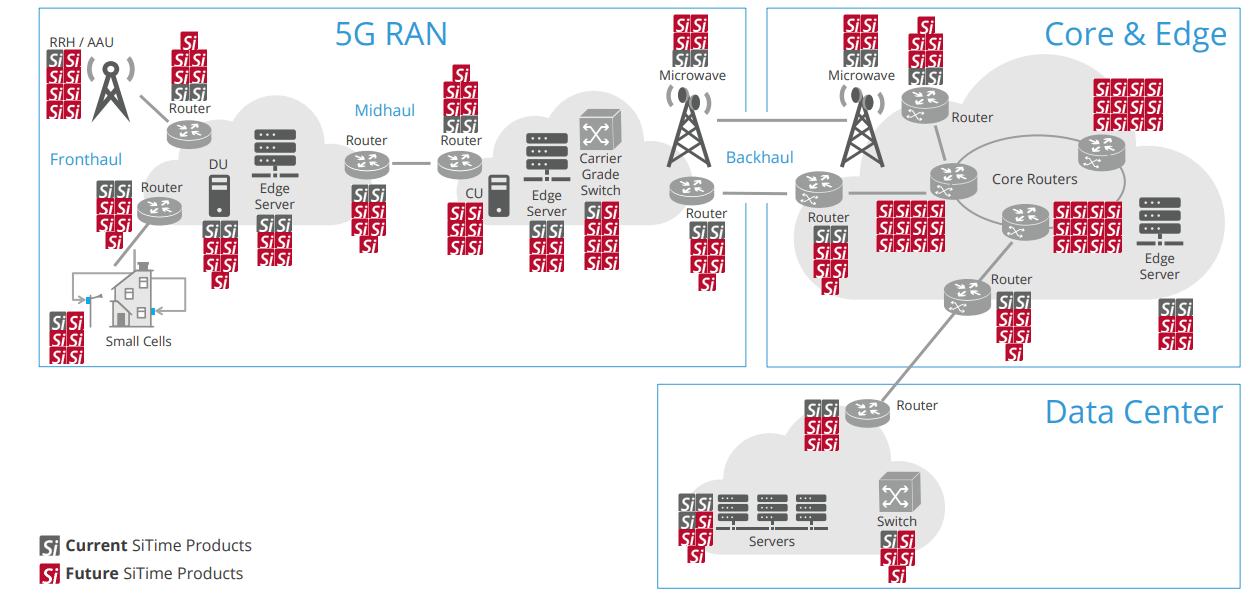

Overall, I think that 5G will be around for a while, and SITM has a lot of opportunities for their precision timing solutions. They can provide solutions for data centers, routers, and:

-

Servers

-

Timing Servers

-

Leaf Switches

-

WAN Routers

-

Spine Switches

-

Switches

-

Storage

These are some of the products that SITM can offer to its customers. There will be a need for 5G products sooner or later. SITM’s precision timing solutions can make this an opportunity for growth in the company.

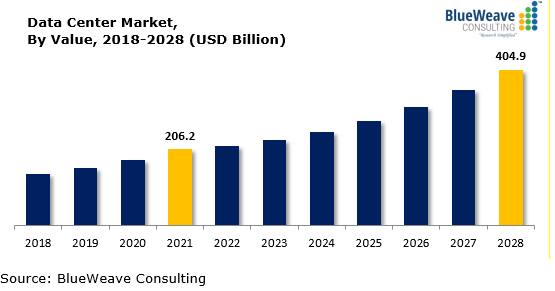

BlueWeave Consulting – Data Center Market

The demands in the respective end markets will continue to grow because of the increasing adoption of advanced technologies. The data center market alone had an addressable market of $206.2 billion in 2021. As I’ve said, there are a lot of opportunities for SITM in the Comms and Enterprise with their precision timing solutions. They’re set up for long-term growth in this end market.

