Justin Sullivan

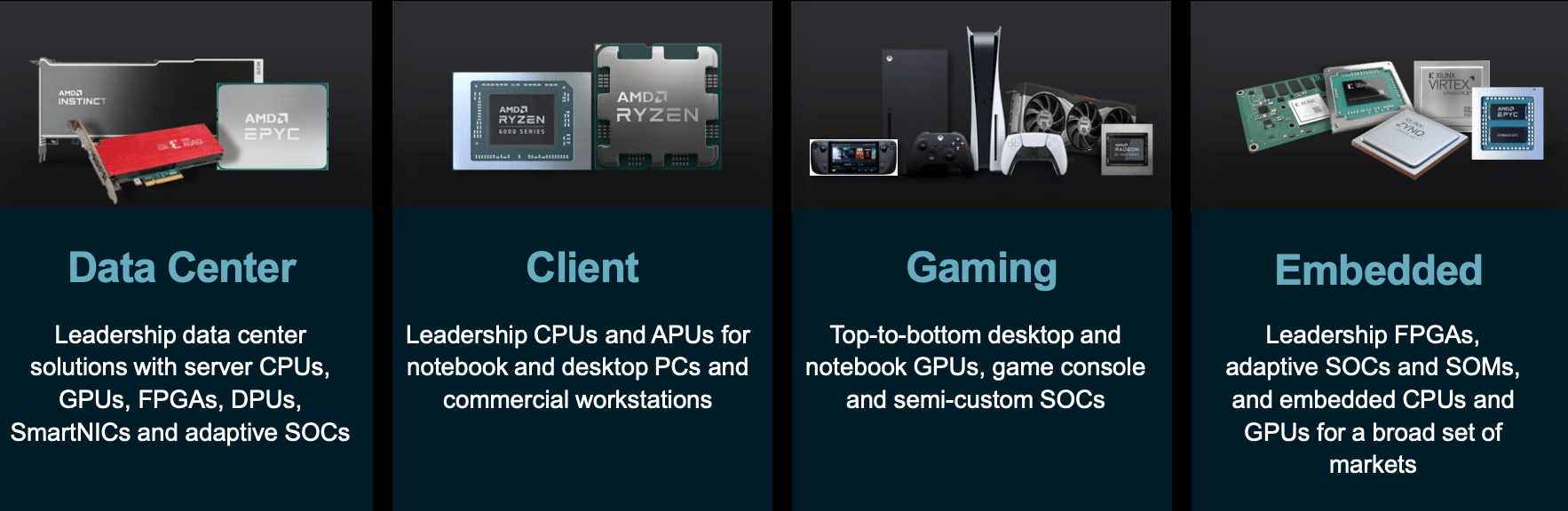

AMD (NASDAQ:AMD) is a leading chip designer which specializes in high-performance chips for PCs, Data Center Servers, Gaming (PlayStation and Xbox), and more.

AMD business model (Q3,22)

The company is poised to benefit from the secular growth across its main industries such as Gaming, Embedded, and of course Data Centers (Cloud). The global cloud computing market was valued at $405 billion in 2021 and is forecasted to grow at a rapid 19.9% compounded annual growth rate, reaching a value of over $1.7 trillion by 2029. Thus in this post, I’m going to break down the company’s business model, financials and valuation, let’s dive in.

