milehightraveler

Introduction

As explained in my previous articles on NuVista (OTCPK:NUVSF) (TSX:NVA:CA), this Canadian natural gas producer is an interesting story to keep an eye on. Unfortunately the AECO natural gas price is pretty weak these days but NuVista has a history of hedging a portion of its output, and this, in combination with still robust condensate and NGL prices, should ensure the company’s cash flows will remain strong.

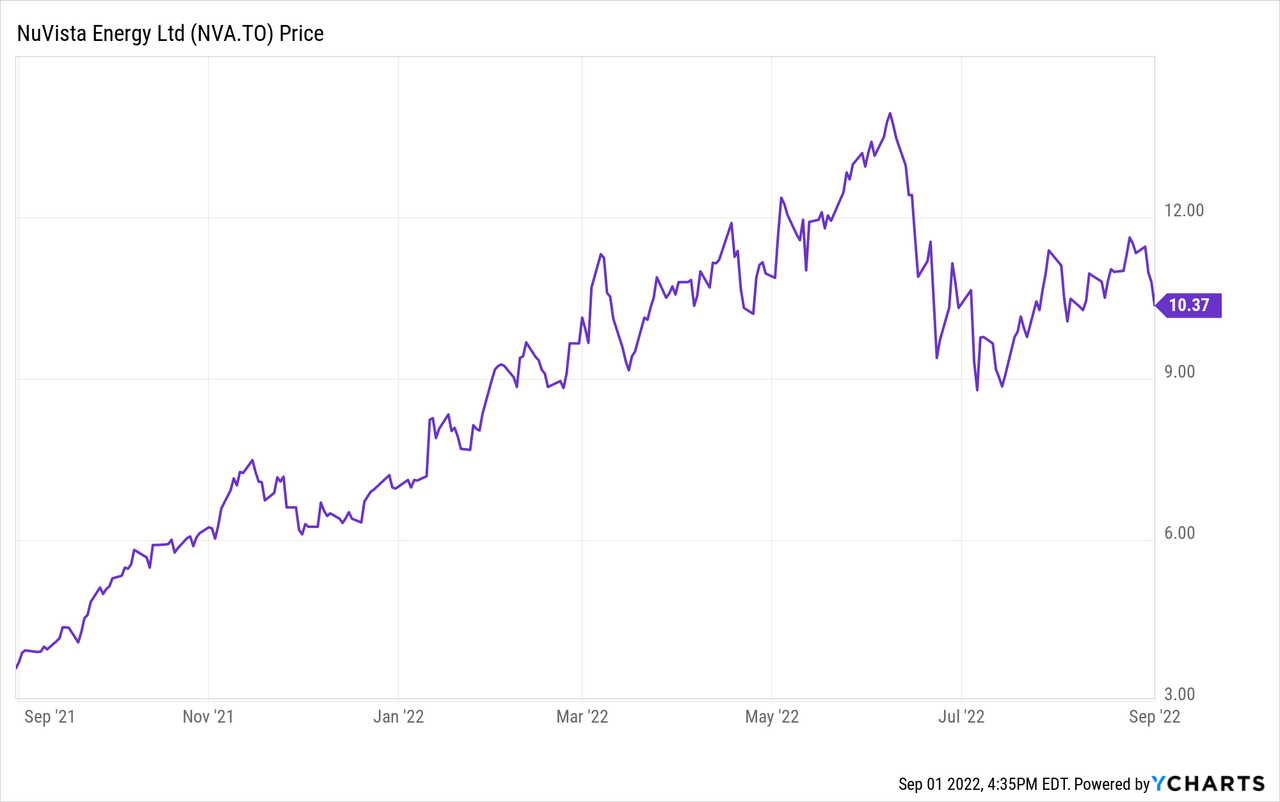

NuVista has a primary listing on the Toronto Stock Exchange where it’s trading with NVA as ticker symbol and a market capitalization of just over C$2.3B. With an average daily volume of in excess of 900,000 shares, the TSX listing clearly is the better option to trade in the company’s securities. The largest shareholder of NuVista with a stake of in excess of 16% is Paramount Resources (POU:CA) (OTCPK:PRMRF) which I discussed in this recent article.

