cosmonaut/iStock via Getty Images

LiveRamp Holdings (NYSE:RAMP) operates a SaaS-based platform offering a privacy safe ecosystem. Back in February of last year, I noted that growth was slowing and advised investors to Take The Off-Ramp due to the stock’s extremely high valuation level relative to its new – slower – growth trajectory. The stock is down 65% since that article was published. However, today that stock is strongly bucking a down market due, apparently, to yesterday’s announcement that its share buyback plan had been increased to a whopping $1.1 billion. Is this an opportunity for investors?

Background

Back in August 2020, I had been bullish on LiveRamp’s “Securely Connecting In A Cookieless World” theme. After all, quarterly revenue had just jumped 35% and it appeared RAMP was designing an attractive platform that was being adopted by some well-respected companies.

However, in November of that year, that macro-environment appeared to turn negative for RAMP when Apple (AAPL) announced changes in its iOS that appeared to obviate the need for RAMP’s authenticated traffic solution (“ATS”) platform. I changed my rating to HOLD on slowing revenue growth and weak forward guidance.

I went to an outright sell in February of 2021 with my “Off-Ramp” article referenced earlier, and when the valuation at the time (forward P/E = 330x) seemed totally inconsistent with quarterly revenue growth of only 16%. On top of that, the company’s forward guidance indicated a further deceleration of revenue growth.

But that was then, this is now. Let’s take a look at the most recent earnings report.

Earnings

RAMP released its Q2 FY23 earnings report in the first week of November. Highlights were:

- Revenue of $147 million was +15.7% yoy, and a $3.63 million beat.

- Subscription revenue was $120 million, +14% yoy.

- GAAP earnings were a loss of $0.45/share.

- Net cash provided by operating activities was $21 million.

Note that stock-based compensation was $27.3 million – more than the net-cash from operations. Still, CFO Warren Jenson said:

In this period of uncertainty, we’ve tightened our belts. As a result, we’re increasing our FY23 non-GAAP operating income guidance to approximately $60 million, representing growth of more than 40% year-on-year.”

Indeed, in November, RAMP made a regulatory filing disclosing a 10% reduction in full-time employees and a planned downsizing of its real estate footprint. The actions are expected to result in annualized operating expense savings of $30-35 million.

For full-year FY23, LiveRamp raised its guidance and now expects to report revenue of $595-$600 million, an increase of 13% yoy. That’s a particularly tight range and may indicate that management has a fairly clear line-of-sight into achieving that revenue estimate. Still, the company expects a GAAP-loss of ~$102 million, and non-GAAP operating income of ~$60 million.

The Buyback Plan

While Q2 revenue growth was solid and better than expected, the company is still losing money on a GAAP basis and continues to burn through cash.

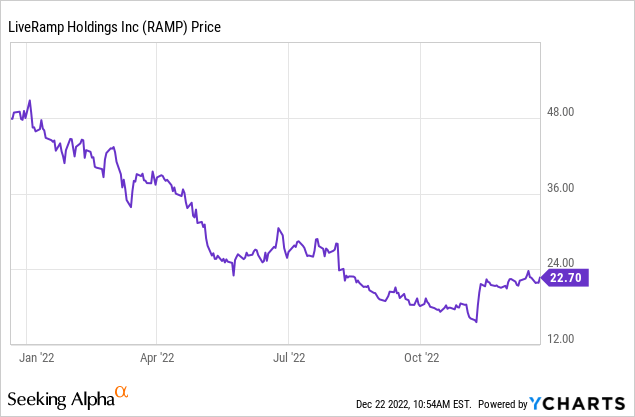

Back in February, at the time of my “Off-Ramp” article, RAMP had cash-on-hand of $663 million. At the end of Q2 FY23, the cash balance had dropped to $485.6 million (down 19% yoy). Much of the cash decline was the result of repurchasing shares at much higher prices than its current level:

Meantime, despite the share buybacks (more on that in a minute …), and thanks to the company’s very generous stock-based compensation plan, RAMP’s fully-diluted outstanding share-count has actually expanded by ~250,000 shares over the past year.