Growing Financials

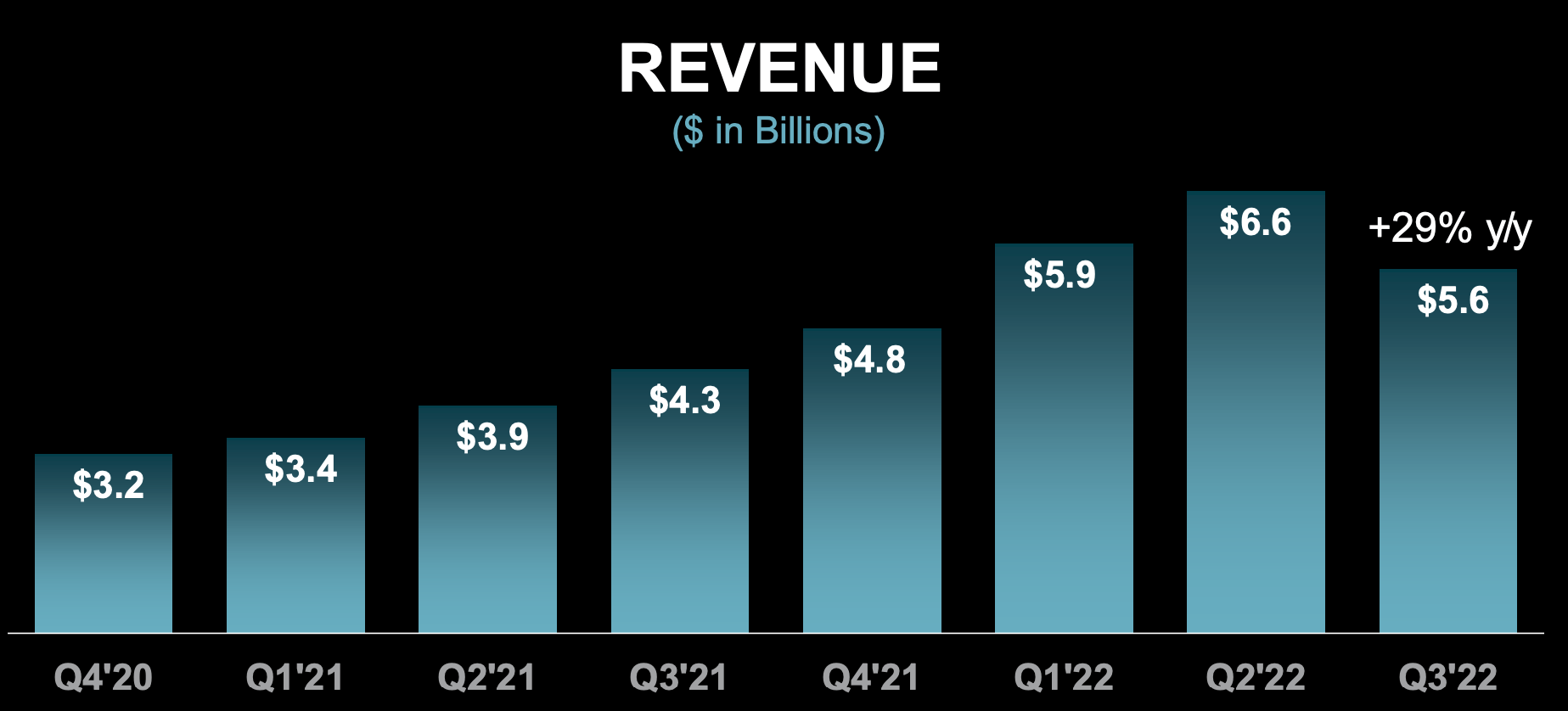

AMD generated solid financial results for the third quarter of 2022. Revenue was $5.6 billion which increased by a rapid 29% year-over-year. The growth was driven by strong data center and embedded segment results. However, revenue did miss analyst expectations by $84 million, which was mainly due to a decrease in Client segment revenue which was driven by a weak PC market, at a macro level.

AMD Revenue (Q3,22)

