bjdlzx

(This article was in the newsletter on July 17, 2022, and has been updated as needed.)

(Tamarack Valley is a Canadian company that reports in Canadian dollars. WTI is in United States dollars).

Tamarack Valley Energy Ltd. (OTCPK:TNEYF) just closed on yet another Clearwater acquisition. Management appears to have made a good deal with the whole purchase price being recovered rather fast. The increasing presence in this very profitable play will lead to some synergies as production increases.

The interesting part about this play is the very low prices that allow for a decent profit. Most of Clearwater appears to be heavy oil, although there are some reports suggesting that there may be some intermediate-grade oil deposits. The oil is a discounted product from WTI pricing. Therefore, when management suggests a certain payback or profitability level at a WTI price, there is an assumed discount relation that often changes at various pricing levels. This also means that management is factoring in a lower price received due to that discount when reporting various profitability levels. That is what makes the play so remarkable.

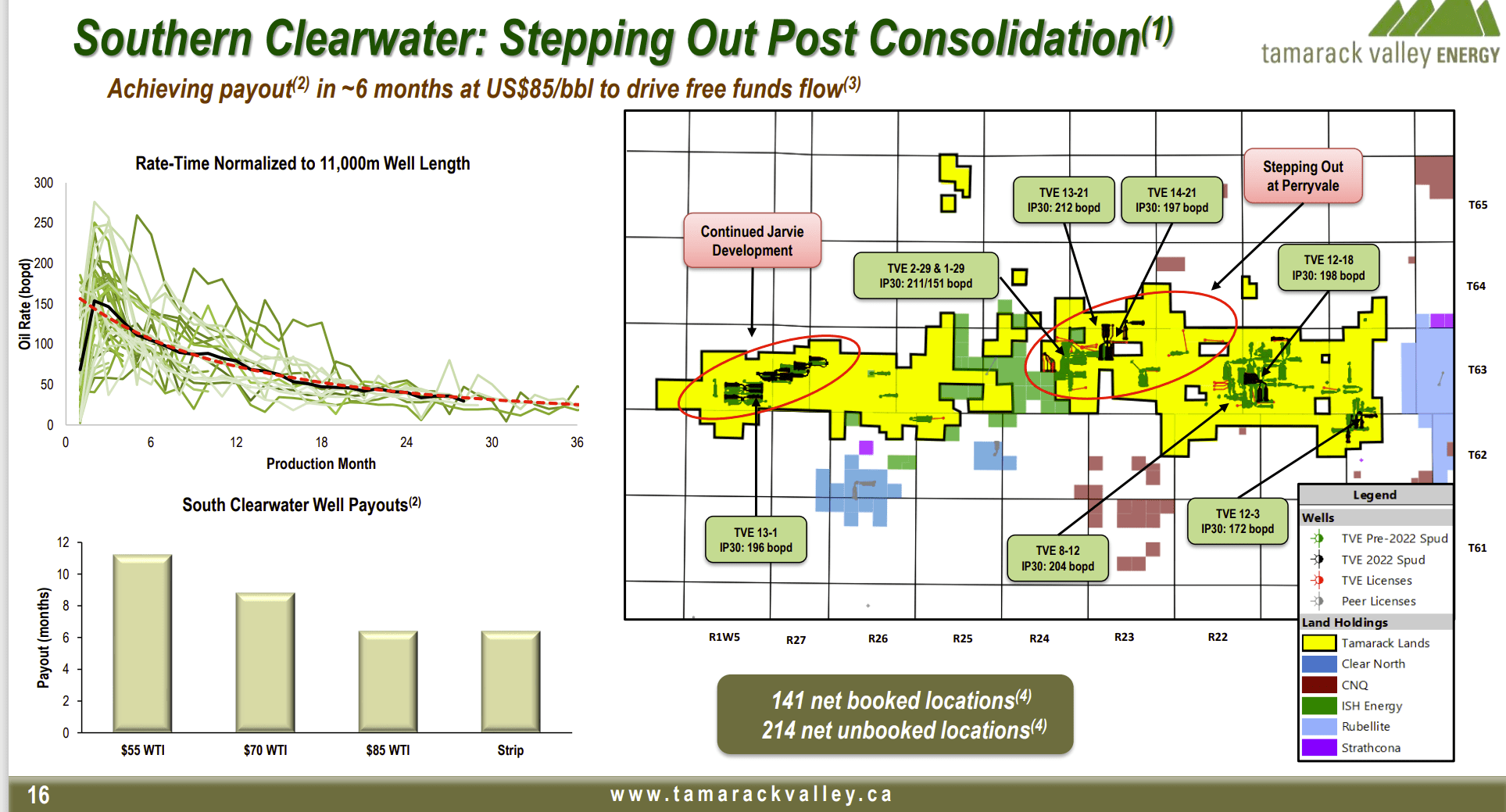

Tamarack Valley Southern Clearwater Profit And Performance Characteristics (Tamarack Valley July 2022, Investor Presentation)

