FooTToo

The current geopolitical environment has pushed on the demand for locally available and sustainable energy sources. Clean Energy Fuels Corp. (NASDAQ:CLNE) is a significant provider of renewable natural gas (RNG) for the transport industry. Earlier this month, the US passed an ambitious climate bill to reduce carbon emissions across many industries, including transportation. The news was well received by sustainable energy companies on the stock market, as seen with CLNE below.

Stock Price One Month Trend (SeekingAlpha.com)

To date, CLNE has had a very unsuccessful financial performance. It has been unprofitable for over 15 years, and there has been little to no sales growth since 2017. A glance at opinions across the internet seems that this is a mismanaged company run by greedy executives.

Nonetheless, 2022 has changed the energy market, and using RNG as an alternative fuel source is becoming a reality. Just this week, CLNE has revealed several significantly large-sized supply deals. Although we are looking at a financially unattractive company, I believe that the upside potential, in the long run, is inevitable for this cheap stock as more and more transport companies are replacing diesel trucks with either electric or RNG alternatives to cut costs and stay in compliance with legislation. CLNE also has some projects going live at the end of this year to increase supply to help meet growing demand. Therefore, I believe investors may want to take a bullish stance on this company.

Growing Market Demand For RNG

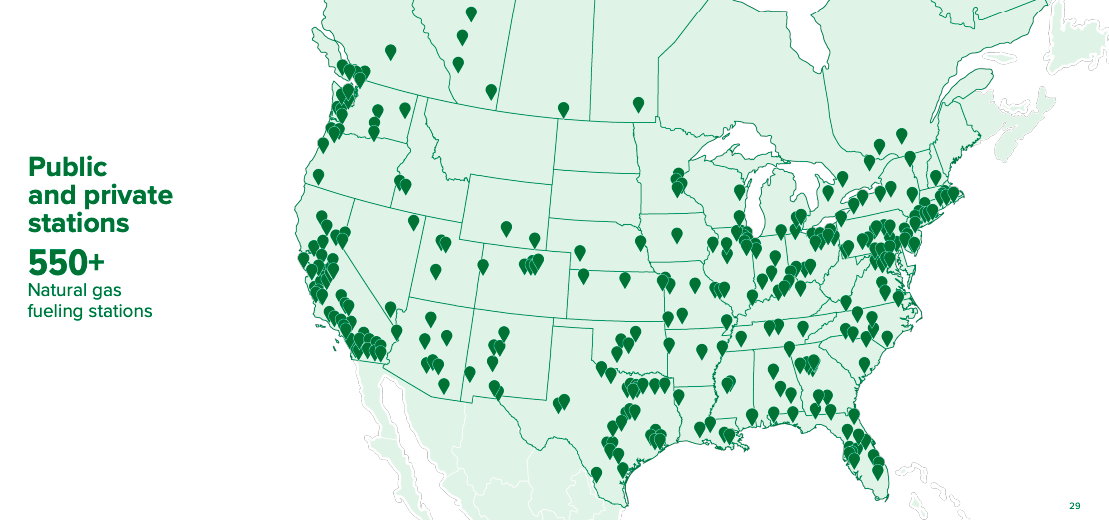

CLNE, founded in 2001, is a major supplier and distributor of different types of natural gases. Since 2014 it has focused on RNG with the goal of decarbonising transportation. The supply facilities are across eleven states. Over its operational history, it has grown its distribution to over 550 fuel stations that it owns or operates in the United States.

Distribution map (Investor Presentation 2022)

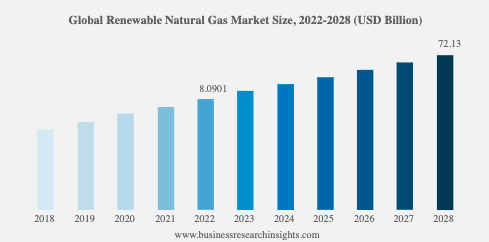

The company’s performance is highly dependent on adopting natural gas vehicles and the price of alternative fuel sources. It focuses on the trucking, transit, refuse, fleet services and airport sectors. 2022’s geopolitical events have catalysed fleet operators to search and switch to alternative energy solutions actively. The demand for RNG is growing as logistics companies consider ease of fuelling, carbon reduction, costs, reliability and compliance with legislative rules. The global RNG market could reach $72.15 billion within six years.

Global RNG Forecast (BusinessResearchInsights.com)

CLNE has announced some exciting supply agreements, and for many of these companies, it is the first time they have considered RNG. Firstly, with California Transportation Dynamics (CTD) is replacing 40 diesel trucks and has agreed to 1.2 million gallons of RNG over the duration of the contract. Secondly, National Ready Mix Concrete has agreed to 130,000 gallons of RNG for 13 trucks. Fourthly the City of Claremont has agreed to 400,000 over a multiyear contract for 20 trucks. Fifthly a 260,000-gallon agreement with NGL Logistics for six trucks. Lastly, Gen Logistics has decided to 30,000 gallons.