Data Center Strength

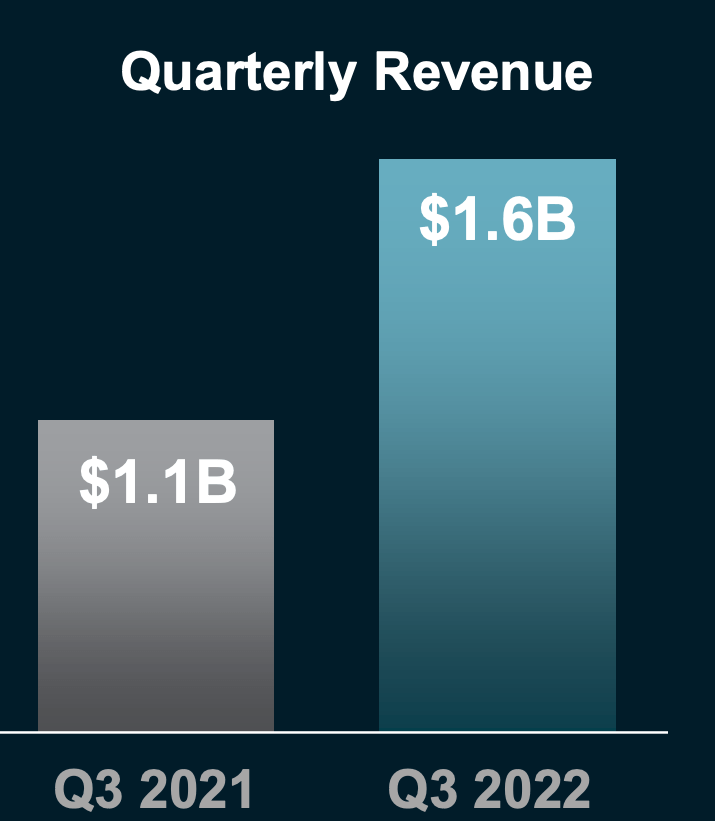

AMD’s Data Center segment generated solid growth with revenue increasing by a blistering 45% year-over-year or 8% quarter-over-quarter to $1.6 billion. AMD is one of the leading providers of server processor chips for data centers. For instance, its EPYC server processor chip has been dubbed the “world’s highest-performance server processor”. According to one study, AMD EPYC processors have demonstrated “better performance” in purely CPU-based operations when compared with Intel Xeon (INTC). EPYC chips also reportedly cost less than the Intel equivalent and are more energy efficient. Therefore it’s no surprise that AMD’s server chips had their 10th consecutive quarter of record sales.

AMD EPYC chip (AMD)

It products are already deployed across the three major providers of Cloud Infrastructure; AWS, Microsoft Azure, and Google Cloud. AMD’s chips are also found inside the data centers of China’s major cloud providers such as Tencent Cloud, Baidu and Alibaba Cloud. Over 70 new instances were launched in the third quarter and its product has a tilt toward optimizing high-performance computing [HPC] and Artificial Intelligence [AI] applications.

AMD has also started to ship its next-generation Genoa CPU, which offers even greater performance and energy efficiency than its predecessor. This continued innovation means it is likely AMD will extend its lead in the market and eat more market share away from Intel.

AMD Data Center Revenue (Q3,22 report)

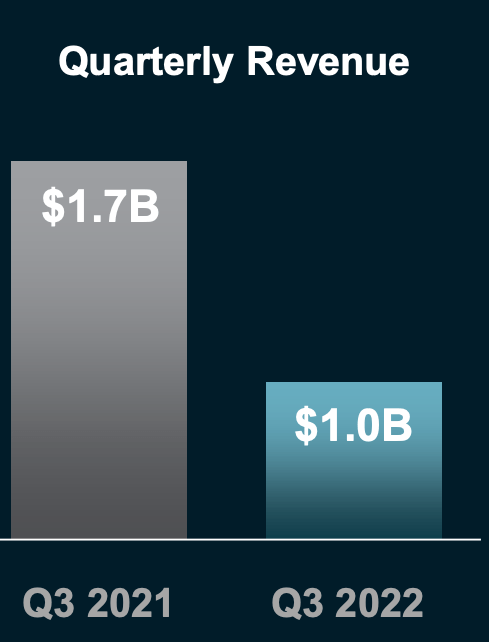

Declining PC Revenue

AMD reported poor client segment revenue of $1 billion, which declined by an eye-watering 40% year-over-year. This was mainly driven by the macroeconomic environment which has resulted in softer demand for PC. During the lockdown of 2020, gaming and PCs had a major boost in sales at an industry level as people upgraded their home computers and businesses purchased more laptops for hybrid workers. However, now we are seeing a correction in this demand, and channel partners are focusing on reducing excess inventory. The good news is the computer market tends to be cyclical by nature, therefore, I forecast a bounce back in the future.

AMD Client (Q3,22 report)

AMD’s gaming segment performed slightly better with revenue increasing by 14% year-over-year to $1.6 billion. This was driven by strong demand for its game console devices as Sony and Microsoft prepared for the holiday season, with their PlayStation and Xbox consoles.

AMD is also launching its new RDNA GPUs (Graphics Processing Units) on a 5nm (nanometer) chipset, which offers higher performance over prior versions. AMD competes directly with Nvidia (NVDA) for graphics cards which dominate the market.

Super Embedded Growth

Embedded segment revenue jumped by over 1,500% to $1.3 billion. This was mainly driven by the recently acquired Xilinx, a leader in FPGA (Field Programmable Gate Array) products. AMD acquired Xilinx in 2020 for a staggering $49 billion, but the transaction didn’t close until 2022. As a former electronics major many years ago, I remember using FPGAs in labs and was told this would be “the future”. FPGAs can be “reconfigured” or changed in the “field,” which gives them greater flexibility over an Application-specific Integrated Circuit [ASIC]. They also offer high performance and great energy efficiency characteristics. Therefore it’s no surprise that Xilinx’s products are used in the Mars Rover and many other mobile applications such as fighter jets, automobiles, etc.