Despite the hedge losses, the Q2 cash flows were superb

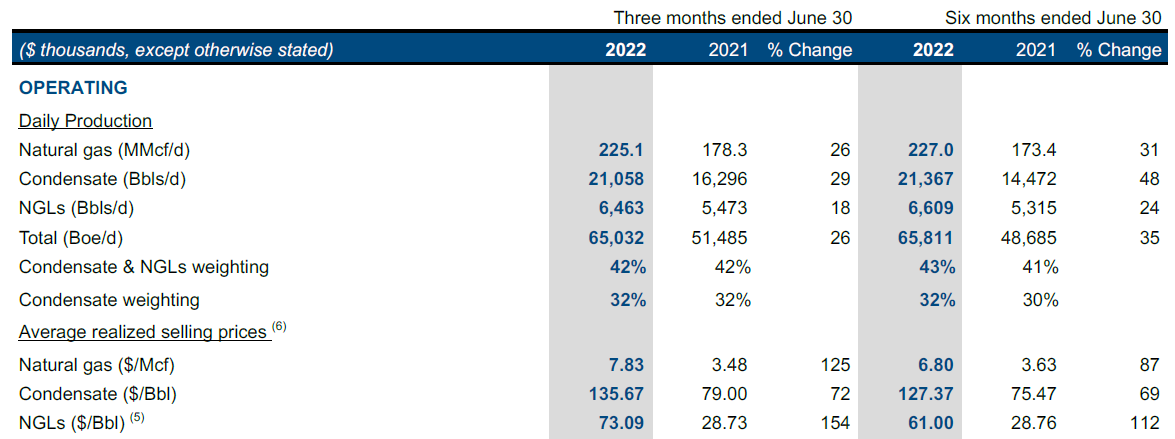

In the second quarter of this year, NuVista saw its production rate slightly decrease to just over 65,000 barrels of oil equivalent per day. About 60% of its oil-equivalent output actually consists of natural gas with just over 30% of the equivalent barrels contributed by the condensate production (which is sold at a price similar to the oil price). The NGLs made up about 10% of the production and thanks to a 154% price increase compared to the second quarter of last year for the NGLs and 72% for the condensate, these “by-products” added quite a bit of value to NuVista’s production profile.

NuVista Energy Investor Relations

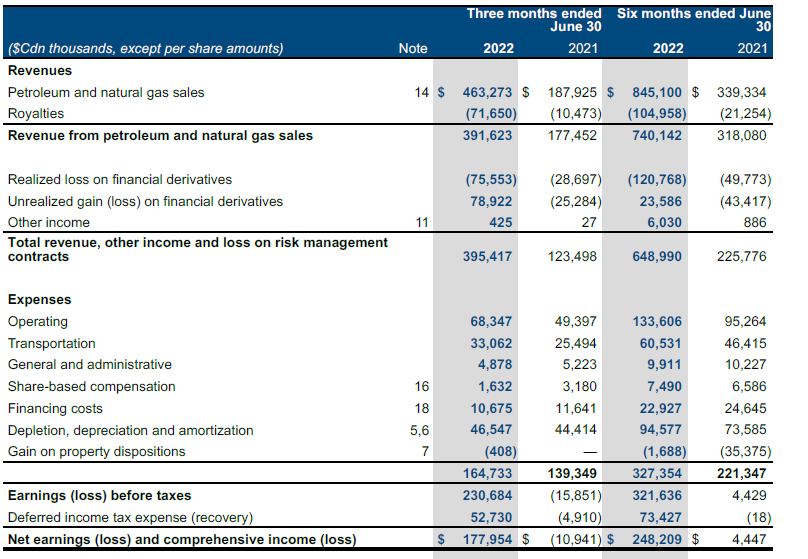

The combination of a higher production rate (compared to Q2 last year) and the much higher oil and gas prices caused the total revenue to increase by more than 150%, from C$188M to just over C$463M. And as you can see below, although the condensate represented just over 30% of the oil-equivalent output, it did represent about 60% of the total revenue so while NuVista for sure is a natural gas player based on the output, natural gas actually isn’t the most important commodity.

NuVista Energy Investor Relations

After deducting the royalties payable on the production of these fossil fuels, the net revenue was approximately C$392M, and after taking the hedges into consideration, the total revenue was C$395M. As you can see below, NuVista realized over C$75M in hedging losses but on other positions it reported an unrealized gain of almost C$79M. And as oil and gas prices have continued to go down, a bunch of those unrealized gains will likely soon be monetized.

NuVista Energy Investor Relations

The total amount of operating expenses was just under C$165M which means NuVista reported a pre-tax income of C$231M and a net income of just under C$178M for an EPS of C$0.78. A very good quarter indeed.

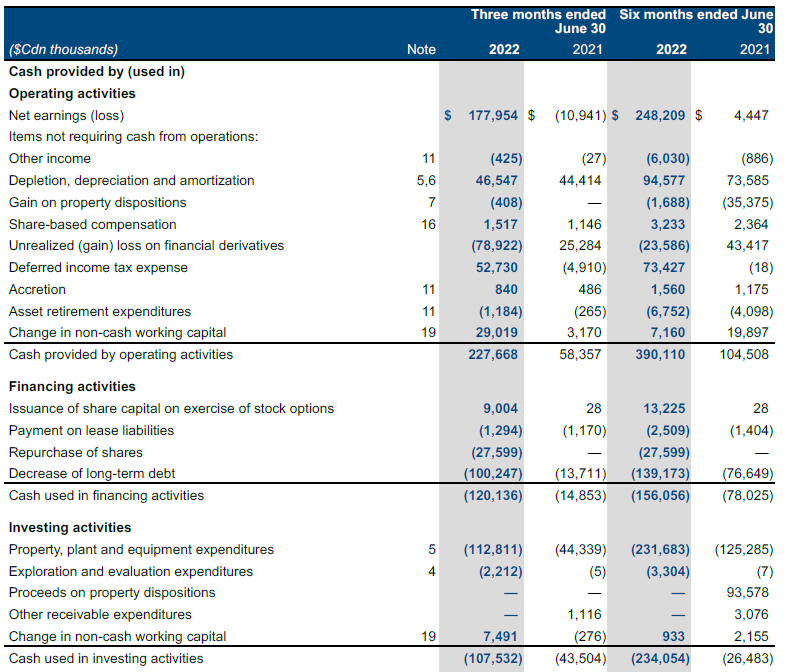

The cash flow result was also pretty strong, but investors are warned the operating cash flow includes the hedging losses but does not include the hedging gains as long as they weren’t realized. The C$228M in operating cash flow looks pretty impressive, but there are a few elements to take into consideration here.

