AndreyPopov/iStock via Getty Images

Investment Thesis

Anheuser-Busch InBev SA/NV (BUD) produces, distributes, and sells beer, alcoholic beverages, and soft drinks globally. It has about 500 beer brands in its portfolio, such as Budweiser, Corona, and Stella Artois. Even though the company has different geographical locations and products, it has been going downhill since 2016. This may be because of the effects of its high debt levels.

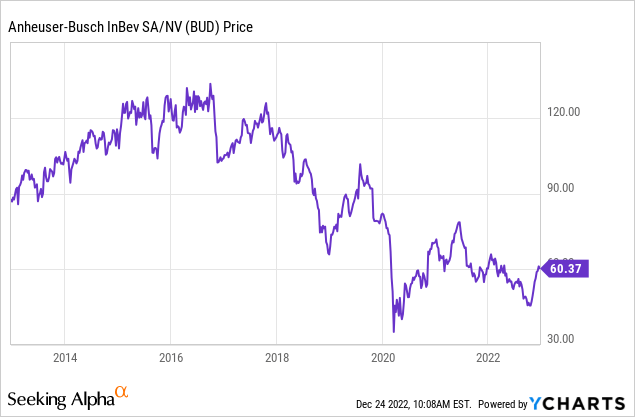

The company’s debt has been paid down significantly after being extremely high for quite some time. The corporation has begun to show signs of improvement after executing this deleveraging process. In my opinion, the company’s excellent deleveraging plan will allow it to continue the upward trend in its stock price, which has been going strong since October. Once the remaining debt is paid off, I expect the company’s development to be fueled by the benefits gained from effectively utilizing the debt load. This, along with the company’s global diversification, which I think protects it from economic downturns in individual states, will keep the company in a good position for the long term.

Global Diversity

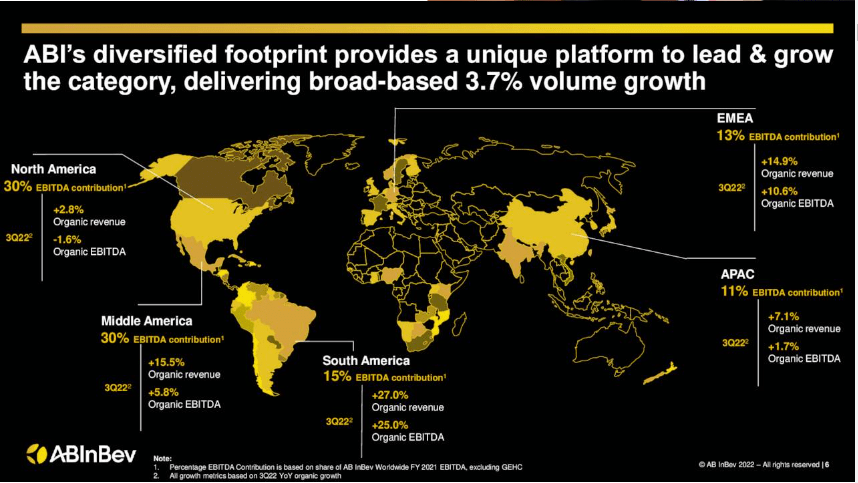

If a company is in more than one market around the world, it may be able to spread the risk of a slowdown in one region over a larger portion of its revenue stream. In other words, diversification on a global scale allows companies to benefit from booming economies while protecting against the negative consequences of slumping ones. BUD, through its diverse geographical presence, benefited at a time when some of its markets reported poor results while others reported tremendous growth. The net effects of these dynamics were what I would term “strong” Q3 2022 results. Below are the highlights of some of its major markets in Q3 2022.

- Despite inflation, volume trends in all major beer sectors in the US have improved during the year. Top line and cash flow grew again this quarter. Its above-core beer portfolio gained share for the third quarter in a row, led by Michelob ULTRA, with volumes climbing by double digits. Its STR volumes dropped by 1.7%, which is less than the industry average. In the experience-based ready-to-drink market, its portfolio continued to do better than the industry average, with both Cutwater and NÜTRL growing by a lot more than the industry average.

- In Mexico, they increased market share and posted double-digit top and bottom-line growth for the third quarter. Their volumes increased by more than 10%

- In Colombia, they generated double-digit top and high single-digit bottom line growth and expanded the beer category again, hitting record per capita consumption. Their premium and super-premium brands reached all-time high volumes and revenue share.