Xilinx FPGA (Xilinx Website)

In the third quarter of 2022, AMD has started to ramp up its shipments of the Xilinx FPGA to consumers. The Energy Sciences Network chose to use Xilinx’s Network accelerator card (Alveo U280) for the U.S. Department of Energy’s next-generation network.

AMD now competes directly with Intel on another front, as Intel acquired Xilinx competitor Altera for $16.7 billion in 2015.

Profitability and Expenses

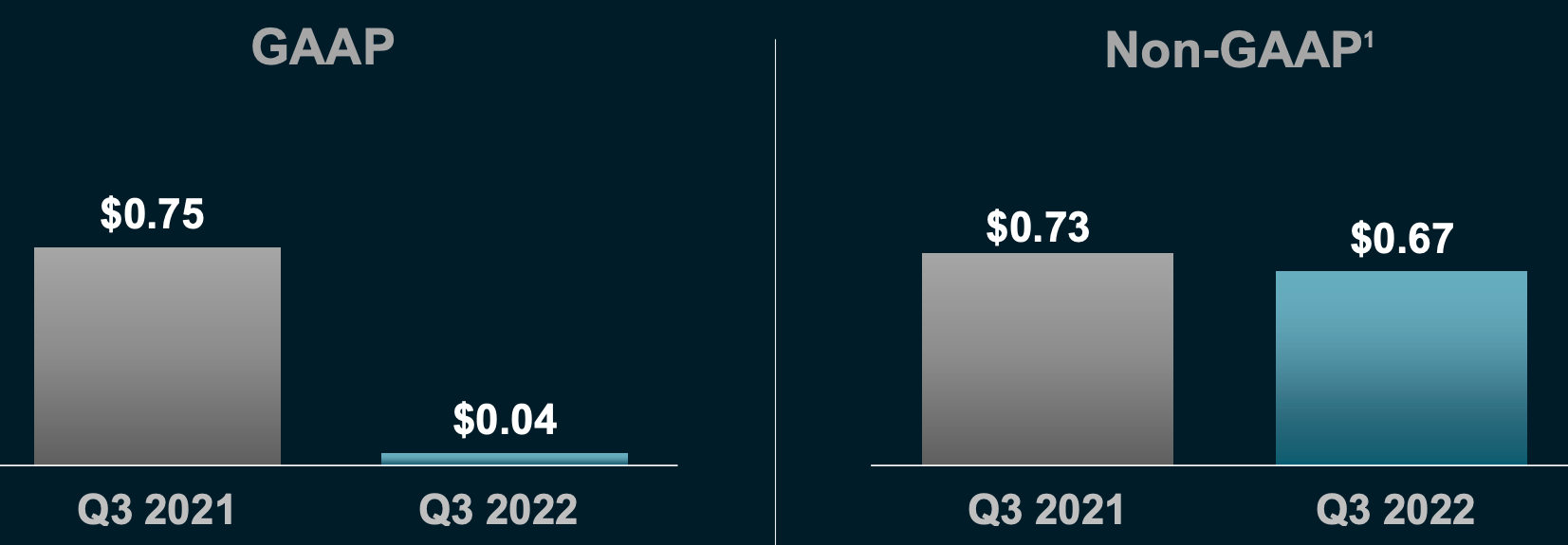

AMD reported earnings per share of $0.04 in the third quarter of 2022, which missed analyst expectations by $0.06. This was down substantially year-over-year, negative 95%. This was caused by a $500 million increase in Operating Expenses. In addition, ~$516 million less in client segment profit as its channel partners sell products at a discount to offload inventory, as demand waned. There was also $89 million less in gaming profit reported in the third quarter of 2022. In addition, there was amortization of some acquisition-related costs (Xilinx). The good news is the majority of these issues are likely to be cyclical by nature. As I mentioned prior, the PC and Gaming markets are going through a cyclical decline. A study by PwC indicates that total gaming revenue is forecasted to increase by ~36% by 2026, which is a strong signal the industry will grow again. On a Non-GAAP basis, EPS was $0.67, which was down 8% year-over-year.