Notice that the company can drill wells that payback in less than a year even at WTI $50 even though that means the company receives closer to $40 (depending upon the heavy oil discount). That is a remarkable profitability statement at that oil price level. Such a statement implies a breakeven point with a received price in the $20 range. That is an extremely low breakeven price in this industry.

In Canada, land is often cheap to acquire when compared to the United States. There is often, as in the case here, plenty of unclaimed acreage that can be a future expansion idea. Therefore, the way that companies achieve a higher valuation tends to be through higher profitability levels. This acreage with existing production and the owned infrastructure will be much more valued on any sale of the company than would non-producing acreage.

In the meantime, the graph above demonstrates that wells continue to outperform their older peers. That means that optimization proceeds and probably advancing technology will cause future wells to continue at a pace that is not currently predictable.

Should technology continue to advance, then the Clearwater Play appears to have several intervals that are currently not producing that are likely to become commercial in the future. This area could be a source of low-cost production for a very long time to come.

Acquisition Strategy

Management continues to acquire properties as long as they can use stock to keep the debt ratio low. This is important as the company is fast reaching production levels where management may consider issuing bonds at some point through the bond market. Currently, the debt is handled in small company fashion.

Using stock is important because it lowers the risk of rapid growth. This management appears to be growing the company to make it an attractive acquisition candidate. Therefore, investors should expect a fair amount of growth along with a relatively large capital budget. A dividend will not be a major source of investors’ returns.

The latest dividend is now C$.01 per share per month. Investors should expect that the dividend will grow with accretive acquisitions made. But that dividend will also remain a relatively small amount of cash flow. Companies with a strategy like this one are aiming for primarily capital gains.

New Issue Discount

Tamarack Valley is a relatively new company that lacks a track record. Management does have considerable past experience. But what matters to the market is the performance of this company as it is currently put together. Therefore, investors should not be surprised if the acquisitions strategy “starts the clock over” because the market views the company after an acquisition as a new entity.

Any seller that acquires stock may at any time in the future sell that stock. Therefore, a company that uses stock for acquisition purposes may have time periods of common stock weakness when one of these sellers exists the position.

Long-term, more stock outstanding will create a larger, more efficient market for the company’s common stock. This will also make using common stock to execute transactions an easier task. Smaller transactions would then have little to no effect on common stock price performance. But the beginning period, which is still right now, could have periods of considerable volatility.

This makes management experience important. Investors can consider this investment anytime like the present when that “new issue discount” appears in full force because of the management experience. The new company risk is much lower as a result. Therefore, an asymmetric return with more upside potential is very likely.

Light Oil

Management is balancing the heavy oil presence with some enticing light oil possibilities. Clearwater is an unusual play with such a low WTI breakeven point for a discounted product like heavy oil. However, there is always the risk that the discount expands during times of pricing weakness. Therefore, some premium production of light oil or even condensate is indicated to offset some of the heavy oil profit volatility.