- In Brazil they grew double-digit top and bottom lines and EBITDA margins. This quarter, their premium and super-premium brands outperformed with high single-digit volume growth. We maintained good beer volumes year-over-year.

- In Europe, the company’s revenue increased by double digits due to volume growth, revenue management initiatives, and on-premise recovery.

BUD Q3 022 Call Presentation

The information above shows not only how different economies compare to each other, but also how diversity as a whole contributed to a 3.7% increase in volume. Most of the company’s markets have grown, which I think is a sign that the deleveraging plan has led to a strong recovery. I think the company will have even better growth numbers in the coming quarters, thanks to this variety and the optimism that comes from having low debt levels.

Adept Use of Credit and Effective Debt Reduction

Debt financing is beneficial since it helps spur expansion and growth by increasing CAPEX and working capital, but it can be detrimental if used excessively because it compromises the company’s overall financial health. The company’s debt peaked in 2016 at $123.25B, and since then it has been steadily decreasing. The debt has been reduced from that amount to the current total of $83.53 billion.

Seeking Alpha

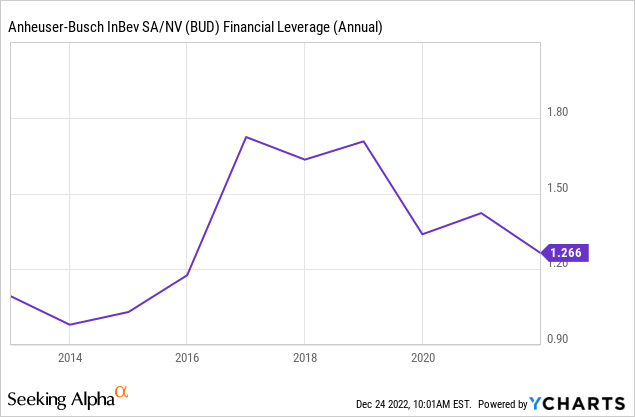

The financial leverage of the company has improved as a result of this deleveraging and now stands at 1.26, down from roughly 1.75 in 2016. I anticipate that this ratio will fall below 1 as the corporation continues its deleveraging strategy.

As for the company’s management of its debt, I found two things to be very impressive. To begin, the company’s management took precautions to protect it from the potentially disastrous effects of rising interest rates and inflation by ensuring that 94% of its bonds have a fixed rate. Given the current difficult macroeconomic situation, which is marked by rising interest rates and inflation, I have to say that the management was smart to take this approach. Second, during the financing process, the company made good use of its geographical variety to reduce its exposure to currency fluctuations. They achieved this goal by acquiring a diversified debt portfolio devoid of financial covenants and denominated in a number of different currencies.

Fernando Tennenbaum, “Moreover, our debt portfolio does not have any financial covenants and is comprised of a variety of currencies, thereby diversifying our FX risk.” “94% of our bonds have a fixed rate, insulated from interest rate volatility and inflation.”

In my opinion, the ease with which the corporation has handled its debt in spite of the harsh macroeconomic environment is due to these two factors.

Another factor to note about its debt is its maturity. BUD has $2.8 billion in bonds that mature between now and 2025, and according to the company’s chief financial officer, the company has more than enough cash on hand to pay down all of them. Something I strongly agree with given their cash balance of $7.36 billion, which is three times the debt due in 2025. This is another piece of evidence that the corporation has a grasp on its debt. In closing, I want to say how impressed I am with the management team’s skillful utilization of credit and their regular and consistent debt servicing. The company’s low debt level, in my opinion, marks the beginning of a great performance that will quicken as deleveraging proceeds.

Conclusion

BUD’s share price has been on an upward trend since October, indicating that the company may be on the mend after a roughly six-year negative trend in share prices. These positive signs are mostly due to the company’s plan to reduce debt, which has led to better financial leverage. Based on the company’s current debt level, which I think is low compared to how much it owed in 2016, and the fact that the company is committed to continuing to pay off this debt, I expect the stock price to keep increasing as it has been doing since October. I expect this growth to speed up as the company keeps paying off its debt.

It’s also important to remember that the company has a long way to go until its debt matures, with the closest maturity date being 2025, which can be met three times over with the company’s existing liquidity. Also, the company’s loans have no commitments, and the interest rates are fixed in several currencies. This makes it easy to pay off the debt, even in the current tough economic climate with rising inflation, interest rates, and fluctuating currencies. If the company’s growth as a result of its global diversity and deleveraging strategy were a journey by plane, I would just fasten my seatbelt because the flight is about to take off.