Earnings Per Share (AMD Q3,22)

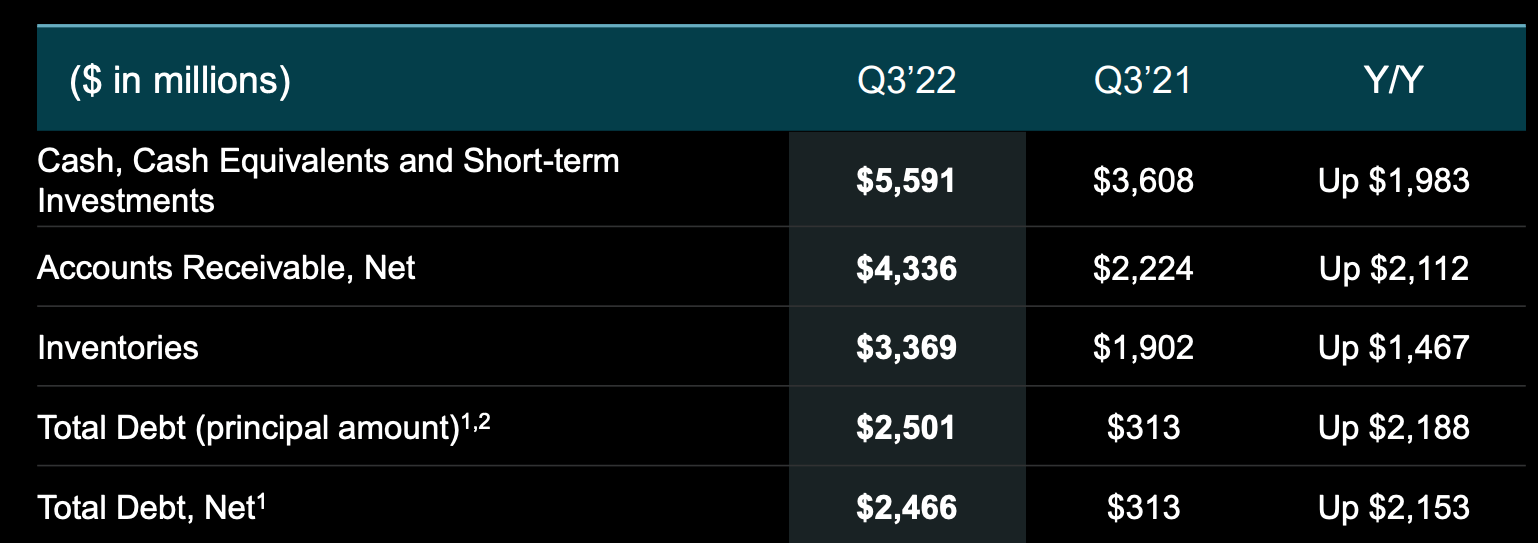

AMD has a solid balance sheet with $5.59 billion in cash, cash equivalents and short-term investments, which has increased by $1.98 billion year-over-year. In addition, the company has total debt of $2.466 billion, which is manageable. I believe the major changes in the balance sheet are a result of AMD’s acquisition of Xilinx.

AMD Balance Sheet (Q3,22 report)

Advanced Valuation

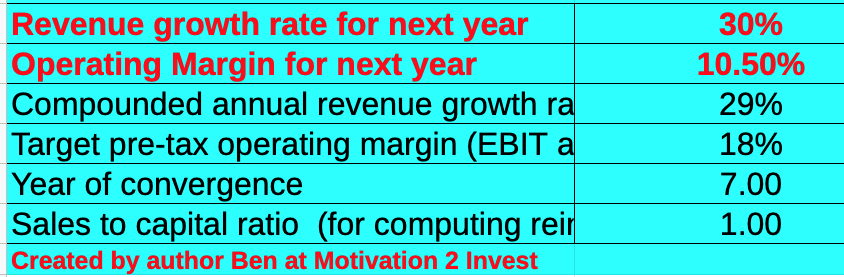

In order to value AMD, I have plugged my latest financials into my advanced valuation model, which uses the discounted cash flow method of valuation. I have forecasted a conservative 30% revenue growth for next year and 29% over the next 2 to 5 years. This is in line with historic growth rates and fairly prudent, given I forecast the economy to rebound in years 2 to 5.

