Justin Sullivan

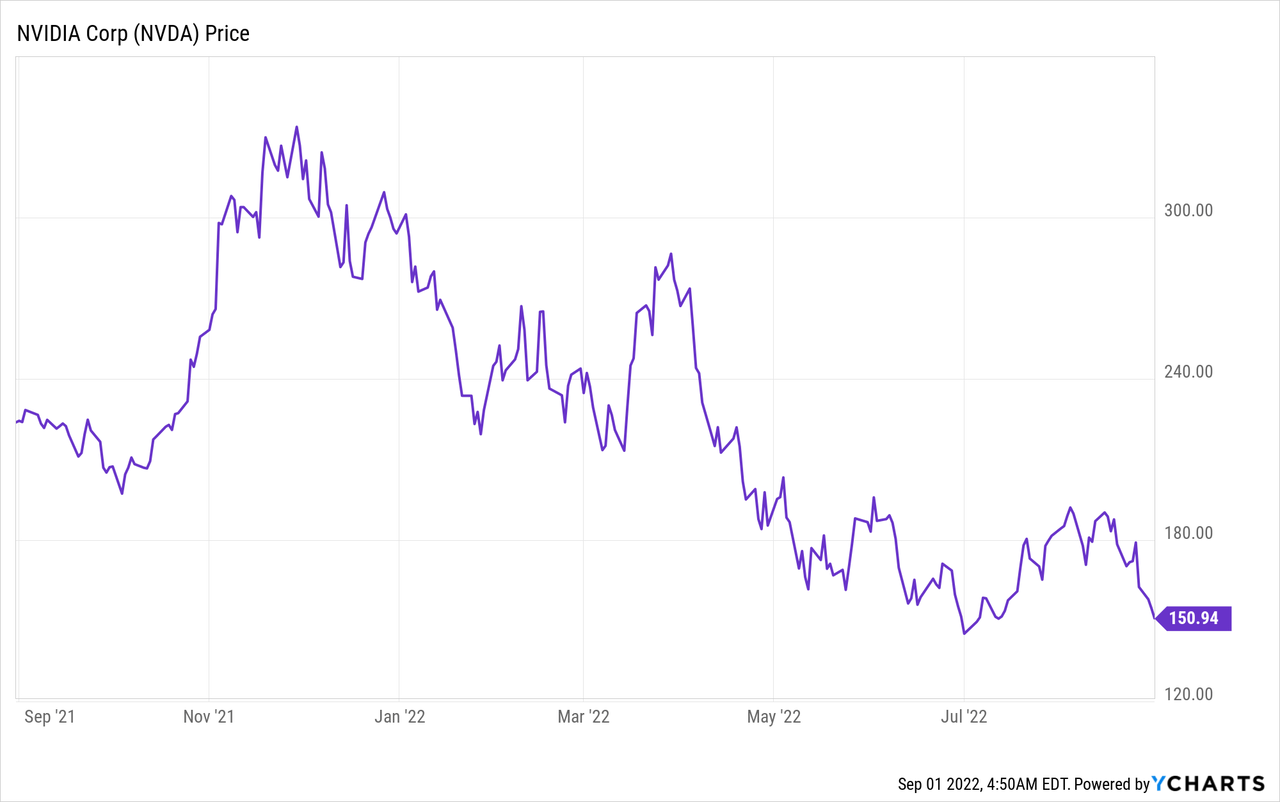

Nvidia (NASDAQ:NVDA) is a technology powerhouse that provides specialist building blocks for the gaming, data center, and even the AI industry. The company’s share price has been butchered and is now down 54% from its all-time highs, which were in November 2021. Its most recent decline was driven by poor earnings results for the second quarter, but it still beat analyst expectations as they weren’t as bad as expected. Nvidia is facing short-term headwinds, but in my opinion, these do not impact the long-term secular growth trends. In this post, I’m going to filter the signal from the noise and breakdown of Nvidia’s Q2 earnings report and its valuation, let’s dive in.