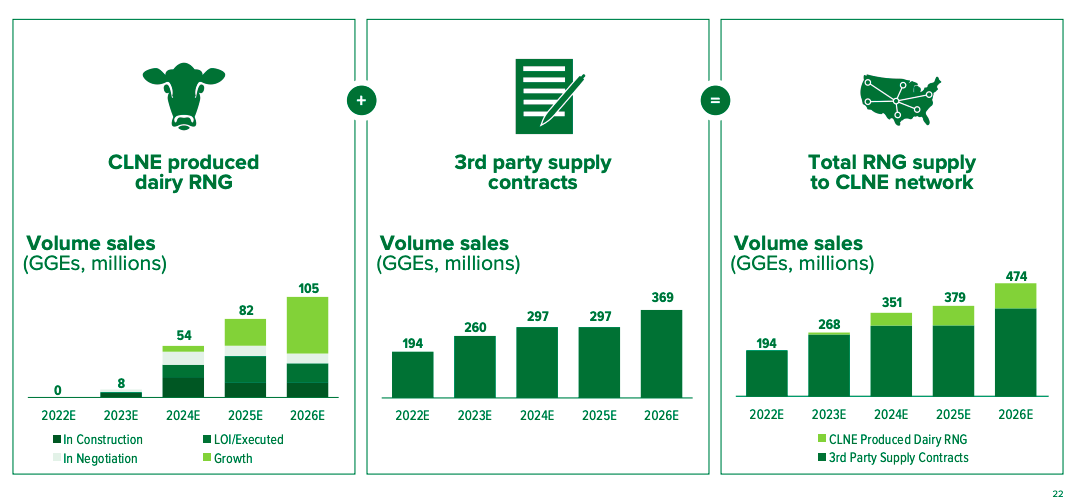

Clean Energy converts methane produced from dairy farm waste to RNG. It has a joint venture with TotalEnergies (TTE) and BP (BP), providing the required capital to operate projects alongside dairy owners across the USA. The company is also benefiting from heavy-duty trucking interest in the new environmentally beneficial 15-litre natural gas engine by Cummins, which is already operational in China and will be live in the States by 2024. The company has had a supply contract with Amazon (AMZN) since last year, which includes the construction of nineteen new fuel stations. Furthermore, it has projects in place to increase the supply over the following years to meet the exceedingly higher demand for natural gas as a fuel source.

Supply Growth Potential (Investor Presentation 2022)

Financials and Valuation

If we look at the company’s annual financial performance, there are red flags as the performance stagnates or declines in earnings and revenue, as seen below between 2019 and 2021. However, 2022’s financials for this company indicate a slow but upward trend per quarter.

Annual and Quarterly Revenue and Earnings (YahooFinance.com)

In Q2 2022, it reported a net loss of $13.2 million, EBITDA was $10 million, cash flow from operations and CAPEX improved significantly year on year by 182% for cashflow to $27.4 million in CapEx by 117% to $10 million. RNG volumes increased by 17% to 50 million gallons. The margin per gallon was $0.28 a gallon for this quarter, an increase of $0.03 from Q1 2022. The margin has increased because of a combination of higher retail prices and higher fuelling costs. The company had $187 million of cash and investments. Although there is a growing demand for RNG fuel, the financials for this company are not in line with the monetary growth you would expect. Nonetheless, it has the infrastructure in place on the distribution side, and it is growing its supply availability which should reap the rewards in the long term.

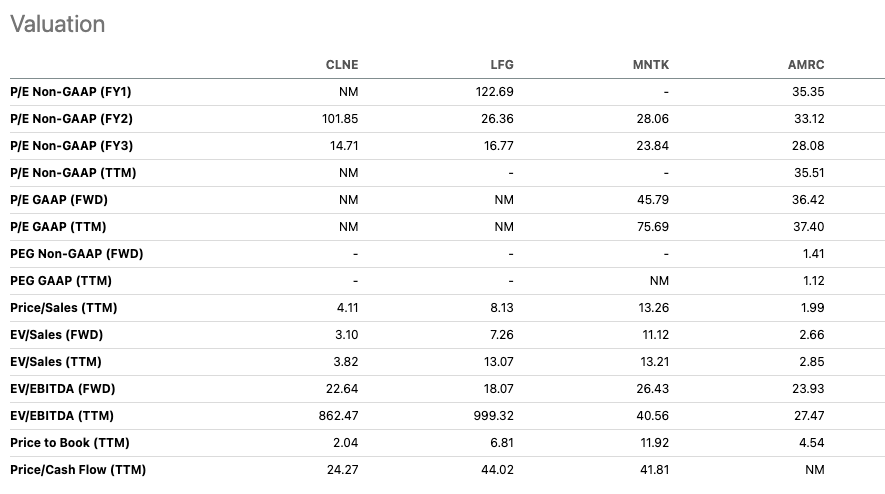

CLNE has a market cap of $1.47 billion and is affordable compared to critical players in the renewable natural gas sector. I have made a relative comparison below, and if we consider the forecasted price-to-earnings ratio for fiscal year three. Although the company is currently loss-making, it is undervalued if we compare its future predicted performance to its peers. If we look at the price-to-book ratio, we see that it is trading higher than the value of its assets, but it seems more attractive at 2.04 compared to its direct peers. The company has a one-year target estimate of $13.06, more than double its current price.

Relative Valuation (SeekingAlpha.com)

Final Thoughts

Although Clean Energy Fuels Corp has a very unimpressive financial performance history, today’s geopolitical environment makes it almost inevitable that this company will succeed in the future with its business proposition aimed at large vehicles in the all-important transport industry. Momentum has picked up this year with the onboarding of new customers, the Amazon contract in place and a growing number of supply and distribution locations to go live in the next few years. A key player in an essential industry at a very affordable price is a rare find. For this reason, I believe investors may want to take a bullish stance on this company.