AMD stock valuation 1 (created by author Ben at Motivation 2 invest)

In order to increase the accuracy of the valuation, I have capitalized the company’s R&D expenses, which has lifted its operating income. I am forecasting an increase in operating margin to 18% over the next 7 years, as the Client and Gaming segment rebounds.

AMD stock valuation 2 (created by author Ben at Motivation 2 Invest)

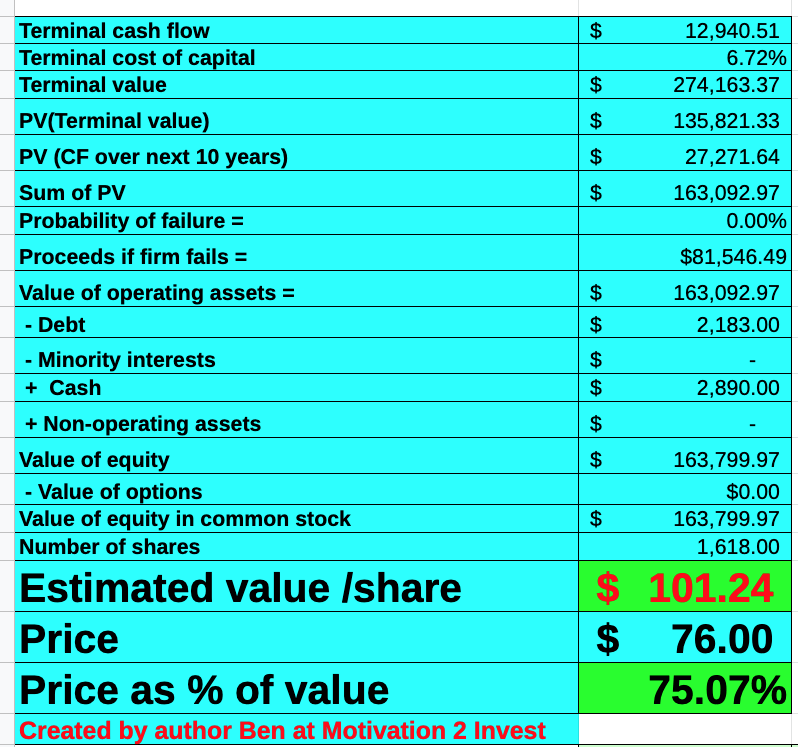

Given these factors, I get a fair value of $101 per share, the stock is trading at ~$76 per share at the time of writing and thus is 25% undervalued.

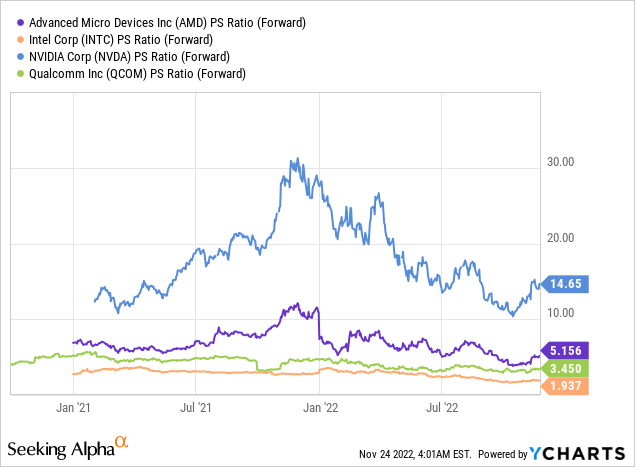

As an extra datapoint, AMD trades at a price-to-sales ratio = 5, which is 14% cheaper than historic levels. Relative to industry peers, AMD is trading at a mid-range valuation; Intel is much cheaper with a PS ratio = 1.9, but the company is facing many issues with its foundry business.

Risks

Recession/Cyclical PC Decline

The high inflation and rising interest rate environment have caused many analysts to forecast a recession. This is not great for any business and may cause longer sales cycles and delayed spending. The cyclical decline in PC and Gaming is also an issue for companies in the industry, who are having their profits squeezed in the short term.

Final Thoughts

AMD is a strong innovator and true leader when it comes to its Data center server chips. The recent acquisition puts the company head-to-head with Intel. Intel is currently facing a series of manufacturing issues and delays. Therefore, this is the optimum time for AMD to eat market share and potentially steal Intel’s crown long term. The stock is undervalued intrinsically and thus it could be a great long-term investment.