Filter the Signal from the Noise

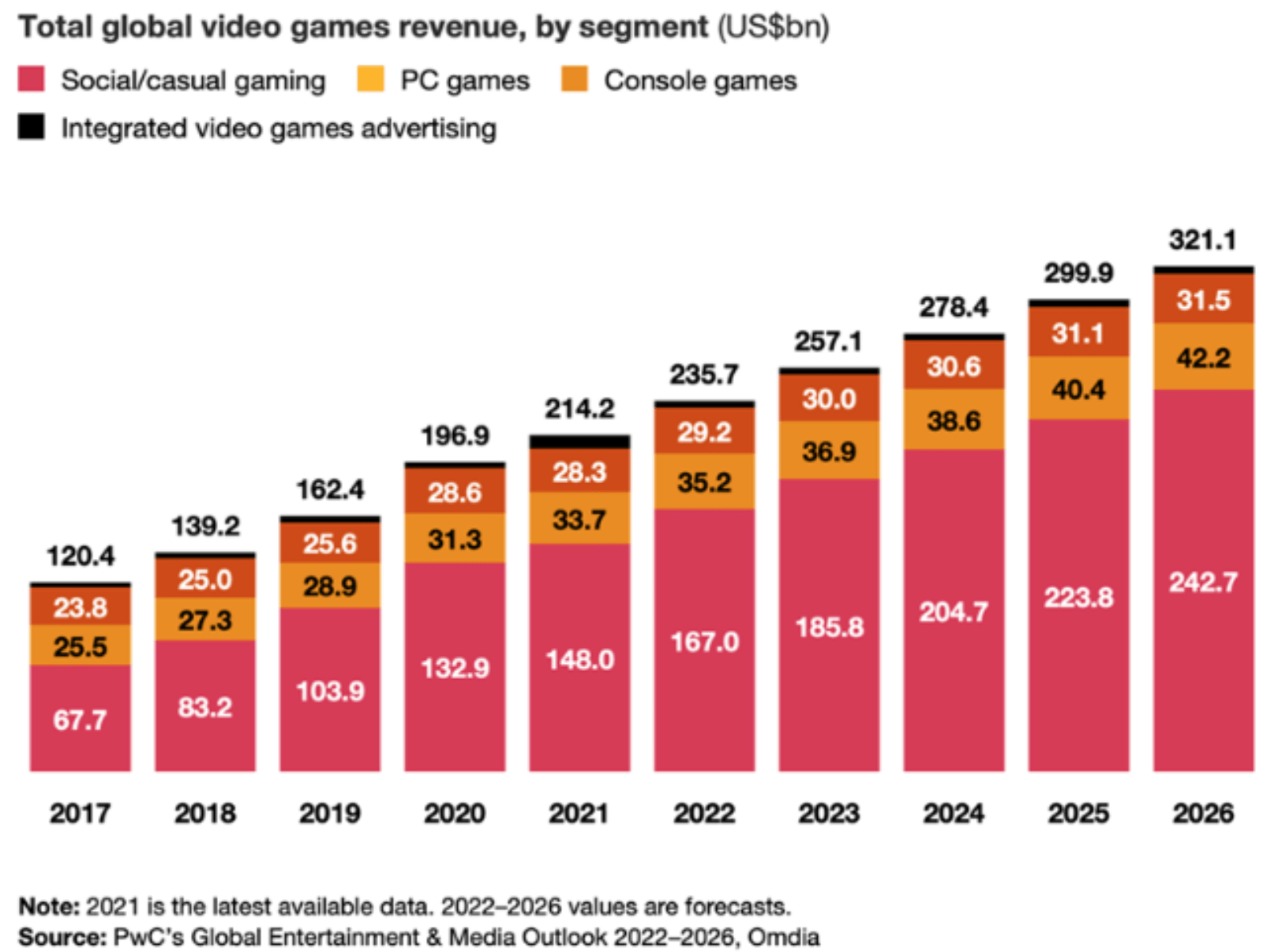

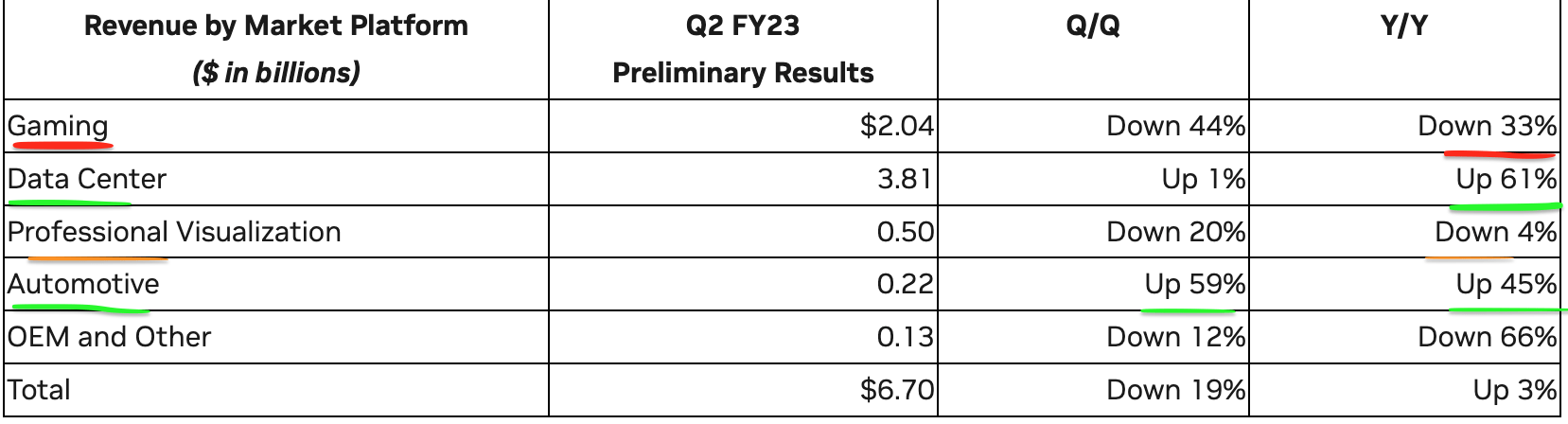

Nvidia reported mixed financial results for the second quarter FY23. Revenue was $6.7 billion which was up just 3% year-over-year and down 19% Q/Q. This may seem terrible at first glance, but when we dive under the hood, it’s clear the reasons why. Gaming revenue was $2.04 billion, which declined by an eye-watering 33% year-over-year. Again, this was driven by a combination of factors such as the tepid consumer demand for gaming which also showed up in Microsoft’s (MSFT) earnings for the Xbox. Taking a step back, it’s clear the gaming market is cyclical and had an unexpected boom over the lockdown of 2020, where the gaming market increased by 23% in value, which was the fastest rate in over a decade. So now we are just seeing a correction in demand to “normal levels”, but the long-term secular trend is still clear. According to a study by PwC, the gaming market is forecasted to grow at a rapid 9% Compounded Annual Growth Rate [CAGR] between 2021 and 2026, reaching ~$321 billion by the end of the period.

Gaming Industry Growth (PwC)