As for the buybacks, in Q2 RAMP reported it had bought back 1.7 million shares for $40 million during the quarter. That works out to an average of $23.52/share, about where the stock is today. Fiscal year to date, RAMP has repurchased ~3.8 million shares for $100 million, or an average of $26.32 – significantly above the current price. While RAMP says it has returned $1.3 billion in capital to shareholders since 2011, investors can see from the stock chart above (and the 10-year chart at the end of the article) that much of that capital was spent on stock at significantly higher prices. And again, the share count is still expanding, not contracting as investors should expect given such a large allocation of shareholder capital to buybacks.

That brings us to yesterday’s announcement that the share buyback authorization was increased by $100 million to $1.1 billion. With the increase in the program, and in consideration of previous purchases, the company said it had ~$215 million available for stock buybacks over the next two years (the plan expires at calendar year-end 2024).

So that means there are nine fiscal quarters left until the buyback expiration date. All things being equal (but acknowledging they seldom are…), that equates to a ~$24 million per quarter buyback run-rate. Which appears quite doable considering the company still has $486.5 million in cash, is growing revenue at ~15%, its net-cash generation from operations ($21 million in Q2), and its relatively strong forward guidance.

Valuation

Meantime, according to Seeking Alpha, RAMP stock is currently trading with a forward P/E of 29.5x. However, that’s obviously based on non-GAAP earnings as the company is still not GAAP profitable – Yahoo Finance reports TTM earnings of -$0.50/share.

Risks

RAMP has no debt, so its balance sheet is super-solid considering its large cash position.

The market in which RAMP operates is constantly changing, and the company’s platform needs to react to sometimes rapidly evolving conditions – some of which are out of its control (the Apple privacy changes, for instance).

Given the bear market of 2022, investors are looking for GAAP earnings and strong free cash flow. And, in general, I would say investors don’t like to see overly generous stock-based compensation, wherein investor capital is arguably being funneled straight back to corporate executives instead of to shareholders. I say that because, as I pointed out earlier, despite the share buyback plan, RAMP’s outstanding share count continues to expand.

Summary and Conclusions

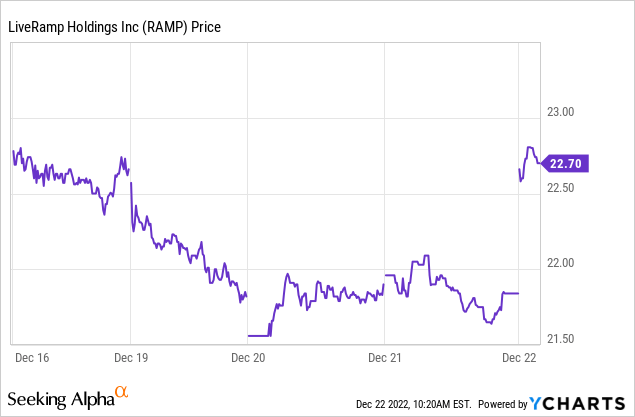

Taking everything into consideration – the demonstrated revenue growth, strong cash position, 50%-plus stock decline, operating expense control – I’m changing my rating on RAMP from sell to buy. It’s still somewhat of a risky proposition given the company has still not figured out how to report GAAP earnings and is still recording stock-based compensation that is too high, in my opinion. However, cash flow is positive, and the large cash position is a source of strength: The $485.6 million in cash equates to an estimated $7.24/share in cash while – at pixel time – the stock is trading at $22.39.

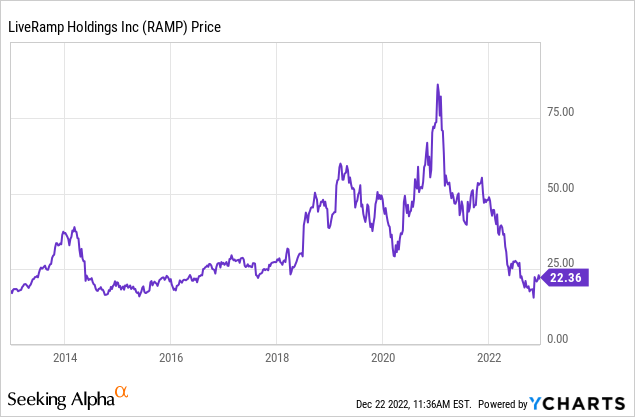

I’ll end with a 10-year chart of RAMP’s stock price and note that it’s now below where it was in 2017: