JHVEPhoto

Luminar Technologies (NASDAQ:LAZR) collapsed on a downgrade by an analyst questioning the design wins of the Lidar sensor company. Luminar was the original Lidar SPAC and considered the leader in the space when the Gores Metropoulos SPAC took the company public. My investment thesis is far more bullish on the stock after the selloff due to the irrational panic with the stock below $8.

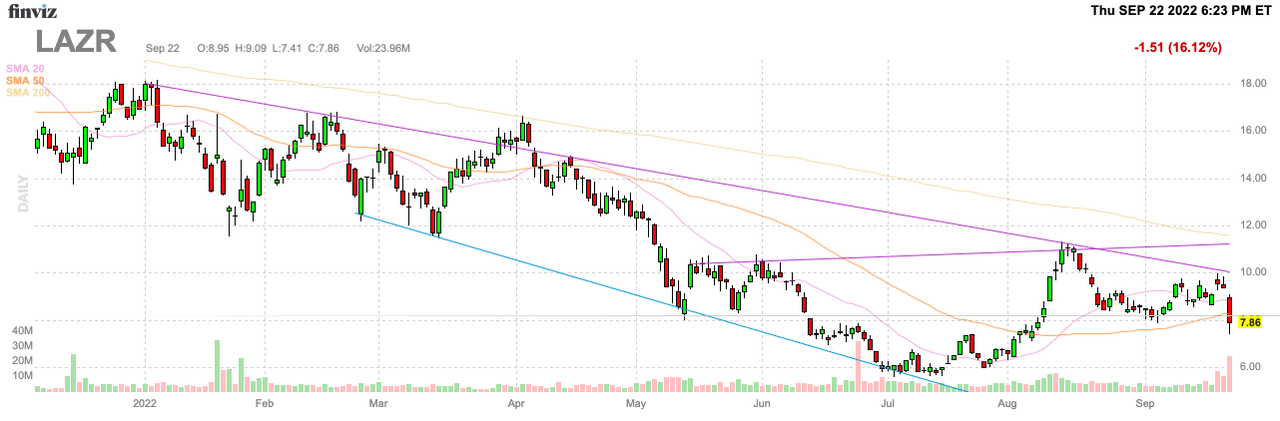

Source: FinViz

Luminar Stock Gets Big Downgrade

Northland Securities downgraded the stock and reduced the price target to $10. The analyst questioned whether Lidar adoption was taking longer than expected and more importantly hinted at auto OEMs selecting less expensive alternatives.

The firm had previously had a $13 price target on Luminar, so the shift to a Market Perform position and a cut to the price target by 23% was a rare drastic shift by an analyst. After all, the stock had already fallen back below $10.

For its part, Luminar had already guided to the forward-order book growing at a 60% clip this year, up from a forecasted 40% growth rate. The company started the year with a $2.1 billion forward-order book covering orders through 2026 and the upgraded growth target predicts the company ending the year with a $3.4 billion amount.

Earlier this year, Innoviz Tech. (INVZ) announced a massive $4.0 billion order from a subsidiary of Volkswagen (OTCPK:VWAGY) pushing their total order book through 2030 at $6.6 billion. The key here is that Luminar didn’t win this deal, but also Innoviz has announced numbers through 2030 which aren’t comparable to what Luminar provides regarding the order book.

At the recent Evercore conference, Luminar didn’t provide any indication of the company failing to meet these prior corporate goals. In fact, CFO Thomas Fennimore had the following positive comments about industry development and design wins:

Our products are going to start to go on vehicles being sold to consumers around the end of this year. Our first wave of customers include Volvo, Polestar, Mobileye, Shanghai Auto. And then our second wave of customers will include names like Mercedes-Benz, Nissan, Daimler Truck and a few others. And so we are on the verge of start of production, which will see a significant increase in our revenue here in short order.

The CFO further highlighted how the order book includes only one vehicle from Volvo (OTCPK:VOLAF) with the ability to greatly expand beyond this initial start. Innoviz includes a multi-vehicle deal with plans for 5 to 8 million units. The Nissan Motor (OTCPK:NSANY) deal offers Luminar a similar option to supply Lidar to their full 4 million annual production targets, but neither deal is included in the current forward-order book.