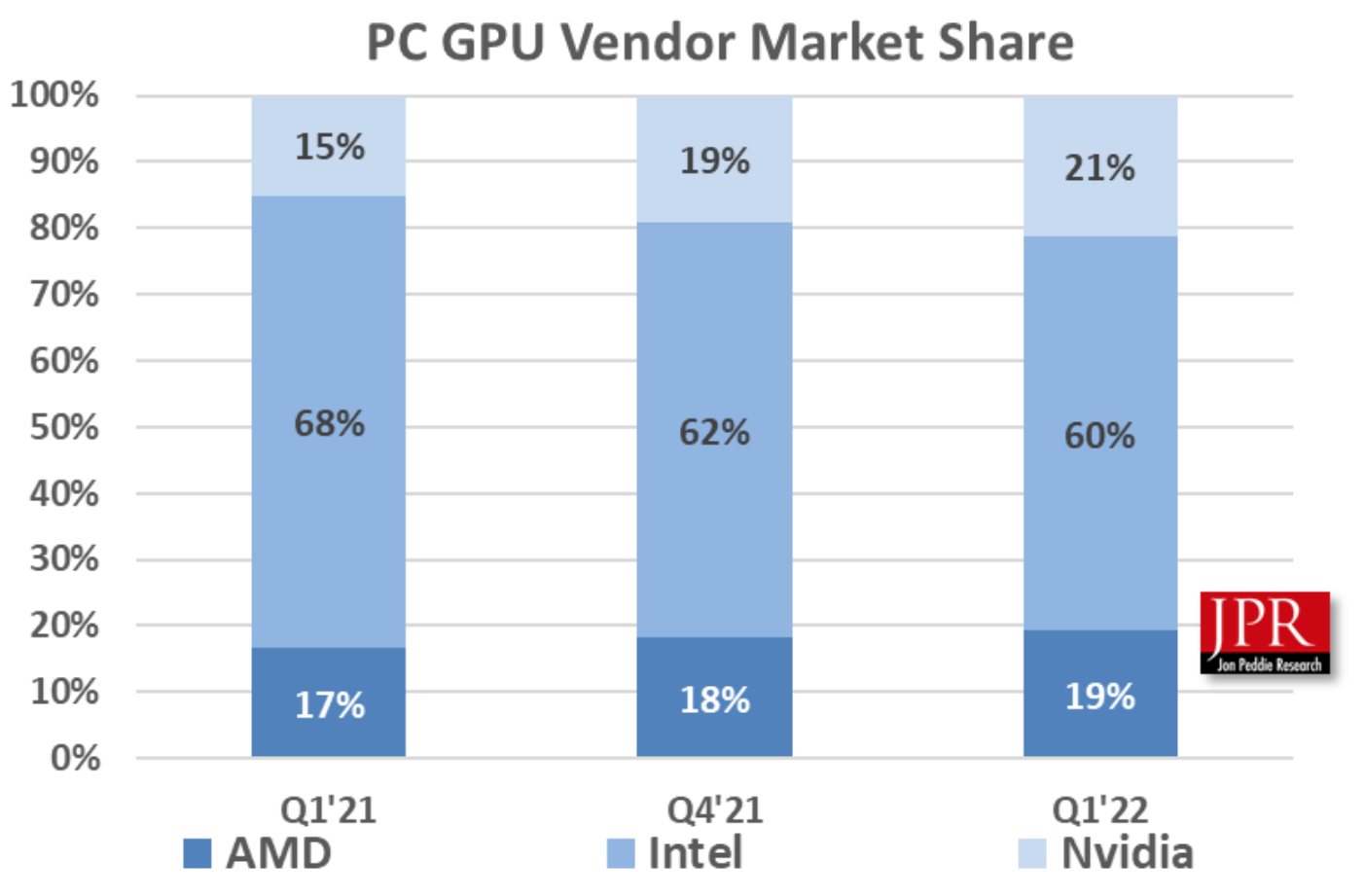

Due to the secular growth trends, I expect Nvidia’s gaming revenue to start to grow again longer term. Intel (INTC) has the largest market share in the Graphical Processing Unit (GPU) industry with ~60% market share. But Nvidia and AMD are leading in “high performance” GPUs which are necessary for gaming. Diving into the chart below, it’s clear to see Nvidia [light blue] had just 15% of the overall GPU market in Q1,21 but by Q1,22, the company had a substantial 21% of the market, while Intel’s market share got squeezed.

GPU Market share (John Peddie Research)

The second major factor which caused a large decline in Nvidia’s gaming revenue was the “Crypto correction”. It has been wildly known that a portion of Nvidia’s GPUs are bought and used for Bitcoin mining. But with the price of Bitcoin plummeting, it is just not economical to mine bitcoin for most people. But this cyclical trend is not something new for Nvidia, and we saw the same boom in “Gaming” revenue during the first crypto bull market of 2017. A slight difference this time is many miners are now using ASICs or (application-specific integrated circuits). In addition, Ethereum is switching to a proof-of-stake model, as with the Proof-of-Work model, the cryptocurrency uses as much power as the Netherlands [yes, the country!] to validate its blocks.

NVIDIA Q2 (Q2 Earnings Report)

Therefore, if we combine, a boom in gaming and a boom in crypto at the top of the cycle, we are now just seeing the cycle reverse. I expect the gaming market to rebound and continue to grow strong following the secular trend. I believe the crypto revenue may not bounce back as high due to the aforementioned reasons. But there are other positive secular trends such as the growth in video editing, driven by the popularity of YouTube and video-based social media apps, which also require high-powered GPUs.

Nvidia’s management has used this decline to execute inventory adjustments and “pricing programs” with channel partners. My best guess is these are a series of discounts to help sell old inventory, which will impact the company’s margins, but it would be better than holding expensive inventory. The company has also announced a series of Gaming laptops and Monitors, which really will help expand the company’s total addressable market.