Automotive, Industrial, and Aerospace

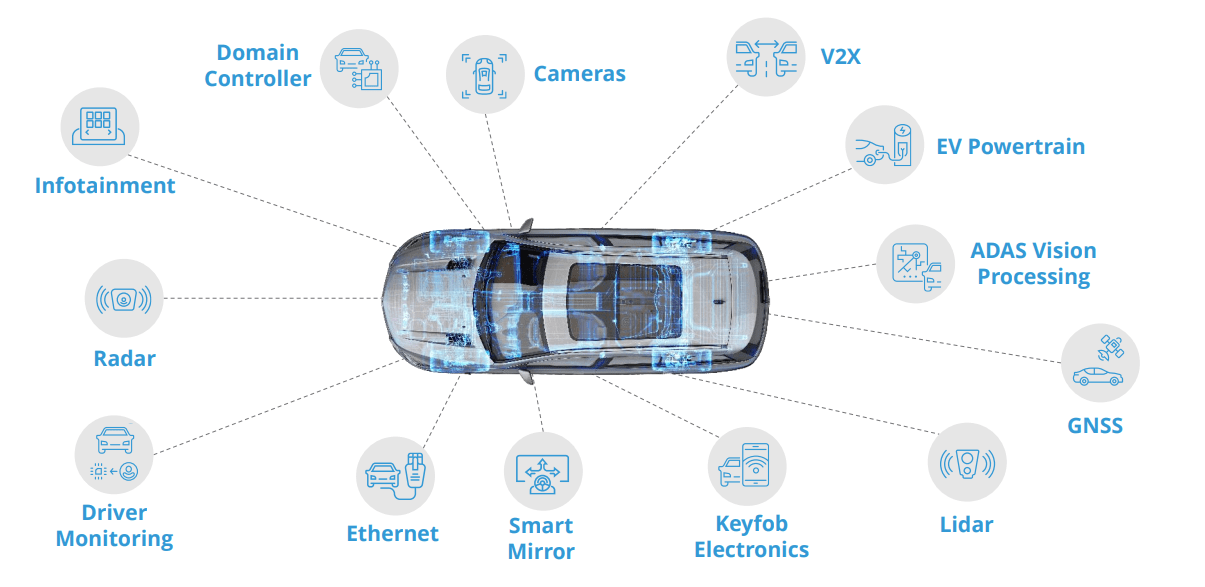

SITM also provides solutions for the Automotive, Industrial, and Aerospace end markets. They offer a wide variety of products that can be used to improve the sensing and connectivity of industrial machines, medical electronics, Advanced Driver-Assistance Systems (“ADAS”), Automotive cameras, drones, and solar inverters.

SITM – Investor Presentation

The global IoT automotive market was worth $58.7 billion in 2021. It will continue to grow as the automotive industry adds more IoT tech to their vehicles, especially sensors, Wi-Fi connectivity, and entertainment. SITM is one of the few companies that produce a wide variety of electronic automotive products. From radars, ADAS, domain controllers, cameras, smart mirrors, ethernet, infotainment, lidar, and more, SITM can produce these products.

Mobile, IoT, and Consumer

SITM also produces precision timing solutions for mobile and wearable devices. Like most companies, they’re focusing on miniaturization or making processors smaller, which means lower latency (the denser the processor, the shorter the signal paths, which means faster computing), making them cheaper to produce.

SITM – Investor Presentation

Although there are already a lot of companies out there that also produce these products, it’s still worth mentioning that SITM has the whole package across different end markets. With SiTime’s Precision Timing, they can make processors and System On Chips (“SoCs”):

-

Smaller

-

They can produce wearable devices with longer battery life

-

Fabless semi-process & supply chain

The Mobile market isn’t currently considered SITM’s strong suit. According to Rajesh Vashist, SITM’s CEO:

Excluding our largest customer, the mobile IoT consumer segment is expected to be down by more than 30% in the second half of 2022.