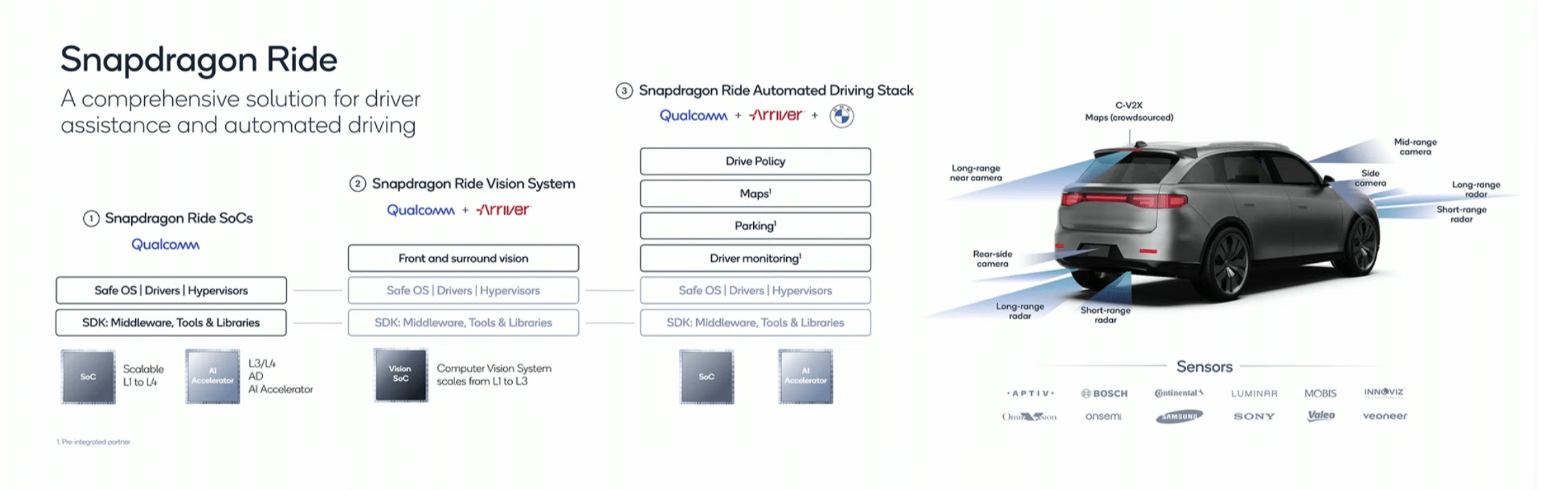

At their Auto Investor Day, Qualcomm (QCOM) announced a massive boost in the design-win pipeline from $19 billion back in July to $30 billion now. The wireless chip giant suggests the Snapdragon Ride platform includes sensors from both Luminar and Innoviz, but the company didn’t provide any indication of how the order book breaks out into various buckets that include digital cockpit and connectivity beyond the opportunity in automated driving.

Source: Qualcomm Auto Investor Day

Playing The Long Game

One of the great advantages to Luminar is that the company has a strong balance sheet with $605 million of cash in the bank. The company can afford to aggressively spend to develop the Lidar sensors needed to meet auto OEM demand over the next decade.

The stock value is down to $2.8 billion and has again dipped below the order book level. Luminar will provide updated financial targets at an Investor Day in Decembers that could bolster confidence in the business.

Luminar might not hit the original revenue targets where sales were forecasted to hit $418 million in 2024 and jump to $837 million in 2025. The recent details don’t suggest the company should stray from the analyst targets at $353 million in 2024 doubling to $797 million in 2025 and reaching $1.4 billion by 2026.

The combined revenue estimates of analysts through 2026 only reaches $2.6 billion, or some $0.8 billion below the current forward-order book total. The market probably expected Luminar to public state larger order books than other Lidar sensor corporations, but the numbers aren’t always comparable and the company appears on target for more recently stated goals.

Takeaway

The key investor takeaway is that the selloff in Luminar Tech. appears irrational. The Lidar sensor company appears on track to hit goals. The market is oddly most bearish as Luminar approaches production launches and could snag some major contract expansions.