Nvidia Gaming Laptops (Nvidia)

As someone who runs a large YouTube channel [Motivation 2 Invest] where I interview CEOs and Hedge Fund Managers, video editing is a prime purpose I need high powered computing for. My extensive research online brought me to Nvidia GPUs which are usually sold inside high-powered $3000+ laptops such as the Dell XPS. But with Nvidia’s venture into laptops, it now may make more sense to purchase directly from Nvidia, which would effectively enable them to capture more value from its products. After all, the most complex and important parts of any PC are the GPU and CPU, the other components can generally be purchased from many manufacturers cheaply.

Data Center Boom

Nvidia is not just a gaming company, its Data Center segment is rapidly growing with strong industry tailwinds. Nvidia generated $3.81 billion in Data Center revenue for Q2, which was up just 1% Q/Q but increased by a blistering 61% year-over-year. The recent quarter-over-quarter decline was down to “supply chain disruptions,” according to management. But in my opinion, this may also have been driven by a short-term slowdown in IT spending due to the macroeconomic conditions [discussed in the risk section]. However, it’s great to remember the long-term secular trend is up. The Data Center market is forecasted to grow at a blistering 21.98% CAGR between 2021 and 2026. Over this period, an extra $615 billion is expected to be added to the market value. Large companies are “digitally transforming” their IT operations to the cloud. This is for a few reasons which include more “agility” and the ability to lower costs long term, as you only pay for the computing power you need. The boom in data centers is already showing up across the board in other companies’ earnings reports, such as Amazon (AMZN), where AWS is its fastest growing and most profitable segment.

Nvidia’s expertise in Artificial intelligence is also another major advantage, given the AI industry is forecasted to grow by a blistering 38% CAGR between 2022 and 2030.

Metaverse?

Professional Visualization revenue for Q2 was $496 million, which did decline slightly by 4% year-over-year and 20% over the prior quarter. This decline was driven by “macroeconomic headwinds” and slowing enterprise demand. Management expects these trends to persist in the third quarter, which isn’t a great sign. However, there were some positives in the quarter, which included Nvidia’s expanded partnership with Siemens to enable the “industrial Metaverse” and increase the adoption of AI digital twins. This is an amazing technology that enables entire manufacturing plants to be replicated digitally, and thus, new layouts and adjustments can be made virtually before implementing inside the real factory. For example, Amazon Robotics is using Nvidia’s technology to build AI digital twins of its warehouses.

Nvidia Digital Twin of the BMW Factory (NVIDIA)

Nvidia also announced its Omniverse Avatar Cloud Engine, which makes it easier to build “lifelike” virtual assistants and “digital humans” powered by AI.

Nvidia Virtual Human (Nvidia Website)

The Metaverse industry is forecasted to grow at a blistering 39.1% CAGR between 2022 and 2030, reaching a value of $824.53 billion by the end of the period. Nvidia is in prime position to ride this trend as a leader in both gaming, visualization and AI. The company even co-founded the Metaverse Standards Forum, which is basically like the declaration of independence but for the Metaverse. Nvidia even created a “Virtual CEO” for its GTC keynote, which was switched seamlessly with the real person and the majority of people didn’t even notice.

Nvidia Virtual CEO (GTC Keynote)

Automotive Revenue Growth

Nvidia’s automotive segment generated $220 million in the second quarter and popped by 45% year-over-year and a rapid 59% over the prior quarter. This is a small but fast-growing segment with a huge market opportunity across self-driving vehicles. Nvidia’s hardware for self-driving cars called “DRIVE Orin” is expected to be rolled about by partners such as NIO (NIO), Li Auto (LI), JIDU, and many more. Pony.ai even plans to use the hardware for its range of self-driving trucks and robotaxis.

Profitability?