– SITM Q2’22 Earnings Call

SITM’s products are available to customers that need precision timing solutions for smartphones, styluses & tablets, headphones, smart watches, Virtual Reality (“VR”), and personal health trackers. While it’s true that SITM’s business model is setting the company for better long-term performance, they’re performing well on the short-term side of things too:

Threat Of New Entry? SITM’s Current Advantage

Although there are a lot of semiconductor companies out there, SITM’s current advantage is supply. They have increased their inventories by $4 million from Q1’22. I’m not saying that they’re immune from any wafer/semiconductor supply chain disruptions. Instead, I think it’s good that management took preventive measures to ensure they can cater to their customers’ demands even if there’s another global chip shortage.

Author – Inventory Growth from SITM Balance Sheet

With their growing inventory, SITM’s big customers can feel safe about supply issues, creating a win-win situation for SITM and its customers if there comes a time when there are intermittent supply disruptions with wafers. Art Chadwick, SITM’s Chief Financial Officer, has this to say about their increase in inventory:

But we’ve made a conscious and strategic decision to build some buffer stock, especially with wafers. In case there are any disruptions in the supply chain, a lot of things can happen in the world that could impact the supply of wafers. We want to make sure we’ve got sufficient supply to handle any intermittent disruption.

–SITM Q2’22 Earnings Call

The semiconductor industry has been affected by the global chip shortages in the early years of COVID-19. There is still a possibility of another global chip shortage, but it’s unlikely to happen. However, if it does happen, SITM’s substantial growth in inventories will mitigate supply disruptions. Personally, I think that it was a good business move for SITM to increase its inventories. Even though the possibility of a supply chain disruption is unlikely, it’s good that they are taking precautionary measures just in case it happens.

Financial Analysis

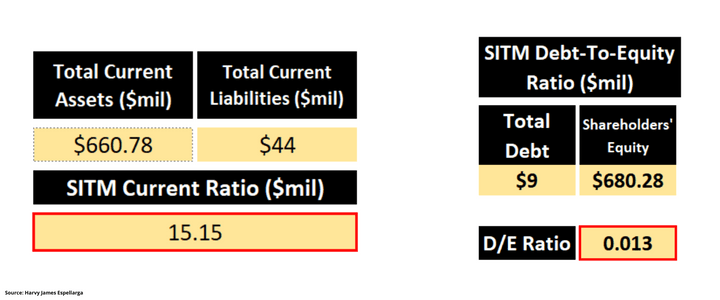

Author – Current & Debt To Equity Ratio from SITM’s Balance Sheet

SITM has $580.26 million in trailing twelve-month cash & cash equivalents, growing almost 600% compared to 2020’s cash & cash equivalents of $73.53 million. The company also has total current assets of $661 million and total current liabilities of $44 million.

This is great because the company won’t have liquidity problems and can quickly pay off its debts, bringing us a 15.15 current ratio. SITM also has $9 million in total debt and $680 million in equity, which gives us a 0.013 debt to equity ratio, which is good because they’re getting their funding not from lenders but equity.

SITM features a strong balance sheet, with high numbers of cash flowing in and relatively low debt levels. The company has no liquidity problems in the foreseeable future. However, you’ll understand why I rate the stock as a Hold in the next section.