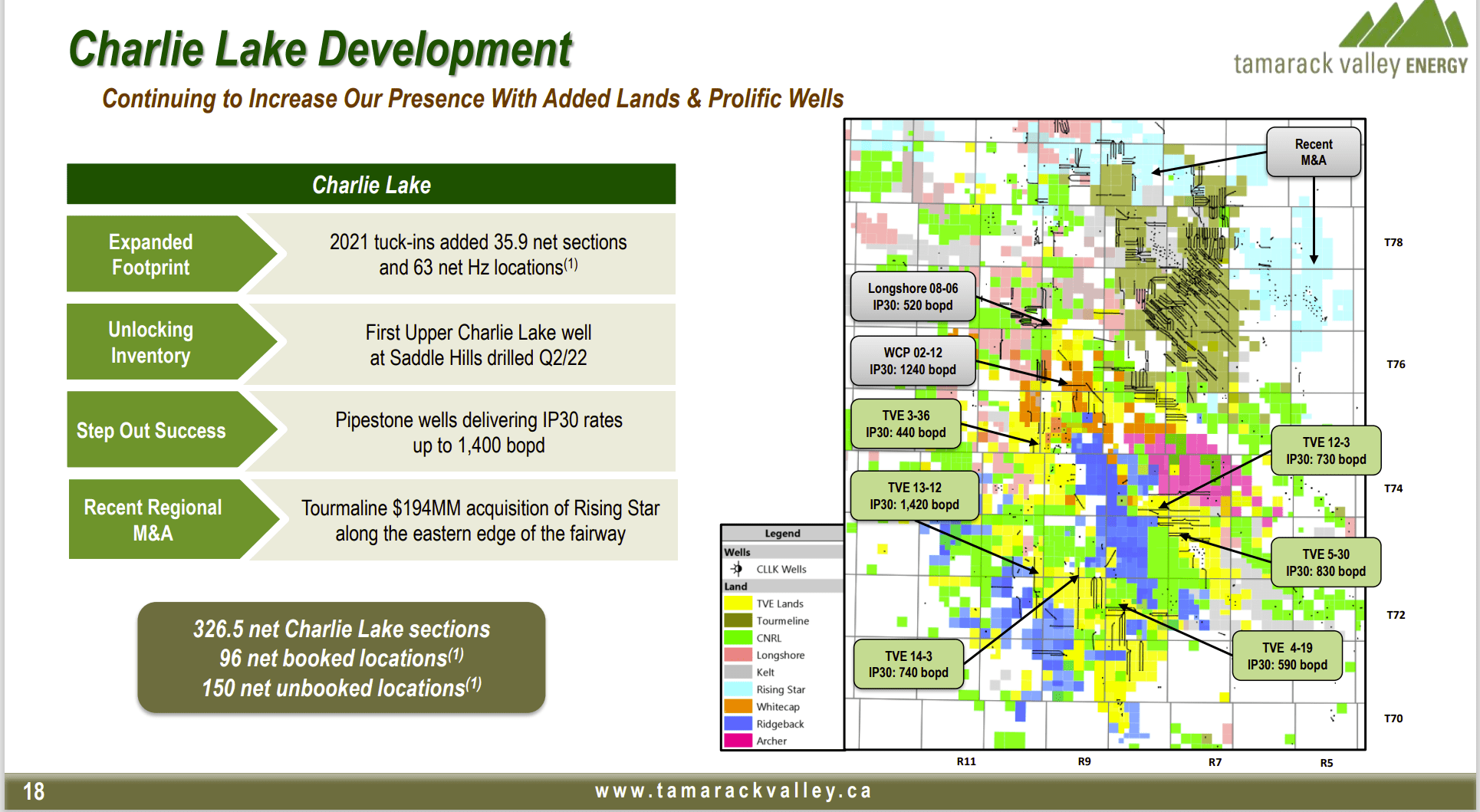

Tamarack Valley Charlie Lake Well Success Map And Lease Holdings (Tamarack Valley July 2022, Corporate Presentation)

Charlie Lake is an area I have covered under several different presentations by other companies. It has some darn good acreage. Yet the play does not appear to get all that much publicity. It finally seems to be getting the development attention it deserved years ago.

Management has some darn good possible development opportunities here. A lot of expensive infrastructure is already in place. Therefore, incremental production growth is rather easy.

The real question is the proper production mix of this play and the Clearwater play for the company to properly get through an industry downturn. Both plays are very profitable. However, profits can (and often have) disappeared from heavy oil plays during cyclical downturns to the point that heavy oil production was shut in to minimize cash losses.

The Future

Management is likely to opportunistically acquire property in the future. The latest acquisition should pay back within one to one-and-one-half years of the closing. That makes it easy to protect that kind of assumption through hedging should management think hedging is necessary to protect cash flow.

The use of stock in the acquisition keeps key financial ratios lower. So, the financial risk typical of relatively new companies is also lower. This management has experience building and selling companies. That also lowers the typical new company risk.

The combination of growth by organic drilling and development as well as acquisitions is attractive at the current price of the stock. Some holders may want to “buy and hold” as management is likely to sell the company at a decent profit at some point.