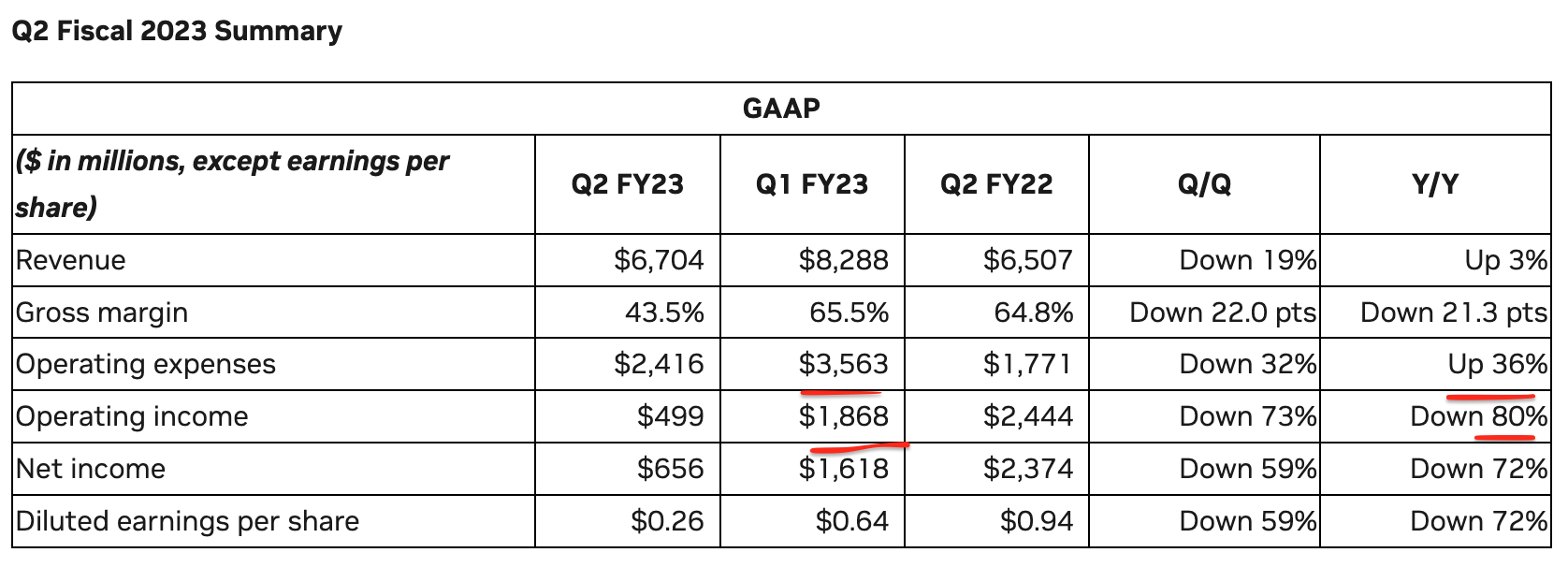

Nvidia has achieved an extremely high gross margin historically of over 65%, however, this has been compressed in the most recent quarter to 43.7%. The good news is management believes its “long-term gross margin profile remains intact”.

Nvidia (Q2 Earnings Report)

Nvidia’s operating expenses popped by a substantial 36% year-over-year, which was driven by a one-off expense of $1.35 billion related to the acquisition of Arm, which didn’t go through. Nvidia also increased the salaries of its employees (which I do not think is a bad thing long term) and also continued to invest heavily into R&D for new products. The good news is operating expenses actually decreased by 32% quarter-over-quarter which is a positive sign.

Despite declining Net income, Earnings per share was $0.26 in the second quarter, FY23, which was $0.06 better than analysts had expected.

Share Buybacks Continue

Nvidia has returned $5.5 billion to shareholders in the form of buybacks and cash dividends in the first half of fiscal 2023. The company plans to “continue stock buybacks” as the CFO foresees “strong cash generation and future growth”.

Nvidia has a solid balance sheet with $17 billion in cash, cash equivalents and short-term investments, in addition, to total debt of $11.7 billion.

Moving Forward

Management expects Gaming and Visualization revenue to continue to decline sequentially next quarter as channel partners “reduce inventory levels” to “align with current demand”. But the company is forecasting solid growth in its Data Center and Automotive segments.

For Q3,23, Revenue is forecasted to be ~$5.9 billion, plus or minus 2%, with a return to strong gross margins of over 62%, which is a positive.

GAAP operating expenses are forecasted to be $2.59 billion, which would represent a further ~8% increase quarter-over-quarter.