NuVista Energy Investor Relations

First of all, there was a deferred income tax of almost C$53M. That’s fine for now as NuVista doesn’t expect to be taxable this year, but in its Management Discussion & Analysis document, the company clearly mentioned it expects to be cash taxable in 2023.

Secondly, there was a C$29M contribution from changes in the working capital while thirdly, the company also spent C$1.3M on making lease payments. Adjusting the operating cash flow for all these elements would result in an operating cash flow of C$145M. Keep in mind this still includes the approximately C$76M in hedging losses.

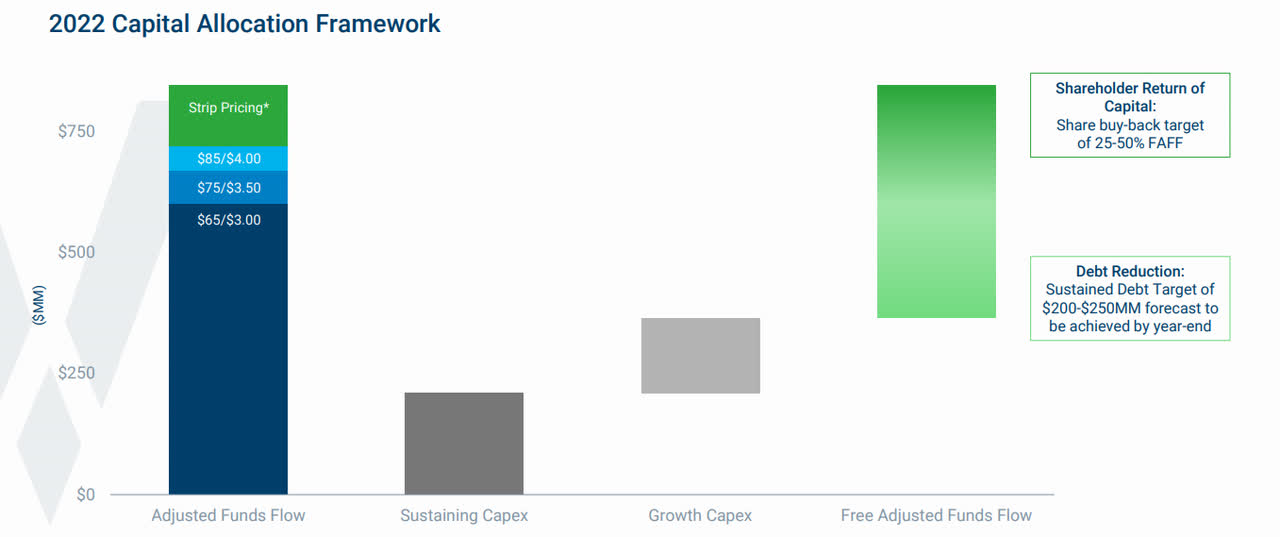

The total capex was approximately C$115M (bringing the H1 capex to just under C$235M). It’s however important to realize the capex does include a substantial amount of growth investments. As you can see below, NuVista’s anticipated sustaining capex is just under C$250M so I will add about 10% and use a sustaining capex of approximately C$70M per quarter, the adjusted operating cash flow in Q2 would have come in at about C$75M or approximately C$0.33 per share.

NuVista Energy Investor Relations

This means that even if you include the C$75.5M in hedging losses, NuVista is generating north of C$1.3 per share in free cash flow. And the image above tells us something else: Even if the oil rice would fall back to just US$65 WTI with NYMEX natural gas at US$3, the operating cash flow would still be approximately C$550-575M resulting in a free cash flow result of C$300M. While you could argue the AECO price is weaker, keep in mind NuVista often hedges the NYMEX/AECO differential as well. On top of that, natural gas is really just a by-product of the condensate production so the oil price will be more important for NuVista than the natural gas price.

Investment thesis

NuVista Energy has a reputation of being a natural gas producer but at the current commodity prices, the oil price is more important as its condensate production is (still) more valuable than the natural gas production.

Thanks to the strong performance in the second quarter, NuVista’s net debt (excluding lease liabilities) decreased to just C$280M (although one should also take the C$113M working capital deficit into account here). And although the oil and (non-NYMEX) gas price is getting weaker over the summer, the sensitivity analysis of the cash flows clearly shows that even at US$65 WTI and US$3 natural gas, NuVista is still trading at a free cash flow yield of 12%-13%.