Valuation

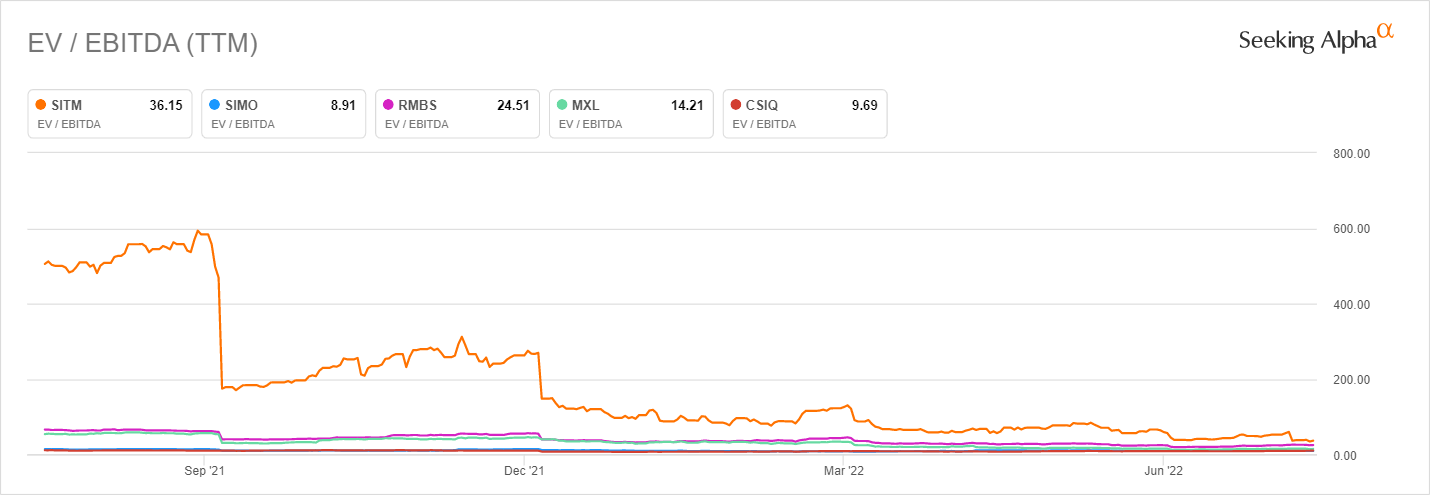

Seeking Alpha – EV/EBITDA

When compared to peers like Silicon Motion Technology Corporation (SIMO), Rambus Inc. (RMBS), MaxLinear, Inc. (MXL), and Canadian Solar Inc. (CSIQ), there was a time that SITM did trade at a higher price compared to its peers making SITM much more expensive. However, the EV/EBITDA ratio is stabilizing. SITM is trading almost closely with its peers at around a 9 EV/EBITDA ratio.

Compared to its peers, SITM is potentially overvalued. It has an EV/EBITDA multiple of 30-60 on average, which is a higher EV/EBITDA that could signify that it’s overvalued. If the company traded around the EV/EBITDA multiple of 15-20 (the average multiple their peers are trading at), then SITM would be reasonably priced.

If SITM traded around a 15-20 EV/EBITDA multiple, then I might change my rating as a Buy, but until that happens, my rating stays the same, a Hold. The company’s EV/EBITDA is correcting itself and might even trade at a lower price. Still, without any significant changes to their core operations and any announcements from management, I rate the stock as a Hold for now.

Risks

Consumer Power

SITM currently relies on its customers and its consumer power. A change in demand for SITM’s computing solutions could potentially harm the business and affect its core operations. A change in demand will affect revenue, affecting the company’s profitability.

Supplier Power

Although I acknowledge that SITM has been building up its inventory for the past few quarters, SITM still depends on wafer suppliers. SITM added $4 million in inventory as “buffer stock” to its Q2’22 results, which is a great business move since they can supply customer demands even if there’s a supply chain disruption for these wafers. However, it is worth noting that this is still a risk SITM can face, especially if the time comes when they could run out of supply in these wafers.

Taiwan and China Situation

Taiwan and China are the largest producers of semiconductors in the world. Even if SITM has sufficient inventory to meet customer demands, tensions between Taiwan and China will disrupt the semiconductor economy if the situation rises. China accounts for 24% of the world’s semiconductor production, followed by Taiwan at 21%. If things go south with both countries, it will affect the semiconductor ecosystem and can even start another worldwide global chip shortage.

Investor Takeaway

I think SiTime Corporation is a good business with a business model set for long-term performance. They have increased revenue and cash flow and have low debt levels. They also have different opportunities in their various end markets. SITM has a chance to hop on the 5G technology, Advanced Driver-Assistance Systems (“ADAS”), and smaller and more compact SoCs for mobile devices trend. SITM is currently much more expensive and potentially overvalued than its peers. I rate the stock as a Hold for now and will gladly follow the business on its future announcements.

Thank you so much for reading. I welcome all comments, ideas, and reactions to my articles. I appreciate you and have a great day.