Advanced Valuation

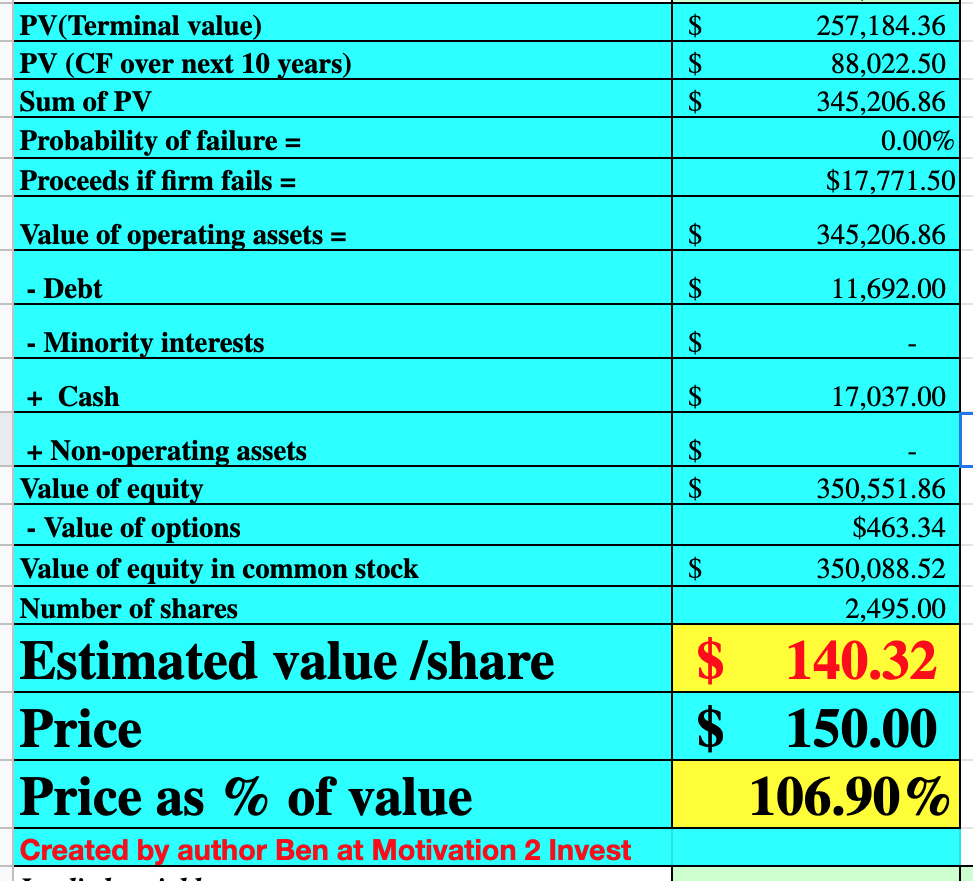

In order to value Nvidia, I have plugged the latest financials into my advanced valuation model, which uses the discounted cash flow method of valuation. I have slashed my revenue growth forecast from previous rates of 30% to 40% to a 10% decline in revenue for next year, followed by 22% revenue growth compounded over the next 2 to 5 years. This valuation is based upon a rebound in cyclical gaming revenue and continued growth in the Data Center and Automotive segments.

Nvidia stock valuation 1 (created by author Ben at Motivation 2 Invest)

I have also forecasted a 45% operating margin over the next 8 years, as the company continues to expand and benefits from greater economies of scale. This also includes an adjustment for the company’s R&D expenses which I have capitalized.

Nvidia stock valuation 2 (created by author Ben at Motivation 2 Invest)

Given these factors, I get a fair value of $140 per share, the stock is trading at $150 at the time of writing and is thus ~7% overvalued.

As an extra data point, Nvidia is trading at a Price to Sales Ratio [FWD] = 14.23, which is ~3% below its five-year average. Therefore, overall, I deem the stock to be “fairly valued” as the bad news for the next quarter has already been priced in.

Risks

Sales stopped in China

Nvidia has recently received a notice from the U.S. government, which has imposed a new license requirement to stop the sale of its A100 and new H100 Integrated circuits in China. This is for national security reasons as it believes the products may have a “military end user” in China and Russia. This makes sense from a security perspective, but it also means a $400 million hit to revenues that were expected to come from China in Q3,23.

Lower IT spend/Recession

A Recession has also been forecasted due to the rising interest rate and high inflation environment, which is expected to further impact consumer sentiment and reduce spending.

Final Thoughts

Nvidia is a leader in high-performance GPUs and is a technology powerhouse. The company’s financials are coming off a strong high last year and the cyclical gaming and crypto industry has taken a major hit. However, the long-term trends are still intact and Nvidia’s innovation is still strong. The majority of the bad news next quarter is already baked into the stock, thus, for long-term investors, the recent panic is mostly noise.